The Reserve Bank of Australia is scheduled to hold a policy meeting on Tuesday with an announcement expected at 05:30 GMT. A day later, the GDP growth estimate for the first quarter is due at 01:30 GMT, making it an important week for the very bullish looking Australian dollar. However, with the growth picture improving fast and investors already having made up their minds that the virus hit on the Australian economy won’t be as severe as initially feared, next week’s events might not be much of a game changer. That is of course assuming that tensions with China remain tempered.

Is RBA done with QE?

It’s only been a couple of months since it launched its first ever quantitative easing (QE) program and the RBA has already begun winding down its purchases of Australian government bonds. In contrast, other central banks, including next door neighbour – the Reserve Bank of New Zealand – have either increased or are likely to increase their asset purchases in the coming months.

Although the RBA targeting the yield curve as opposed to setting outright targets on the amount of bonds it buys may be one reason why Australia has not had to intervene as heavily in the bond market, another reason is the quicker turnaround in the economic outlook, which has helped bond yields stabilize.

Virus impact not as great as feared

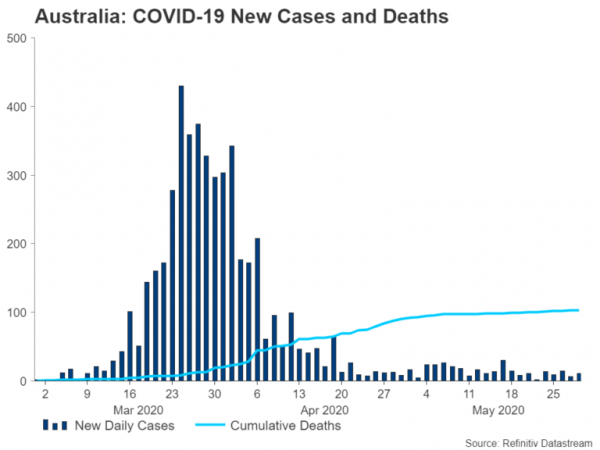

Australia stands out as one of the few countries that managed to contain the spread of the coronavirus very quickly and has one of the lowest per capita death rates. That has allowed it to begin reopening its economy with less risk of a second wave than some other countries that are deemed to have lifted lockdown restrictions too early like the United States. It also means the economic and health toll on the country has not been as high as first predicted.

To give an example, the government recently revised its estimate of how much the JobSeeker scheme – a program of subsidizing workers’ wages to minimize layoffs – will cost, saying it now expects to make savings of A$60 billion as far fewer people have signed up to it than had been originally anticipated. Australia is also in the advantageous position of most of its exports going to China, which was the first country to enter a lockdown and therefore also the first to exit it.

A mild recession?

Add to that the pickup in growth at the start of the year when the US and China had just reached a trade deal, and Q1 GDP is not expected to have declined as steeply in Australia as has been reported in other advanced economies. Forecasts are for economic output to have shrunk by just 0.3% in the March quarter, with year-on-year growth remaining positive at 1.4% but down from 2.2% in Q4. Although there is little doubt that the numbers will get much uglier in Q2 (as suggested by preliminary retail sales numbers for April), there are signs that the downturn will not be as deep as earlier projections.

RBA Governor Philip Lowe has said employment is now expected to decline by 15% instead of 20%, though he does warn that the outlook remains “incredibly uncertain”. What is more certain, however, is that Lowe and his colleagues will keep monetary policy unchanged on Tuesday.

Pressure for more fiscal stimulus

In fact, it’s looking less and less likely that there will be any additional stimulus coming from the RBA. That applies not only to the possibility of further reductions in the cash rate – negative interest rates are almost out of the question in Australia – but also on the likelihood of more QE. While not ruling out increasing QE, Lowe appears to be shifting the burden of supporting the economy onto the government, telling lawmakers “fiscal policy will have to play a greater part than in the past”.

All this has propelled the Australian dollar to 2½-month highs versus the mighty greenback, with the improved risk tone in the broader markets further underlining the currency’s bullish performance since bottoming at 17-year lows in late March.

Aussie on the verge of breaking past 200-day MA

If the RBA does not signal any additional easing as expected and there are no negative surprises in the GDP readings, it should be no trouble for the aussie to break above the 200-day moving average in the $0.6655 area. Clearing this hurdle would set the stage for the $0.6750 and $0.6805 levels, both of which were congested regions in the past.

To the downside, a retreat towards the latest swing low of $0.6504 is possible if the RBA is more dovish than anticipated and/or the GDP data casts doubt about the economy’s resilience.

However, a bigger downside risk is likely to come from any further flare up in US-China tensions that threatens to upset the trade truce, while a souring in Sino-Australian relations cannot be dismissed either. China appears to be increasingly frustrated with Australia’s foreign policy stance, specifically, for backing the US over key issues such as Huawei’s alleged security threat and the Chinese government’s handling of the virus outbreak. With Australia not about to soften its hard-line approach to China, the risk that markets are caught off guard by tougher Chinese retaliation than the limited and selective trade restrictions announced so far is uncomfortably high.

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals