Sterling rises broadly today as recession risk recede after better than expected GDP data. While it’s unsure whether growth could sustain, the Pound cheers the improved outlook anyway. At this point, Australian Dollar is second strongest, followed by New Zealand Dollar. On the other hand, Swiss Franc is the weakest one, followed by Yen and then Dollar.

Technically, both GBP/USD and GBP/JPY extend last week’s rebound and further rise should be seen. Focus will be on whether 1.2502 and 135.07 would hold on next rises. More importantly, EUR/GBP will be facing 0.8891 cluster support. For, we’d still expect this support to hold to bring rebound. But decisive break will extend the fall from 0.9324 to 0.8797 fibonacci level and possibly below.

In Europe, FTSE is down -0.69%. DAX is up 0.39%. CAC is down -0.13%. German 10-year yield is up 0.0365 to -0.597, back above -0.6 handle. Earlier in Asia, Nikkei rose 0.56%. Hong Kong HSI dropped -0.04%. China Shanghai SSE rose 0.84%. Singapore Strait Times rose 0.06%. Japan 10-year JGB yield dropped -0.0107 to -0.255.

UK GDP grew 0.3% in July, but flat in the three months

UK GDP grew 0.3% mom in July, well above expectation of 0.1% mom. However, for the three months to July, GDP was flat, following -0.2% from April to June. Looking at the details for the three months to July, Index of services rose 0.13%. Index of production dropped -0.07%. Index of construction dropped -0.05%.

Head of GDP Rob Kent-Smith said: “GDP growth was flat in the latest three months, with falls in construction and manufacturing. While the largest part of the economy, services sector, returned to growth in the month of July, the underlying picture shows services growth weakening through 2019. The trade deficit narrowed due to falling imports, particularly unspecified goods (including non-monetary gold), chemicals and road vehicles in the three months to July.”

Also from UK, industrial production came in at 0.1% mom, -0.9% yoy in July versus expectation f0.0% mom, -1.0% yoy. Manufacturing production was at 0.3% mom, -0.6% yoy versus expectation of 0.0% mom, -1.0% yoy. Visible trade deficit widened slightly to GBP-9.1B, smaller than expectation of -9.6B.

NIESR expects UK economy to return to growth, but unsure for how long

The NIESR said in a report that UK economy is on course to grow 0.3% in Q3, rebounding from Q2’s -0.2% contraction. NIESR said it’s a “welcome resumption of economic growth”. However, it also warned that “it is not clear how long growth will continue.”.

NIESR added, “Only the services sector is expanding, primarily to meet higher demand from consumers driven by increased household incomes fuelled by rising real wages. But there is a limit to how much further real wages can grow without a pick-up in investment and productivity, and this seems unlikely in the near term.”

UK parliament to be suspended after today’s businesses

UK Prime Minister Boris Johnson’s call for general election today will very much likely fail. Labour already indicated in a statement that they “would not support Boris Johnson’s ploy to deny the people their decision by crashing us out of the EU with No Deal during a general election campaign”. Meanwhile, Johnson’s spokesperson James Slack has confirmed that Parliament will be suspended once today’s business has been completed.

Separately, Johnson said in Ireland, alongside Irish Prime Minister Leo Varadkar that he wants to “find a deal” and “get a deal” on Brexit. And, “for the sake of business, for farmers, and millions of ordinary people who are counting on us to use our imagination and creativity to get this done. I want you to know I would overwhelmingly prefer to find an agreement.”

Varadkar, on the other hand, said “in the absence of agreed alternative arrangements, no backstop is no deal for us… We are open to alternatives, but they must realistic ones, legally binding and workable and we haven’t received such proposals to date.”

Eurozone Sentix investor confidence improved to -11.1, but economy not far from recession

Eurozone Sentix Investor Confidence improved to -11.1 in September, up from -13.7 and beat expectation of -16.0. Expectations Index improved notably from -20.0 to -12.8. However, Current Situation Index declined for the fourth month in a row, from -7.3 to -9.5, hitting the lowest level since January 2015.

The Current Situation Index shows that “Eurozone is not far from a recession”, as noted by Sentix, as they expected a recession from -10 points. Sentix added: “It is also questionable whether a recession can be avoided. For even if the expected values have improved significantly to -12.8 points, they still bear a negative sign. A sustained turnaround would require positive expectations.”

Sentix also said, “Investors are focusing on two issues here: firstly, the trade dispute between the USA and China. After the bad experiences with US President Trump’s tweets, however, hardly anyone is prepared to make an advance payment here. What remains is the ECB, from which investors expect real wonders at the forthcoming meeting. The sentix barometer for central bank policy is +30 points. So, the expectations of Mario Draghi to deliver something big and effective are high. We’ll see if he can deliver. For the financial markets, but even more for the real economy.”

Also released, German trade surplus widened to EUR 20.2B in July, above expectation of EUR 18.8B. Swiss unemployment rate was unchanged at 2.3% in August.

Bank of Franc MIBA indicates 0.3% GDP growth in Q3

According to its monthly index of business activity (MIBA), Bank of Franc said GDP is expected to grow 0.3% in Q3. Manufacturing indicator rose from 96 to 99 as industrial production gained ground. Services indicator was unchanged at 100, picked up slightly. Construction indicator was unchanged at 104 as activity was almost stable in August in both structural and finishing works.

Japan Q2 GDP finalized at 0.3% qoq, private consumption driven

Japan Q2 GDP growth was finalized at 0.3% qoq, revised down from 0.4% qoq. The economy grew at annualized pace of 1.3%, sharply lower than preliminary reading of 1.8%. GDP deflator was finalized at 0.4% yoy, unrevised.

Growth was primarily driven by consumer spending, which grew 0.6% qoq. While continued growth in private consumption is expected ahead, it could take a hit from the planned sales tax hike in October.

Meanwhile, business investment was weak and just grew 0.2% qoq. Considering global slowdown and uncertainties from trade tensions, business investment has already shown some resilience. Yet, as US-China trade war intensified in Q3, there is more headwind for businesses for the rest of the year.

Also from Japan, current account surplus narrowed to JPY 1.65T in July, slightly below expectation of JPY 1.70T.

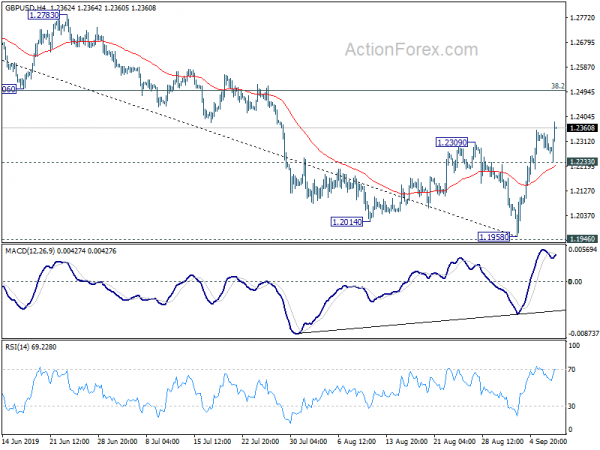

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2265; (P) 1.2305; (R1) 1.2329; More….

GBP/USD’s rebound from 1.1958 extends further to as high as 1.2385 so far today. Intraday bias stays on the upside for 38.2% retracement of 1.3381 to 1.1958 at 1.2502 first. Break will target 61.8% retracement at 1.2837. On the downside, however, break of 1.2233 minor support will turn bias back to the downside for 1.1958 support instead.

In the bigger picture, we’d remain cautious on medium term bottoming around 1.1946 (2016 low). Sustained trading above 55 week EMA (now at 1.2779) will extend the consolidation pattern from 1.1946 with another rise to 1.4376 resistance. Nevertheless, decisive break of 1.1946 will resume down trend from 2.1161 (2007 high) to 61.8% projection of 1.7190 to 1.1946 from 1.4376 at 1.1135.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Manufacturing Activity Q2 | -0.70% | 1.00% | 0.80% | |

| 23:50 | JPY | Current Account (JPY) Jul | 1.65T | 1.70T | 1.94T | |

| 23:50 | JPY | GDP Q/Q Q2 F | 0.30% | 0.30% | 0.40% | |

| 23:50 | JPY | GDP Deflator Y/Y Q2 F | 0.40% | 0.40% | 0.40% | |

| 1:30 | AUD | Home Loans M/M Jul | 5.00% | 0.50% | -0.90% | -0.80% |

| 5:45 | CHF | Unemployment Rate Aug | 2.30% | 2.30% | 2.30% | |

| 6:00 | EUR | German Trade Balance (EUR) Jul | 20.2B | 18.8B | 18.1B | 18.0B |

| 8:30 | EUR | Eurozone Sentix Investor Confidence Sep | -11.1 | -16 | -13.7 | |

| 8:30 | GBP | Monthly GDP M/M Jul | 0.30% | 0.10% | 0.00% | |

| 8:30 | GBP | Industrial Production M/M Jul | 0.10% | 0.00% | -0.10% | |

| 8:30 | GBP | Industrial Production Y/Y Jul | -0.90% | -1.00% | -0.60% | |

| 8:30 | GBP | Manufacturing Production M/M Jul | 0.30% | 0.00% | -0.20% | |

| 8:30 | GBP | Manufacturing Production Y/Y Jul | -0.60% | -1.00% | -1.40% | |

| 8:30 | GBP | Construction Output M/M Jul | 0.50% | 0.20% | -0.70% | |

| 8:30 | GBP | Index of Services 3M/3M Jul | 0.20% | 0.10% | 0.10% | |

| 8:30 | GBP | Visible Trade Balance (GBP) Jul | -9.1B | -9.6B | -7.0B | -8.9B |

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals