An upcoming summit of EU leaders could decide the fate of the European recovery fund and the direction of Brexit talks, setting up possible stumbling blocks for the euro’s and pound’s rebounds. The pound will also be keeping an eye on the Bank of England’s policy meeting, with more QE looking likely. The Bank of Japan’s and Swiss National Bank’s respective meetings are not expected to be as exciting. But as some of the recent optimism starts to fade, it may ultimately be up to the US retail sales data to determine the market mood, by either refuelling or dashing hopes of economic recovery.

Will the EU deliver on its stimulus pledge?

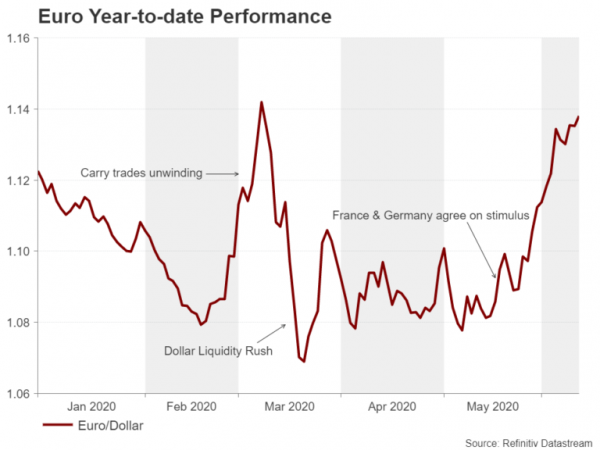

The euro had been drifting aimlessly before a pact between France and Germany for a €500 billion virus rescue fund propelled the currency to three-month highs versus the US dollar. The European Commission has given the Franco-German plan its blessing and has even added a €250 billion loan component to the package, beefing it up to €750 billion. European Union leaders will decide at a Council meeting on June 19 whether to approve the Commission’s proposal and some last-minute haggling is almost certain as fiscally conservative members such as Austria and the Netherlands are not happy about the generous package.

Any downsizing of the rescue fund, which is deemed crucial for aiding the economic recovery of virus-stricken countries like Italy and Spain, is bound to hamper the bloc’s growth prospects and therefore weigh on the euro.

In terms of data releases, it will be relatively quiet but the final readings on Eurozone inflation for May on Wednesday and the ZEW economic sentiment index for June out of Germany on Tuesday might attract some interest.

Bank of England to pump more stimulus

The Bank of England restarted its quantitative easing (QE) program in March, adding £200 billion to its warchest to fight the COVID-19 pandemic. At the current pace of purchases, the latest allotment could be depleted by July and so the BoE will want to replenish it before that happens as the virus crisis is far from over. The Bank is expected to announce an extra £100 billion in asset purchases on Thursday.

However, with more QE already priced in, the main focus for the pound will be whether or not policymakers will flag the possibility of negative rates, especially after Governor Andrew Bailey recently suggested it remains an option in a major U-turn for the Bank.

In the absence of any surprises from the BoE, there’s plenty of UK data to keep investors on edge. Employment numbers on Tuesday should reveal the full scale of job losses in April, when the country was in complete lockdown. But once again, the claimant count might steal the limelight as these are one month more up to date and may show a slight improvement given that some of the restrictions were relaxed in May.

Inflation figures will follow on Wednesday but most of the attention will probably fall on Friday’s retail sales report. Retail sales plunged by a bigger-than-expected 18.5% in April so any easing of the consumption slump in May could be positive for sterling, particularly if Brexit headlines aren’t very supportive for the currency.

British Prime Minister Boris Johnson will reportedly hold talks with the president of the EU Commission, Ursula von der Leyen, on June 15 as the two sides have made virtually no progress in the past few months. Thus, if there’s no breakthrough in the coming days and Johnson continues to rule out an extension of the transition period, which needs to be requested by the end of June, the odds of a no-deal Brexit will shoot up.

BoJ and SNB to stand pat in June

The Bank of Japan will conclude its two-day policy meeting on Tuesday and is not anticipated to make any changes to its key policy tools. However, the Bank may expand its emergency lending programmes to support local businesses hit hard by the pandemic. The yen is unlikely to flicker from the BoJ’s decision, however there may be some reaction to Wednesday’s trade numbers. Japanese exports plummeted by 21.9% year-on-year in April and should the May figures be equally worrying, they may add to the growth jitters amid some doubts about the predictions of a V-shaped recovery.

The Swiss National Bank is also expected to keep policy steady on Thursday, leaving interest rates stuck at a record low of -0.75%. As usual, Chairman Thomas Jordan will make a point of reaffirming the SNB’s determination to keep a cap on the Swiss franc. The safe-haven currency appreciated considerably when the coronavirus started spreading in Europe and it’s widely believed the SNB was intervening heavily to keep the euro from dropping below 1.05 francs. Although the upside pressure on the franc has eased as the virus turmoil subsided, Jordan is unlikely to tone down his tough language on the exchange rate.

Aussie and kiwi may wobble on domestic and Chinese data

With risk appetite looking increasingly fragile, the Australian and New Zealand dollars are in particular danger from any prolonged market sell-off, having enjoyed a strong 2½-month rally. While investors will be taking their cues mostly from the broader market tone, the upcoming data out of China, Australia and New Zealand could play a role in setting the mood.

Chinese indicators on industrial output, retail sales and urban investment will be watched on Monday for signs that the virus recovery in the world’s second largest economy remains on track. In Australia, the May employment report due on Thursday will be important for the aussie as any sharp negative surprises may dent the country’s fast-improving growth outlook. The minutes of the Reserve Bank of Australia’s last policy meeting may grab some attention too on Tuesday.

As for the kiwi, first quarter GDP estimates out of New Zealand may provide some clues as to the likelihood of the Reserve Bank of New Zealand taking rates to negative. New Zealand is one of few countries in the world to declare that it is virus-free so a mild contraction in Q1 would lessen the need for further policy action by the RBNZ.

US retail sales to bounce back but stocks may not care

Wall Street’s dubious rally may have finally run its course this week as traders reassess the chances of a quick recovery from the pandemic. Although for the bulls to take charge again much will depend on the new virus cases in the United States to go back down after a resurgence in some states, the risks from next week’s data will actually be mainly upside ones. The problem is markets may not buy the optimism story this time round as reality begins to bite. That means the dollar could again find itself being a magnet for safety flows, ending its downside correction.

Looking at the key releases for the US next week, the big numbers are all due on Tuesday, comprising of retail sales and industrial output. After a record 16.4% month-on-month drop in April, retail sales in America are forecast to have rebounded by 7% in May. Industrial production is also projected to have begun recovering but by a paltrier rate of 2.4% m/m.

Other indicators are expected to point to an uptick in economic activity as well. Building permits and housing starts due on Wednesday are forecast to have risen in May, while the Empire State and Philly Fed manufacturing gauges, out on Monday and Thursday respectively, will probably show the sector is contracting at a slower pace in June.

If the data fail to revive the risk rally, Fed Chair Jerome Powell’s testimony before Congress might go some way in soothing fears about a weak recovery. Powell spooked markets at his FOMC press conference after he maintained his grim view on the outlook despite the recent green shoots in the US economy. But following the adverse market reaction, Powell might try to backtrack on some of his pessimism when he addresses lawmakers on Tuesday and Wednesday.

Moving north of the border, the Canadian dollar may also not be swayed much by the latest releases. Inflation figures for May will be out Wednesday and retail sales for April will follow on Friday. But with the Bank of Canada likely to hold fire for the time being, global risk sentiment and oil prices will continue to drive the loonie in the coming days.

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals