Sterling remains the weakest one among the major currencies as selloff continues. Though, Dollar and Yen are catching up today while markets turned back into risk-on mode. Commodity currencies are generally firmer as led by Aussie. Even Canadian Dollar shrugs of terrible April retail sales data. Instead, the Loonie is taken up by oil prices.

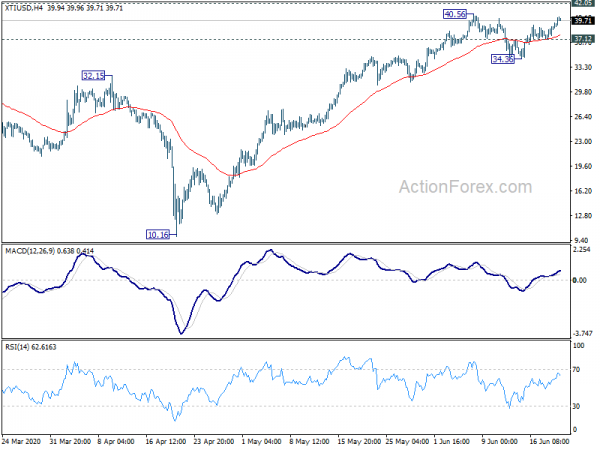

Technically, WTI crude oil’s correction might have completed at 34.36. Break of 40.56 will resume recent strong rally. But for now, we’re not expecting a sustained break of 42.05 key support turned resistance. So upside potential should be limited. Break of 37.12 minor support will turn focus back to 34.36. So, the lift to CAD will likely be temporary. Meanwhile, EUR/GBP has finally breached 0.9054 resistance to resume the rebound from 0.8670. More broad based weakness in the Pound could follow.

In Europe, currently, FTSE is up 1.38%. DAX is up 1.16%. CAC is up 1.52%. Germany 10-year yield is up 0.0015 at -0.438. Earlier in Asia, Nikkei rose 0.55%. Hong Kong HSI rose 0.73%. China Shanghai SSE rose 0.96%. Singapore Strait Times dropped -1.16%. Japan 10-year JGB yield dropped -0.0044 to 0.012.

Canada retail sales dropped -26.4% in April, ex-auto sales dropped -22.0%

Canada retail sales dropped -26.4% mom in April to CAD 34.7B, well worse than expectation of -14.0% mom. Ex-auto sales dropped -22.0% mom, versus expectation of -7.3% mom. Retail sales were down in every sub sector in for the first time in 27 years since May 1993. Motor vehicle and parts dealers sub sector dropped -44.3%, contributing the most to the sales declines.

UK retail sales rose 12% in May, ex-fuel sales rose 10.2%

UK retail sales rose 12.0% mom in May while ex-fuel sales rose 10.2% mom. However, over the year, retail sales dropped -13.1% yoy while ex-fuel sales dropped -9.8% yoy. In quantity bought terms, fuel grew 2.7% mom. Non-store retailing grew 3.8%. Non-food stores grew 5.9%. Food stores dropped slightly by -0.2%.

Gfk Consumer Confidence rose 6 pts to -30 in June, hitting the highest level since March. That’s also the biggest improvement in nearly four years. Expectations on general economic situation over the next 12 months improved by 9 pts to -48, but stayed deeply negative.

Also released in Europe, Germany PPI dropped -0.4% mom, -2.2% yoy in May, versus expectation of -0.3% mom, -2.1% yoy. Eurozone current account surplus narrowed to EUR 14.4B in April.

Japan: Economy still in extremely severe situation but had almost stopped worsening

In the last monthly report of Japan’s Cabinet Office, it’s noted that the economy remained in an “extremely severe situation” but it had “almost stopped worsening”. Private consumption is picking up. However, business investment is in a “weak tone”. Exports are “decreasing rapidly”. Industrial production is “decreasing”. Corporate profits are “decreasing rapidly”. Employment situation is “showing weakness”. Consumer prices are “flat”.

“Concerning short-term prospects, the economy is expected to move toward picking up from an extremely severe situation, supported by the effects of the policies while the socio-economic activities will be resumed gradually with taking measures to prevent the spread of infectious diseases. However, attention should be given to the trend of domestic and overseas infections, and the effects of fluctuations in the financial and capital markets.”

Japan CPI core dropped -0.2% yoy, staying in deflation for second month

Japan national CPI core (all items less fresh food) was unchanged at -0.2% yoy in May, worse than expectation of an improvement to -0.1% yoy. That’s also the second straight month of negative reading. Nevertheless, CPI core-core (all times less fresh food, energy) rose back to 0.4%, up from 0.2% yoy, which might be a sign of relief. Headline CPI (all items) was unchanged at 0.1% yoy.

In the minutes of April 27 BoJ meeting, one membered warned that “the economy might fall into deflation”, “fiscal and monetary authorities could further cooperate with each other”. Another member said BoJ should “consider what was necessary to avoid deflation”. A member said it was appropriate to “revise the forward guidance” with a view to “not allowing deflation to take hold”.

Australia retail sales rose record 16.3% in May, insufficient to recover April’s record decline

Preliminary data showed that Australia retail sales rose 16.3% mom in May. that’s the largest rise on 38 years of record. But that wasn’t enough to recover the record contraction of -17.7% mom in April.

ABS said, “there were large rises for clothing, footwear and personal accessory retailing and cafes, restaurants and takeaway food services, as restrictions on trade were lifted during May. Despite the rises, both these industries remain well down on the levels of May 2019.”

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2362; (P) 1.2464; (R1) 1.2526; More….

GBP/USD’s fall from 1.2813 continues today and intraday bias remains on the downside. Sustained trading below 55 day EMA (now at 1.2473) suggests that whole rebound from 1.1409 has completed. Deeper fall would be seen to 1.2065 support for confirmation. On the upside, break of 1.2587 minor resistance will turn bias back to the upside instead.

In the bigger picture, while the rebound from 1.1409 is strong, there is not enough evidence for rend reversal yet. Down trend from 2.1161 (2007 high) should still resume sooner or later. However, decisive break of 1.3514 should at least confirm medium term bottoming and turn outlook bullish for 1.4376 resistance first.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | National CPI Core Y/Y May | -0.20% | -0.10% | -0.20% | |

| 23:50 | JPY | BoJ Minutes | ||||

| 06:00 | GBP | Retail Sales M/M May | 12.00% | -16.00% | -18.10% | -18.00% |

| 06:00 | GBP | Retail Sales Y/Y May | -13.10% | -22.60% | -22.70% | |

| 06:00 | GBP | Retail Sales ex-Fuel M/M May | 10.20% | -15.00% | -15.20% | -15.00% |

| 06:00 | GBP | Retail Sales ex-Fuel Y/Y May | -9.80% | -18.20% | -18.40% | -18.50% |

| 06:00 | GBP | Public Sector Net Borrowing (GBP) May | 54.5B | 49.3B | 61.4B | 47.8B |

| 06:00 | EUR | Germany PPI M/M May | -0.40% | -0.30% | -0.70% | |

| 06:00 | EUR | Germany PPI Y/Y May | -2.20% | -2.10% | -1.90% | |

| 08:00 | EUR | Eurozone Current Account (EUR) Apr | 14.4B | 27.4B | ||

| 12:30 | CAD | Retail Sales M/M Apr | -26.40% | -14.00% | -10.00% | |

| 12:30 | CAD | Retail Sales ex Autos M/M Apr | -22.00% | -7.30% | -0.40% | |

| 12:30 | USD | Current Account (USD) Q1 | -104B | -101B | -110B | -104B |

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals