Executive Summary

- The global outlook is dominated by negative economic effects of efforts from governments around the world to stem the spread of the coronavirus, as well as low global oil prices. Against this bleak backdrop, we have reduced our GDP forecasts for the Eurozone, United Kingdom, Japan and Canada. Given the extent of the economic shocks, we now see the global economy entering recession in the first half of this year and expect global GDP to contract by 2.9% in 2020, though we do expect global markets and economic activity to stabilize by late this year.

- With most major and emerging economies set to fall into recession in 2020, monetary and fiscal policymakers have responded with aggressive stimulus measures. Despite these efforts, we doubt they will be enough to help these economies avoid a deep slump in growth in the near term.

How Low Can the Economic Data Go?

As the COVID-19 crisis continues to evolve, with global cases now more than 2,170,000 and global fatalities more than 146,000, the global economic outlook continues to deteriorate due to effects of the virus and measures taken by governments to contain its spread. In recent weeks, the incoming data have started to more clearly illustrate the potential extent of the economic damage.

- In China, which was the first major economy to be affected by the COVID-19 outbreak, Q1 GDP slumped 9.8% quarter-over-quarter and 6.8% year-over-year. For Q1, retail sales dropped some 19% year-over-year, while industrial output fell 8.4%.

- In the U.S., there have been a cumulative 22,034,000 initial jobless claims in the past four weeks, and even though nonfarm payrolls fell by only 701,000 in March, much larger declines are likely in the months ahead. March retail sales fell a record 8.7% month-over-month, an indication the service sector will be hard hit by lockdown measures.

- In Europe, there is so far only limited hard data to assess the potential effect of the COVID-19 crisis, although a 58% year-over-year drop in Eurozone March car registration offers an illustration of what is to come for the consumer sector. What’s more, manufacturing survey data point clearly to a sharp downturn across Europe, as the Eurozone and U.K. March services PMIs both plunged to record lows, of 26.4 and 34.5, respectively.

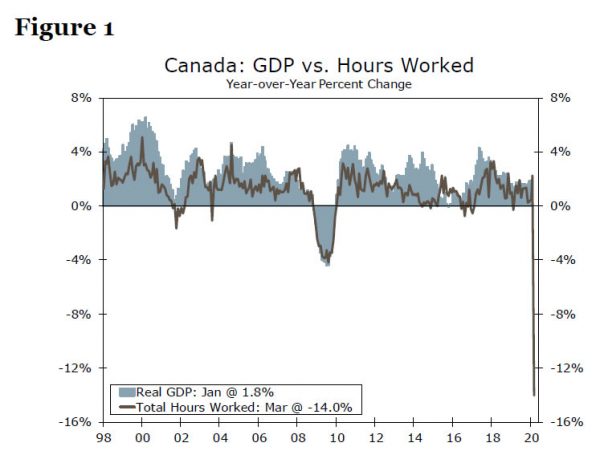

- Finally, in perhaps one of the starkest data points so far highlighting the effects of the COVID- 19 virus, Canadian March employment fell by 1,011,000, by far the largest monthly decline on record, and driven by a fall in private sector jobs. The unemployment rate jumped to 7.8%, while total hours worked plunged 15.1% month-over-month, potentially suggesting a similarsized drop in Canada’s March monthly GDP (Figure 1).

Overall, the key source of concern for the global economy has shifted to the services sector from the manufacturing sector. One of the most notable themes of 2019 was a relatively solid consumer and services sector (helped by solid employment and wage growth not only in the U.S., but also other major economies including the Eurozone, United Kingdom and Canada, among others). In contrast, industrial output was under pressure for large parts of last year, with persistent global trade tensions weighing on activity. Looking at the OECD countries (which includes most of the major developed economies, but does not include China), Q4 saw OECD employment growth of 1.0% year-over-year and compensation per employee growth of 2.9% year-over-year. Allowing for personal consumption inflation, real OECD compensation growth was running at 2.5% year-overyear in Q4 last year, a solid source for consumer spending (Figure 2). With dramatic employment declines to come in the months ahead, household incomes are set to turn from a source of stability to a source of instability, meaning a sharp global downturn is in prospect even as policymakers try to fill that income gap.

All Policymaker Hands on Deck

The sudden stop in economic activity, virtually simultaneously across the world, is unprecedented. In addition, as the flow of data has offered more precision on the likely severity of the global downturn, monetary and fiscal policymakers have also stepped up with an essentially unprecedented response.

Summarizing some of the key responses, and recognizing that it is not necessarily a “policy apples-to-apples” comparison across countries and regions, among the most important actions since early March so far are:

- U.S.: A cumulative 150 bps reduction in the fed funds rate, Fed purchases of Treasury securities and agency-backed mortgages securities in essentially unlimited amounts, and a range of other various purchase and liquidity programs to support various credit markets, and main street businesses. For fiscal policy, a stimulus package of around 9% of GDP was approved, with expectations of more to come.

- Eurozone: An extra €870B in asset purchases over the balance of 2020, with the majority of those under the Pandemic Emergency Purchase Program for which there are no issuer limits. The ECB also provided more long-term lending, at easier terms and conditions than previously. For the major Eurozone countries fiscal spending packages have so far ranged between 1.4% to 4.5% of GDP, while policymakers are also working on a coordinated €540B regional fiscal response, which would be around 4.5% of Eurozone GDP.

- U.K.: A cumulative 65 bps of rate cuts, an extra £200B in asset purchases, and a range of liquidity and lending programs. Meanwhile, fiscal stimulus so far has been around £65B or 3% of GDP.

- Japan: No major monetary policy moves, but a fiscal package with a headline figure of some ¥108 trillion (20% of GDP) covering multiple rounds of stimulus. That said, actual fiscal spending is close to ¥39 trillion (7% of GDP).

- Canada: A cumulative 150 bps of rate cuts and purchases of Canadian government securities of C$5B per week, provincial and corporate bond purchase programs, and other lending and liquidity measures. Fiscal stimulus measures currently amount to around 4.5% of GDP.

These policy responses are impressive and important, and are likely a contributing factor to some recovery in global equities from their recent lows, while they should also lead to an eventual stabilization in global economic activity—both developments that are important for the currency market outlook. However, given the size of the COVID-19 virus shock we think it is very unlikely these policy measures will be enough to help these economies avoid a sharp contraction in the near-term. As a result we have made some further significant downward revisions to our international growth outlook and now see 2020 GDP declines of 5.5% for the Eurozone, 5.4% for Japan, 4.9% for the United Kingdom and 5.7% for Canada.

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals