Euro drops broadly today on some dovish comments from ECB officials. Also, it’s believed that surge in oil prices could hurt Eurozone’s balance of payment. Sterling stays weak as meeting between Prime Minster Boris Johnson and EU Jean-Claude Juncker ended without any noticeable progress. Generally weaker sentiments also keep Australian Dollar soft. On the other hand, Canadian Dollar remains the strongest one as oil prices surged after attack on Saudi Arabia’s production facilities. Yen is the second strongest on mild risk aversion, followed by Dollar.

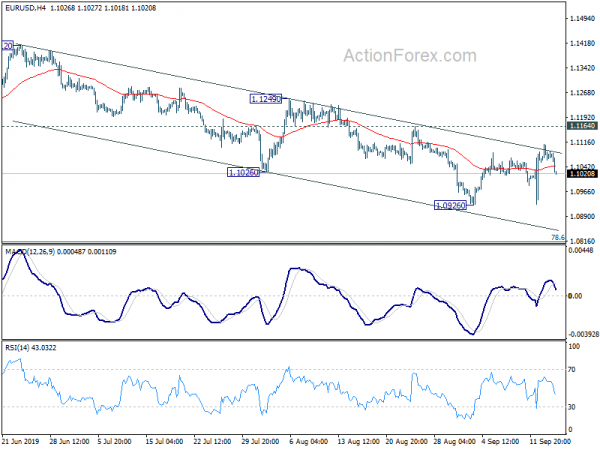

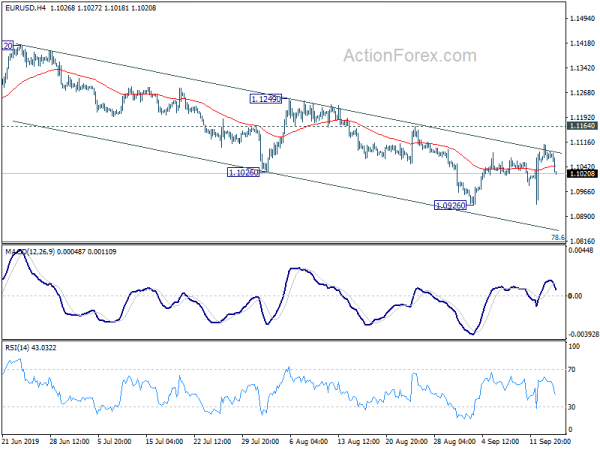

Technically, EUR/USD was rejected by near term falling channel resistance and focus could be back to 1.0926 low. Though, as long as this support holds, near term consolidations could still expected. Recovery in USD/CHF also puts focus back to 0.9946 temporary top. Break will resume the choppy rebound from 0.9569. USD/CAD recovered after initial dip today. With 1.3177 minor support intact, rebound from 1.3133 is still in favor to extend to 1.3382 resistance.

In Europe, FTSE is down -0.26%. DAX is down -0.55%. CAC is down -0.63%. German 10-year yield is down -0.0253 at -0.471, but staying comfortably above -0.5. Earlier in Asia, Japan was on holiday. Hong Kong HSI dropped -0.83%. China Shanghai SSE dropped -0.02%. Singapore Strait Times dropped -0.24%.

US Empire state manufacturing dropped to 2, future optimism waned

US Empire State Manufacturing Survey general business conditions index dropped to 2.0 in September, down from -4.8 and missed expectation of 4.0. 27% of respondents reported that conditions had improved over the month, but 25% said conditions had worsened. Number of employees index jumped sharply from -1.6 to 9.7, back in positive territory. The index for future business conditions fell -12 points to 13.7, suggesting that “optimism about future conditions waned”.

ECB Stournaras: Insufficient contribution from fiscal policy

ECB Governing Council member Yannis Stournaras said there is strong case for incoming President Christine Lagarde to maintain policy stimulus. And, he added, “stimulus package last week was necessary because inflation remains very low. Benefits of taking action now exceed to a large extent the costs. There has been an insufficient contribution from fiscal policy.

Another Governing Council member Pablo Hernandez De Cos urged stronger progress towards fiscal union. He said in an event in Spain that “I strongly believe that a central fiscal capacity at euro area level could contribute … to macroeconomic stabilization.” Additionally, “monetary policy would not become overburdened, as it might be in the current economic juncture.”

UK Johnson and EU Juncker agreed to intensify discussion on Brexit

UK Prim Minister Boris Johnson’s office issued a statement after his meeting with European Commission President Jean-Claude Juncker. The statement noted “the leaders agreed that the discussions needed to intensify and that meetings would soon take place on a daily basis”.

And, “It was agreed that talks should also take place at a political level between Michel Barnier and the Brexit Secretary, and conversations would also continue between President Juncker and the Prime Minister.”

Johnson’s spokesman also reiterated that he would not request a delay to Brexit beyond October 31.

Chinese Premier Li said very difficult to grow at 6%, data showed deepened slowdown

Chinese Premier Li Keqiang warned that the economy is facing “certain downward pressure” due to global slowdown and rise of protectionism. And, it’s “very difficult” for GDP to grow at 6% rate or higher. He said “for China to maintain growth of 6% or more is very difficult against the current backdrop of a complicated international situation and a relatively high base, and this rate is at the forefront of the world’s leading economies.”

A batch of August data released today showed deepened slowdown in China’s economy. Industrial production growth slowed to 4.4% yoy in August, down from 4.8% yoy and missed expectation of 5.2% yoy. That’s the slowest pace since February 2002. Retail sales growth slowed to 7.5% yoy, down from 7.6% yoy and missed expectation of 8.0% yoy. Fixed assets investments grew 5.5% ytd yoy, below expectation of 5.7% ytd yoy. Surveyed unemployment rate, though, dropped from 5.3% to 5.2%.

Suggested reading on China: China Watch – Economy Going from Bad to Worse.

WTO services trade barometer at 98.4, broad loss of momentum

The new WTO’s Services Trade Barometer came in at 98.4, slightly below baseline value of 100. The reading indicates that serves trade continued to face strong headwinds into second half of the year.

WTO noted that “declines in most of the Services Trade Barometer’s component indices drove the second quarter softening, as they signalled a broad loss of momentum across various services sectors.” However, despite loss of momentum this year, “services trade has generally held up better than goods trade since the latter is more directly affected by recent trade tensions.”

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1049; (P) 1.1079; (R1) 1.1103; More…

EUR/USD was rejected by near term falling channel resistance and drops notably today. But downside is held well above 1.0926 low. Intraday bias remains neutral first and more consolidation could be seen. Overall outlook remains bearish as long as 1.1164 resistance holds. Firm of 1.0926 will resume lager down trend from 1.2555 for 1.0813 fibonacci level next. However, firm break of 1.1164 will be an early indication of larger reversal and target 1.1249 resistance .

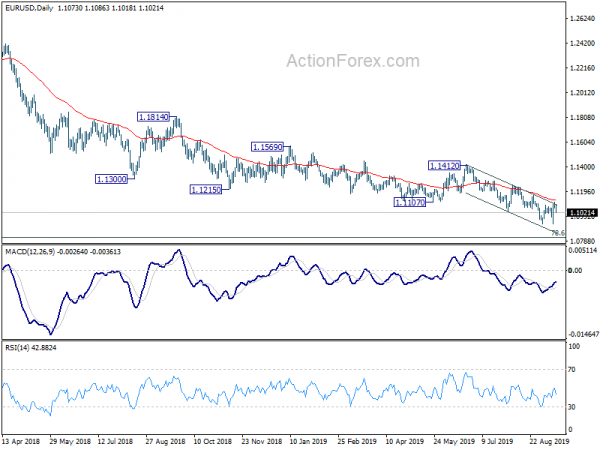

In the bigger picture, down trend from 1.2555 (2018 high) is in progress. Prior rejection of 55 week EMA also maintained bearishness. Further fall should be seen to 78.6% retracement of 1.0339 to 1.2555 at 1.0813. Decisive break there will target 1.0339 (2017 low). On the upside, break of 1.1412 resistance is needed to indicate medium term bottoming. Otherwise, outlook will stay bearish in case of rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | Rightmove House Prices M/M Sep | -0.20% | -1.00% | ||

| 02:00 | CNY | Fixed Assets Ex Rural YTD Y/Y Aug | 5.50% | 5.70% | 5.70% | |

| 02:00 | CNY | Industrial Production Y/Y Aug | 4.40% | 5.20% | 4.80% | |

| 02:00 | CNY | Retail Sales Y/Y Aug | 7.50% | 8.00% | 7.60% | |

| 02:00 | CNY | Surveyed Jobless Rate Aug | 5.20% | 5.30% | ||

| 12:30 | CAD | International Securities Transactions (CAD) Jul | -1.17B | 2.53B | -3.98b | -4.06B |

| 12:30 | USD | Empire State Manufacturing Sep | 2 | 4 | 4.8 |

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals