Euro drops broadly after ECB finally delivers and announced a package of stimulus. The cut in deposit rate and size of QE are somewhat smaller than expected. But the new economic projections remain decidedly dovish despite the easing package. At this point, Sterling is following closely as the second weakest and then Canadian. Dollar firm up mildly after stronger than expected core CPI reading. Yet, it’s, for now, still overwhelmed slightly by Yen, as treasury yields reverse this week’s gains.

Technically, despite today’s fall, EUR/USD has yet to break 1.0926 support. This will remain the focus for the rest of the session. Firm break will resume larger down trend to 1.0813 fibonacci level next. EUR/GBP breaches 0.8891 key cluster support briefly but fails to sustain so far. Firm break there will dampen our original bullish view and bring deeper fall to 0.8797 fibonacci level and below. EUR/JPY also breaches 117.73 minor support, without follow through selling. Firm break will indicate completion of rebound from 115.86 and bring retest of this low.

In Europe, currently, FTSE is up 0.11%. DAX is up 0.70%. CAC is up 0.70%. German 10-year yield is down -0.060 at -0.620, back below -0.6 handle. Earlier in Asia, Nikkei rose 0.75%. Hong Kong HSI dropped -0.26%. China Shanghai SSE rose 0.75%. Singapore Strait Times dropped -0.30%. Japan 10-year JGB yield dropped -0.004 to -0.21.

Euro dives as ECB cuts deposit rate, restarts QE

ECB announced to cut deposit facility rate by -10bps to -0.50%. Main refinancing rate and marginal lending facility rate are kept unchanged at 0.00% and 0.25% respectively. A two-tier system for reserve remuneration will also be introduced, with part of banks’ holdings of excess liquidity exempted from negative deposit rate.

Forward guidance is also changed to “The Governing Council now expects the key ECB interest rates to remain at their present or lower levels until it has seen the inflation outlook robustly converge to a level sufficiently close to, but below, 2% within its projection horizon, and such convergence has been consistently reflected in underlying inflation dynamics.”

ECB will also restart asset purchase program at EUR 20B per month, starting November 1, without any specified end date.

ECB revised down growth in inflation projections after easing

ECB’s GDP growth projections are revised to 1.1% in 2019 (vs 1.2% in June), 1.2% in 2020 (vs 1.4%) and 1.4% in 2021 (unchanged).

Eurozone’s slowdown in growth mainly reflects “prevailing weakness of international trade in an environment of prolonged global uncertainties which are particularly affecting the euro area manufacturing sector.” But services and construction show “ongoing resilience. Risk to growth “remain tilted to the downside” due to “prolonged presence of uncertainties, related to geopolitical factors, the rising threat of protectionism and vulnerabilities in emerging markets.”

HICP inflation projections are revised down over the whole projection horizon, “reflecting lower energy prices and the weaker growth environment.” HICP projections are at 1.2% in 2019 (vs 1.3% in June), 1.0% in 2020 (vs 1.4%), 1.4% in 2021 (vs 1.6%).

Eurozone industrial production dropped -0.4%, below expectation of 0.1%

Eurozone industrial production dropped -0.4% mom in July, well below expectation of 0.1% mom. EU28 industrial production dropped -0.1% mom. In the euro area, for monthly comparison. production of non-durable consumer goods fell by -0.8% mom, energy by -0.7% mom and intermediate goods by -0.3% mom, while production of durable consumer goods rose by 1.2% mom and capital goods by 1.8% mom.

Among Member States of EU28 for which data are available, the largest decreases in industrial production were registered in Romania (-3.3% mom), Estonia (-2.9% mom) and Latvia (-2.1% mom). The highest increases were observed in Croatia (4.9% mom), Portugal (3.6% mom) and Denmark (3.5% mom).

Also released, Germany CPI was finalized at -0.2% mom, 1.4% yoy in August. Swiss PPI dropped -0.2% mom, -1.9% yoy in August.

German Ifo warns of recession, downgrades 2019 GDP forecast to 0.5%

Ifo warned in the Economic Forecast Autumn 2019 that German economy is at risk of recession. -0.1% GDP contraction is expected in Q3, thus, together with -0.1% drop in Q2, that’s a technical recession. Also, 2019 growth forecast was downgraded from 0.6% to 0.5%.

Ifo noted: “This downturn was triggered by a series of world political events calling into question a global economic order that had evolved over decades and required adjustments to established international value chains. As a result, economic uncertainty worldwide rose to historic highs and the international economy cooled off increasing”.

“Meanwhile, world trade and world industrial production are declining. In addition, automobile manufacturers in particular are facing an abrupt technology shift, which in some cases brings with it enormous adaptation requirements.”

US CPI slowed to 1.7%, but core CPI accelerated to 2.4%

US CPI slowed to 1.7% yoy in August, down from 1.8% and matched expectations. Core CPI, on the other hand, accelerated to 2.4% yoy, up from 2.2% yoy and beat expectation of 2.3% yoy.

Also released, initial jobless claims dropped -15k to 204k in the week ending September 7, better than expectation of 217k. Four-week moving average dropped -4.25k to 212.5k. Continuing claims dropped -4k to 1.67m in the week ending August 31. Four-week moving average dropped -14.5k to 1.680m.

Released earlier today

UK RICS house price balance improved to -4 in August, up from -9 and beat expectation of -10. Japan domestic CGPI dropped -0.9% yoy in August, below expectation of -0.8% yoy. Machine orders dropped -6.6% mom in July versus expectation of -8.1% om. Tertiary industry index rose 0.1% mom in July, above expectation of -0.3% mom. Australia consumer inflation expectations dropped to 3.1% in September.

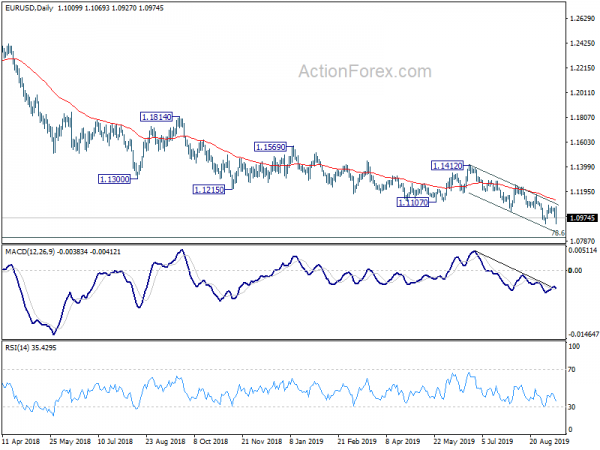

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0979; (P) 1.1017; (R1) 1.1050; More…

EUR/USD drops sharply today but stays above 1.0926 support. Intraday bias remains neutral first. Consolidation from 1.0926 could extend with another recovery. But upside is expected to be limited below 1.1164 resistance to bring fall resumption. On the downside, break of 1.0926 will resume lager down trend from 1.2555 for 1.0813 fibonacci level next.

In the bigger picture, down trend from 1.2555 (2018 high) is in progress. Prior rejection of 55 week EMA also maintained bearishness. Further fall should be seen to 78.6% retracement of 1.0339 to 1.2555 at 1.0813. Decisive break there will target 1.0339 (2017 low). On the upside, break of 1.1412 resistance is needed to indicate medium term bottoming. Otherwise, outlook will stay bearish in case of rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | RICS House Price Balance Aug | -4% | -10% | -9% | |

| 23:50 | JPY | Domestic CGPI Y/Y Aug | -0.90% | -0.80% | -0.60% | |

| 23:50 | JPY | Machine Orders M/M Jul | -6.60% | -8.10% | 13.90% | |

| 1:00 | AUD | Consumer Inflation Expectation Sep | 3.10% | 3.50% | ||

| 4:30 | JPY | Tertiary Industry Index M/M Jul | 0.10% | -0.30% | -0.10% | |

| 6:00 | EUR | German CPI M/M Aug F | -0.20% | -0.20% | ||

| 6:00 | EUR | German CPI Y/Y Aug F | 1.40% | 1.40% | ||

| 6:30 | CHF | Producer & Import Prices M/M Aug | -0.10% | |||

| 6:30 | CHF | Producer & Import Prices Y/Y Aug | -1.70% | |||

| 9:00 | EUR | Eurozone Industrial Production M/M Jul | 0.10% | -1.60% | ||

| 11:45 | EUR | ECB Rate Decision | 0.00% | 0.00% | ||

| 11:45 | EUR | ECB Marginal Lending Facility | 0.25% | 0.25% | ||

| 11:45 | EUR | ECB Deposit Facility Rate | -0.50% | -0.40% | ||

| 12:30 | EUR | ECB Press Conference | ||||

| 12:30 | CAD | New Housing Price Index Y/Y Jul | 0.00% | -0.20% | ||

| 12:30 | USD | CPI M/M Aug | 0.10% | 0.30% | ||

| 12:30 | USD | CPI Y/Y Aug | 1.70% | 1.80% | ||

| 12:30 | USD | CPI Core M/M Aug | 0.20% | 0.30% | ||

| 12:30 | USD | CPI Core Y/Y Aug | 2.30% | 2.20% | ||

| 12:30 | USD | Initial Jobless Claims (SEP 7) | 217K | 217K | ||

| 14:30 | USD | Natural Gas Storage | 84B |

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals