Sterling remains undoubtedly the strongest one for today, and the week, cheering Conservative’s landslide victory in UK elections. Boris Johnson pledged that “we will get Brexit done on time by the 31st of January, no ifs, no buts, no maybes.” That’s what markets are firmly believing in now. Meanwhile, sentiments turned cautious though as US-China trade deal is back under question, or at least the terms. We’d only know if there would be tariff rollbacks after the expected form announcement by Trump’s administration today.

Technically, GBP/USD and GBP/JPY retreats after this week strong rally. But near term outlook will remain bullish as long as 1.3050 and 142.47 support holds respectively. Similarly, while EUR/GBP recovers, outlook will stay bearish as long as 0.8508 resistance holds. USD/JPY was rejected by 109.72 resistance on renewed uncertainty on US-China trade deal. Consolidation might extend into early next week.

In Europe, currently, FTSE is up 1.98%. DAX is up 0.65%. CAC is up 0.70%. German 10-year yield is up 0.0010 at -0.257. Earlier in Asia, Nikkei rose 2.55%. Hong Kong HSI rose 2.57%. China Shanghai SSE rose 1.78%. Singapore Strait Times rose 0.61%. Japan 10-yaer JGB yield dropped -0.0105 to -0.029.

Markets rocked as Trump said WSJ report on China trade deal was fake news

Markets are rocked by US President Donald Trump’s tweet again. He complained that WSJ’s story regarding US-China trade deal was “completely wrong, especially their statement on Tariffs.” He added, “Fake News. They should find a better leaker!”

Trump said yesterday that he’s getting “VERY close to a BIG DEAL with China.” WSJ indicated US would cut the currently imposed tariffs by 50% as part of the deal. New tariffs would be put on hold. China generally believed to offer to step up US farm products purchases in 2020, possibly doubling from the value in 2017 to USD 50B.

Markets are expecting some form of formal announcement to be made today by US administration. It remains to be seen if that would happen.

US retail sales rose 0.2%, ex-auto sales rose 0.1%

US retail sales rose 0.2% mom to USD 528.0B in November, below expectation of 0.4% mom Ex-auto sales rose 0.1% mom, below expectation of 0.4% mom. Ex-gasoline sales rose 0.1% mom. Import price index rose 0.2% mom, matched expectations.

Released earlier, Japan Tankan large manufacturing index dropped to 0 in Q4, down from 5. Large manufacturing outlook dropped to 0, down from 2. Both missed expectations. However, non-manufacturing index dropped to 20, down from 21. Non-manufacturing outlook rose to 18, up from 15. Both beat expectations. All industry capex rose 6.8%, beat expectation of 6.0%.

New Zealand BusinessNZ manufacturing index dropped to 51.4 in November, down from 52.6.

ECB de Guindos said UK election results eliminate uncertainty in the short term

ECB Vice President Luis de Guindos hailed that “the results of the elections in Great Britain are positive because they eliminate uncertainty in the short term”. And, “we know perfectly well that on the 31st January the United Kingdom will leave the union – this is good in terms of uncertainty, but also hails a new period, one which will not be easy.” “It will not be easy because commerce rules will have to be renegotiated.”

Separately, Governing Council member Francois Villeroy de Galhau said “The economic situation in the euro zone is beginning to stabilise … and as the situation stabilizes so does monetary policy”. He added, “we are applying the measures decided in September and aren’t adding any more… For how long depends on the economic situation and its improvement.” Another Governing Council member Bostjan Vasle said “domestic factors represent the main drive of economic activity while the growth of foreign demand will be weak”.

EU von der Leyen aims at zero tariff, zero quotas, zero dumping with UK

European Commission President Ursula von der Leyen talked about future relationship with UK after Brexit. She said “We aim at zero tariff, zero quotas and zero dumping, and this is very important for us.”

She also warned that “we are addressing the challenge that the time is very short, we have 11 months to negotiate a broad field”. “And it’s not only about trade, but we are also speaking about education, transport, fisheries, many, many other fields are in the portfolio to be negotiated.”

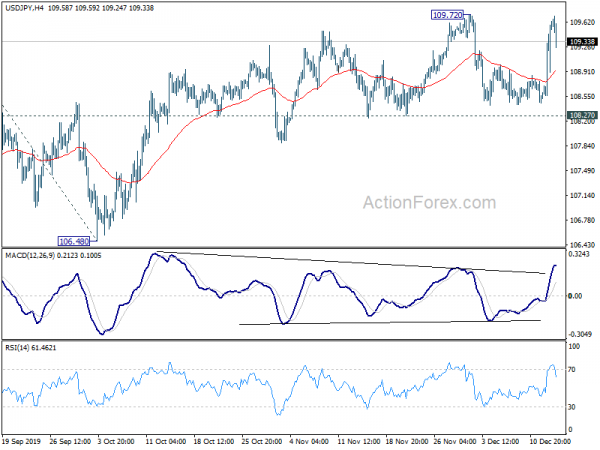

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 108.69; (P) 109.07; (R1) 109.68; More..

USD/JPY retreats notably after failing to break through 109.72 resistance. Intraday bias is turned neutral first. As long as 108.27 support holds, outlook remains bullish for further rally. On the upside, break of 109.72 will resume the rise fro 104.45 for 100% projection of 104.45 to 108.47 from 106.48 at 110.50. However, sustained break of 108.27 support will indicate near term reversal and turn outlook bearish.

In the bigger picture, strong support was seen from 104.62 again. Yet, there is no confirmation of medium term reversal. Corrective decline from 118.65 (Dec. 2016) could still extend lower. But in that case, we’d expect strong support above 98.97 (2016 low) to contain downside to bring rebound. Meanwhile, on the upside, break of 112.40 key resistance will be a strong sign of start of medium term up trend.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | NZD | BusinessNZ Manufacturing Index Nov | 51.4 | 52.6 | ||

| 23:50 | JPY | Tankan Large Manufacturing Outlook Q4 | 0 | 3 | 2 | |

| 23:50 | JPY | Tankan Large Manufacturing Index Q4 | 0 | 2 | 5 | |

| 23:50 | JPY | Tankan Non – Manufacturing Outlook Q4 | 18 | 16 | 15 | |

| 23:50 | JPY | Tankan Non – Manufacturing Index Q4 | 20 | 16 | 21 | |

| 23:50 | JPY | Tankan Large All Industry Capex Q4 | 6.80% | 6.00% | 6.60% | |

| 04:30 | JPY | Industrial Production M/M Oct F | -4.50% | -4.20% | -4.20% | |

| 13:30 | USD | Retail Sales M/M Nov | 0.20% | 0.40% | 0.30% | 0.40% |

| 13:30 | USD | Retail Sales ex Autos M/M Nov | 0.10% | 0.40% | 0.20% | 0.30% |

| 13:30 | USD | Import Price Index M/M Nov | 0.20% | 0.20% | -0.50% | |

| 15:00 | USD | Business Inventories Oct | 0.20% | 0.00% |

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals