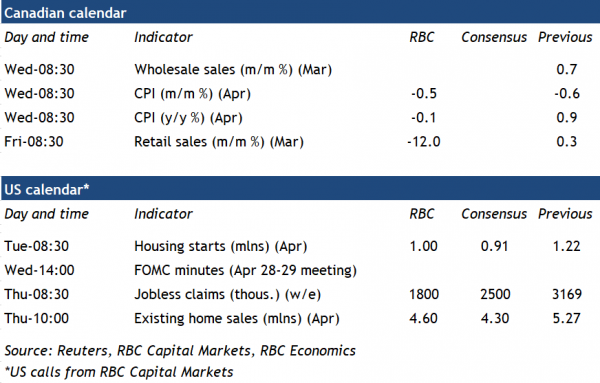

Next week brings two reports that will shed some more light on how the consumer sector (more than half of Canada’s economy) has been impacted by the COVID-19 crisis. March retail sales will look a bit stale, particularly with the US having already reported retail activity for April (much worse than March, and much worse than expected). Our own consumer spending tracker (using anonymized card data) suggests March was a tale of two halves in Canada, with spending falling sharply in the final two weeks of the month when coronavirus containment measures forced the closure of many non-essential storefronts. Declines are likely to be widespread but with clothing stores and auto dealerships leading the way (the latter isn’t captured in our card data but separate figures show unit sales were 50% lower in the month). Grocery and general merchandise stores (including big box retailers) should be the exception, and will actually have benefitted from consumers stocking up as pandemic concerns escalated.

On balance, though, we expect a double digit decline in overall retail sales that will easily exceed previous records. Again, based on the US experience and our own consumer tracking, retail spending slowed further in April when containment measures were in place for the full month (though our data suggests some improvement later in the month). It’s important to keep in mind that retail figures are only one aspect of consumer spending. Outlays on other services like restaurants, arts and entertainment, and travel and accommodation (none of which is captured in next week’s report) have declined significantly. At the same time, though, online spending isn’t fully accounted for in Canada’s retail sales data and will thus miss out on some of the growth in e-commerce purchases since the lockdown began.

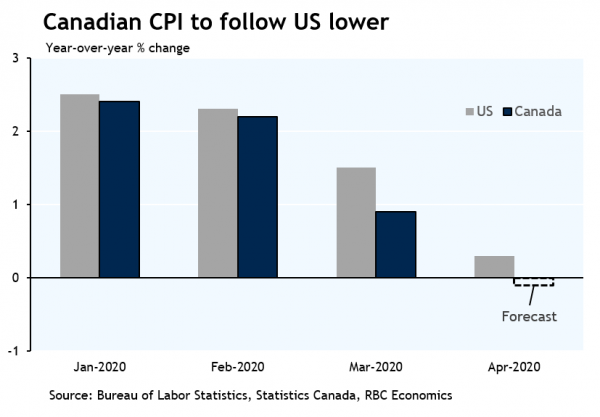

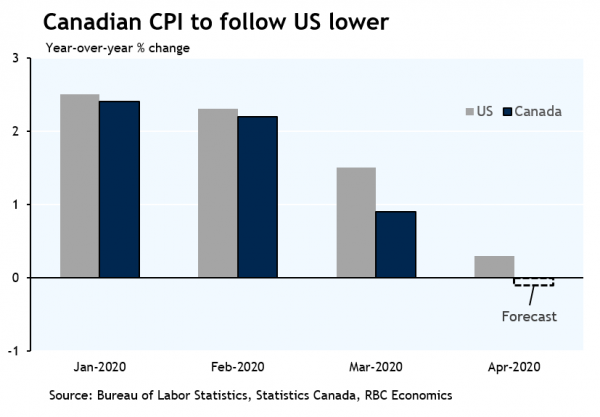

The other aspect of the consumer story is prices, and data there is a bit timelier with next week’s CPI report covering April. Again we have the benefit of having seen the US figures this week, which showed the largest monthly decline in headline inflation since December 2008. Lower gasoline prices and a record drop in core prices (including sharply lower prices for apparel and airfare) were the major factors dragging US inflation lower, and we expect a similar story in Canada with headline CPI likely to slip into negative territory on a year-over-year basis for the first time since 2009. But that figure won’t accurately reflect what Canadian households are spending their money on at present—few people are taking advantage of lower airfares and gas prices. Prices for essentials are of greater concern right now so a sharp increase in food prices in the US, which we expect to see in Canada as well, won’t be welcome news, particularly for the millions of Canadian that have lost their jobs or seen their hours worked cut back significantly. While analysis in the Bank of Canada’s Financial System Review showed government programs like CERB (income support) and CEWS (wage subsidies) will help fund a large portion of core spending (shelter, food and telecom) for many households, some will still have trouble covering even those essentials. Any price increases in those areas—even as official CPI falls sharply—will be a tough pill to swallow.

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals