The sharp reversal in Chinese stocks is somewhat weighing on global sentiments today. European indices are generally in red while US stocks also open mildly lower. Dollar firms up mildly but upside momentum is unclear for now. Euro is also resilient after ECB stands pat as widely expected and delivers nothing astonishing. On the other hand, Australian Dollar and New Zealand Dollar are paring some of this week’s gains after dissatisfying job and inflation data. Sterling is also soft as data suggests more people have left the job market during the pandemic.

Technically, Yen crosses appear to be picking up some buying in early US session. For today’s session, focus will be on 107.43 minor resistance in USD/JPY, 122.50 minor resistance in EUR/JPY and 1350.58 minor resistance in GBP/JPY. Break of theses levels could prompt some buying into next Asian session. Gold will also be a focus as it’s still inch below 1817.91 short term top. Break will resume larger up trend, and could hint on renewed selling in Dollar elsewhere.

In Europe, currently, FTSE is down -0.24%. DAX is down -0.36%. CAC is down -0.39%. German 10-year yield is down -0.0179 at -0.461. Earlier in Asia, Nikkei dropped -0.76%. Hong Kong HSI dropped -2.00%. China Shanghai SSE dropped -4.50%. Singapore Strait Times dropped -0.95%. Japan 10-year JGB yield dropped -0.0096 to 0.016.

US retail sales rose 7.5% in June, ex-auto sales rose 7.3%, initial jobless claims dropped to 1.3m

US retail sales rose 7.5% mom to USD 524.3B in June, well above expectation of 4.8% rise. Nevertheless, total sales for April through June were still down -8.1% from the same period a year ago. Looking at some details, Ex-auto sales rose 7.3% mom, above expectation of 4.5% mom. Ex-gasoline sales rose 7.0% mom. Ex-auto, ex-gasoline sales rose 6.7% mom.

Initial jobless claims dropped -10k to 1300k in the week ending July 11, slightly above expectation of 1250k. Four-week moving average of initial claims dropped -60k to 1375k. Continuing claims dropped -422k to 17338k. Four-week moving average of continuing claims dropped -738k to 18272k.

Also released, Philly Fed manufacturing survey dropped to 24.1 in July, above expectation of 20.0. Canada ADP employment rose 1042.9k in June. Canada foreign securities purchases dropped to CAD 22.41B in May.

ECB stands pat, activity improved significantly but remains well below pre-pandemic levels

ECB left interest rates unchanged as widely expected. The main refinancing rate is held at 0.00%. Marginal lending facility rate and deposit facility rate are kept at 0.25% and -0.50% respectively. ECB “expects the key ECB interest rates to remain at their present or lower levels until it has seen the inflation outlook robustly converge to a level sufficiently close to, but below, 2% within its projection horizon, and such convergence has been consistently reflected in underlying inflation dynamics.”

The central bank will continue the PEPP asset purchase with a total envelope of EUR 1350B, until “at least the end of June 2021” and “until it judges that the coronavirus crisis phase is over.” Principal payments from maturing securities under PEPP will be reinvested until “at least the end of 2022.” APP net purchase will continue at a monthly pace of EUR 20B, together with the additional EUR 120B temporary envelope, until the end of the year.

In the post meeting press conference, President Christine Lagarde said “incoming data and survey results suggest that economic activity improved significantly in May and June from its trough in April”. But indicators remain “well below” pre-pandemic levels. The recovery is “in its early stages” and “remain uneven across sectors and jurisdictions”. GDP is still expected to have “contracted even further overall” in Q2.

There were signs of recovery in consumption and rebound in industrial output. But “subdued labour market conditions and precautionary household saving are weighing on consumer spending”. “Weak business prospects and high uncertainty are dampening investment”. “Weakness in the global economy is hampering foreign demand”. Activity is expected to rebound in Q3 but “uncertainty about the overall speed and scale of the rebound remains high.”

UK unemployment rate unchanged at 3.9% in May

UK unemployment rate was unchanged at 3.9% in the three months to May, much better than expectation of a surge to 4.7%. Regarding income, average earnings excluding bonus rose 0.3% 3moy in May, slightly above expectation of 0.6%. Average earnings including bonus dropped -3moy, better than expectation of -0.5%.

ONS noted: “The relative flatness of the unemployment figures may seem surprising, given that there are notable decreases in the number in employment. However, some initial exploratory analysis has suggested that a larger than usual proportion of those leaving employment are not currently looking for a new job and therefore becoming economically inactive, rather than unemployed.”

Claimant counts dropped -28.1k in June, versus expectation of 250k rise. Nevertheless, since March, the claimant count has increased 112.2%, or 1.4m.

Australia unemployment rate jumped to 22-yr high, PM unveils trainer support

Australia employment rose 210.8k to 12.33m in June, above expectation of 112.5k rise. Full time job dropped -38.1k to 8.49m. Part-time jobs, on the other hand, surged 249k to 3.84m. Unemployment rise rose 0.4% to 7.4%, matched expectations. That’s the highest level since November 1998. Nevertheless, the positive sign is that participation rate jumped back by 1.3% to 64.0%, as people are back in the job markets.

Prime Minister Scott Morrison unveiled today a new AUD 2B JobTrainer plan aimed at reskilling and upskilling Australians. He said, the program “doesn’t just support those who have left the workforce through no fault of their own, but that also is supporting school leavers as well at the end of this year.”

AUD/JPY weakens mildly after the release but stays above 4 hour 55 EMA. We’re viewing the sideway price actions from 72.52 as the second leg of the pattern form 76.78 high only. That is, we’d expect at least another decline before the pattern completes. Break of 73.98 support should target 72.52 and below.

New Zealand CPI dropped -0.5% qoq in Q2, affirming more RBNZ easing

New Zealand CPI dropped -0.5% qoq in Q2, matched expectations. That’s the first quarterly fall in inflation since December 2015 quarter. Petrol prices dripped -12% qoq, biggest quarterly decline since December 2008 quarter. Annually, CPI slowed to 1.5% yoy, down from 2.5% yoy, matched expectations too. Stats NZ prices senior manager Aaron Beck said “the COVID-19 pandemic has created a lot of volatility and uncertainty. These have resulted in some large price fluctuations as well as several measurement challenges.”

The data suggests that inflation could move back to target slower than RBNZ is expecting. The development reaffirms the easing case for the central bank ahead. It’s generally expected to expand the asset purchase program in the coming months. As RBNZ is also preparing the financial system for, negative rate is still a likely option to be adopted next year.

China GDP grew 3.2% yoy in Q2, June retail sales weak

China’s GDP grew 3.2% yoy in Q2, above expectation of 2.5% yoy. Barring the steep -6.8% contraction in Q1, Q2’s figure is still the worst on record. For H1 as a whole, the economy contracted -1.6% yoy from a year earlier. On quarter-on-quarter basis, GDP rose 11.5% qoq in Q2, higher than expectation of -9.6% qoq, and sufficient to reverse the -9..8% qoq decline in Q1.

Also from China, retail sales dropped -1.8% yoy in June, below expectation of 0.3% yoy rise. Industrial production rose 4.8% yoy in June, slightly above expectation of 4.7% yoy. Fixed asset investment dropped -3.1% ytd yoy in June, slightly above expectation of -3.2% ytd yoy.

Suggested reading on China: China Recorded Strong Recovery in 2Q20 but Domestic Demand Remained Weak. Risks Skewed to Downside in Second Half

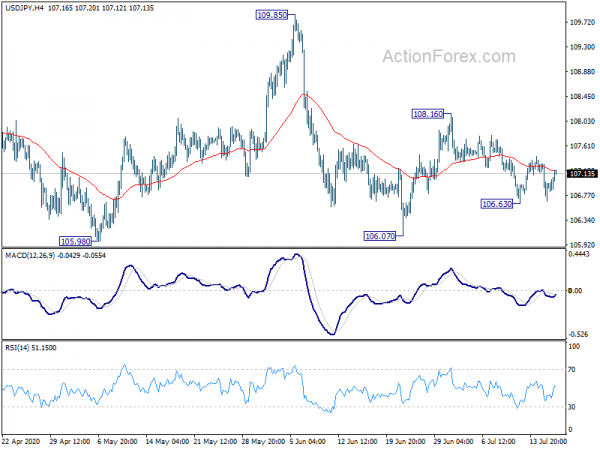

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 106.64; (P) 106.97; (R1) 107.28; More…

USD/JPY recovers ahead of 106.63 support but stays inside range below 108.16 resistance. Intraday bias remains neutral first. On the downside, below 106.63 will target 106.07. Break there will extend the whole pattern from 111.71 and target 61.8% retracement of 101.18 to 111.71 at 105.20. On the upside, however, break of 108.16 will resume the rebound from 106.07 and target 109.85 resistance instead.

In the bigger picture, USD/JPY is still staying in long term falling channel that started back in 118.65 (Dec2016). Hence, there is no clear indication of trend reversal yet. The down trend could still extend through 101.18 low. However, sustained break of 112.22 should confirm completion of the down trend and turn outlook bullish for 118.65 and above.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | CPI Q/Q Q2 | -0.50% | -0.50% | 0.80% | |

| 22:45 | NZD | CPI Y/Y Q2 | 1.50% | 1.50% | 2.50% | |

| 01:00 | AUD | Consumer Inflation Expectations Jul | 3.20% | 3.30% | ||

| 01:30 | AUD | Employment Change Jun | 210.8K | 112.5K | -227.7K | |

| 01:30 | AUD | Unemployment Rate Jun | 7.40% | 7.40% | 7.10% | |

| 02:00 | CNY | GDP Y/Y Q2 | 3.20% | 2.50% | -6.80% | |

| 02:00 | CNY | Retail Sales Y/Y Jun | -1.80% | 0.30% | -2.80% | |

| 02:00 | CNY | Industrial Production Y/Y Jun | 4.80% | 4.70% | 4.40% | |

| 02:00 | CNY | Fixed Asset Investment YTD Y/Y Jun | -3.10% | -3.20% | -6.30% | |

| 06:00 | GBP | Claimant Count Change Jun | -28.1K | 250.0K | 528.9K | |

| 06:00 | GBP | Claimant Count Rate Jun | 7.30% | 7.80% | ||

| 06:00 | GBP | ILO Unemployment Rate (3M) May | 3.90% | 4.70% | 3.90% | |

| 06:00 | GBP | Average Earnings Excluding Bonus 3M/Y May | 0.70% | 0.60% | 1.70% | |

| 06:00 | GBP | Average Earnings Including Bonus 3M/Y May | -0.30% | -0.50% | 1.00% | |

| 09:00 | EUR | Eurozone Trade Balance (EUR) May | 8B | 5.0B | 1.2B | 1.6B |

| 11:45 | EUR | ECB Interest Rate Decision | 0% | 0% | 0% | |

| 12:30 | EUR | ECB Press Conference | ||||

| 12:30 | CAD | ADP Employment Change Jun | 1042.9K | 208.4K | ||

| 12:30 | CAD | Foreign Securities Purchases (CAD) May | 22.41B | 49.04B | ||

| 12:30 | USD | Retail Sales M/M Jun | 7.50% | 4.80% | 17.70% | 18.20% |

| 12:30 | USD | Retail Sales ex Autos M/M Jun | 7.30% | 4.50% | 12.40% | 12.10% |

| 12:30 | USD | Initial Jobless Claims (Jul 10) | 1300K | 1250K | 1314K | 1310K |

| 12:30 | USD | Philadelphia Fed Manufacturing Survey Jul | 24.1 | 20 | 27.5 | |

| 14:00 | USD | Business Inventories May | -2.10% | -1.30% | ||

| 14:00 | USD | NAHB Housing Market Index Jul | 59 | 58 | ||

| 14:30 | USD | Natural Gas Storage | 48B | 56B |

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals