Dollar tumbled again overnight after the rather uneventful FOMC rate decision. But selling slowed a little bit in Asian session today. Nevertheless, the greenback remains the worst performer for the week. Commodity currencies are actually not performing well, with New Zealand and Canadian Dollar down against most for the week. Sterling and Euro are the stronger ones, taking turns to be the best performer. Movements in the markets could re-accelerate with busy calendar and heave weight economic data scheduled for today and tomorrow.

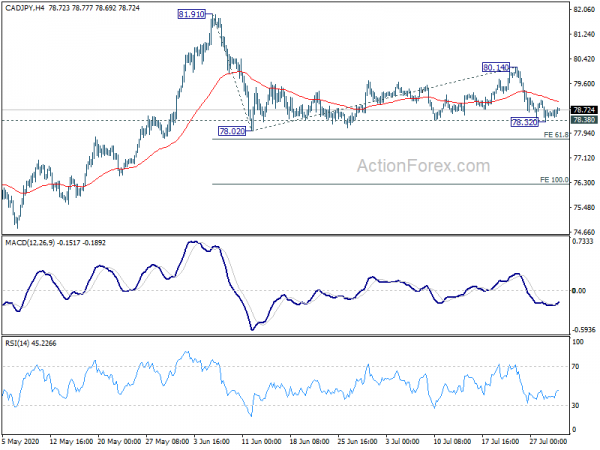

Technically, Yen crosses would be interest to watch, with clear divergence. On the one hand, both EUR/JPY and GBP/JPY drew notable support from 4 hour 55 EMA and rebounded. Focuses are back on 124.29 and 136.62 temporary tops respectively. Break will extend recent rally. On the other hand, AUD/JPY and CAD/JPY struggles in very tight range above 74.87 and 78.38 temporary lows respectively and look vulnerable. Break of these levels will extend recent decline. We’d probably find out which way is the way for Yen pretty soon.

In Asia, currently, Nikkei is down -0.16%. Hong Kong HSI is up 1.05%. China Shanghai SSE is up 0.09%. Singapore Strait Times is down -1.56%. Japan 10-year JGB yield is up 0.0012 at 0.022. Overnight DOW rose 0.61%. S&P 500 rose 1.24%. NASDAQ rose 1.35%. 10-year yield dropped -0.002 to 0.579, staying below 0.6 handle.

Fed stands pat, notes economic activity and employment have picked up somewhat

Overnight, Fed kept federal funds rate unchanged at 0-0.25% as widely expected. It also maintained the pledge to use its “full range of tools to support the U.S. economy in this challenging time, thereby promoting its maximum employment and price stability goals.” Also, Fed will continue to ” increase its holdings of Treasury securities and agency residential and commercial mortgage-backed securities at least at the current pace”.

Fed acknowledged that “economic activity and employment have picked up somewhat in recent months but remain well below their levels at the beginning of the year. Weaker demand and significantly lower oil prices are holding down consumer price inflation. Overall financial conditions have improved in recent months, in part reflecting policy measures to support the economy and the flow of credit to U.S. households and businesses.”

NASDAQ up 1.35% after Fed, consolidation continues with bullishness intact

US stocks closed higher overnight after Fed maintained the pledge to keep monetary policy loose and use all its tools to support the economy. Yet strength was limited as Chair Jerome Powell acknowledged that “data are pointing to a slowing in the pace of the recovery”.

“Recent labor market indicators point to a slowing in job growth, particularly among smaller businesses,” he added, and consumer surveys “look like they may be softening again now.” “There’s probably going to be a long tail where a large number of people are struggling to get back to work…. There will be a need both for more support from us and for more fiscal policy.”

NASDAQ ended up 1.35% or 140.85 pts at 10542.94. Current development suggests that it’s merely in a near term sideway consolidation pattern, with near term bullishness intact. The record run should resume sooner rather than later as long as 10182.46 support holds. However, break of this support will argue that deeper correction is underway to 55 day EMA (now at 9953.05) and below.

Australia Kennedy: Victoria coronavirus outbreak pulls us back

Australia’s Victoria reported a record 723 daily coronavirus cases for the past 24 hours as situation in the second most populous state continued to worsen despite returning to lockdown. Australia Treasury Secretary Steven Kennedy said that the outbreak in Victoria “pulls us back” and together with new Queensland border restrictions, the national economy will be hurt more than forecast in last week’s federal budget update.

Kennedy said, “further constraints, be they through movement or through the extension of the six-week measures that the Victorian government announced, will mean growth will be lower, employment will be lower and unemployment will be higher. Beyond that, of course, people can lose confidence and have concerns about what they’re seeing unfolding, even in other parts of the country.

He added that 75% of Victorian firms currently receiving the JobKeeper wage subsidies were likely to remain on the scheme beyond the September renewal deadline. Meanwhile, Q2 GDP is expected to contract -7% and road to recovery will be long and unpredictable. New South Wales’ management of the virus would now be crucial for the economy.

Also from Australia, import price index dropped -1.9% qoq in Q2 versus expectation of -2.5% qoq. Building permits dropped -4.9% mom in June versus expectation of 0.0% mom.

New Zealand ANZ business confidence: Bounces are fun but nearly run its course

New Zealand ANZ Business Confidence rose to -31.8 in July, up from June’s -34.4, but down from prelim reading of -29.8. Confidence was worst in agriculture at -54.5 and beat in retail at -22.6 while all sector stayed negative. Own activity outlook rose to -8.9, up notably from June’s -25.9, but also revised down to -6.8. Activity was worst in agriculture again at -15.2 but best in services at -5.0.

ANZ said “bounces are fun, but this one has probably nearly run its course.” It warned that “unfortunately, that blow is coming; it’s inevitable.” Border will remain closed for the rest of the year, which is “one of the few certainties in our economic forecasts at the moment”. That means “big hole in economic activity, centred on tourism and the foreign education sector.” Also, the blow “won’t be felt evenly” with the country “split into two economies – the tourism-dependent regions and the rest”.

Looking ahead

The economic calendar is rather busy today. Germany will release Q2 GDP, July employment and CPI. Swiss will release KOF economic barometer. Eurozone will release unemployment rate and economic sentiment, as well as ECB monthly bulletin. Later in the day, US will release Q2 GDP and jobless claims.

EUR/JPY Daily Outlook

Daily Pivots: (S1) 123.25; (P) 123.52; (R1) 124.02; More….

EUR/JPY recovers after drawing support from 4 hour 55 EMA but stays below 124.29/43 resistance zone. Intraday bias remains neutral first. Overall, further rally will remain in favor as long as 121.96 support holds. On the upside, firm break of 124.43 will resume the rise from 114.42 to 61.8% projection of 114.42 to 124.43 from 119.31 at 125.49. On the downside, however, break of 121.96 will turn bias to the downside for 119.31 support instead.

In the bigger picture, whole down trend from 137.49 (2018 high) could have completed at 114.42 already. Rise from 114.42 would target 61.8% retracement of 137.49 to 114.42 at 128.67 next. Sustained break there will pave the way to 137.59 (2018 high). This will remain the preferred case for now, as long as 55 day EMA (now at 120.80) holds. However, sustained break of 55 day EMA will revive medium term bearishness for another low below 114.42 at a later stage.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Building Permits M/M Jun | 0.50% | 35.60% | 41.70% | |

| 23:50 | JPY | Retail Trade Y/Y Jun | -1.20% | -6.50% | -12.50% | |

| 01:00 | NZD | ANZ Business Confidence Jul | -31.8 | -29.8 | ||

| 01:30 | AUD | Import Price Index Q/Q Q2 | -1.90% | -2.50% | -1.00% | |

| 01:30 | AUD | Building Permits M/M Jun | -4.90% | 0.00% | -16.40% | -15.80% |

| 06:00 | EUR | Germany GDP Q/Q Q2 P | -9.00% | -2.20% | ||

| 07:00 | CHF | KOF Economic Barometer Jul | 72.5 | 59.4 | ||

| 07:55 | EUR | Germany Unemployment Rate Jul | 6.50% | 6.40% | ||

| 07:55 | EUR | Germany Unemployment Change Jul | 45K | 69K | ||

| 08:00 | EUR | Italy Unemployment Rate Jun | 8.50% | 7.80% | ||

| 08:00 | EUR | ECB Economic Bulletin | ||||

| 09:00 | EUR | Eurozone Unemployment Rate Jun | 7.70% | 7.40% | ||

| 09:00 | EUR | Eurozone Economic Sentiment Indicator Jul | 75.7 | |||

| 09:00 | EUR | Eurozone Industrial Confidence Jul | -17.2 | -21.7 | ||

| 09:00 | EUR | Eurozone Consumer Confidence Jul | -15 | -15 | ||

| 09:00 | EUR | Eurozone Services Confidence Jul | -22.9 | -35.6 | ||

| 09:00 | EUR | Eurozone Business Climate Jul | -2.26 | |||

| 12:00 | EUR | Germany CPI M/M Jul P | -0.20% | 0.60% | ||

| 12:00 | EUR | Germany CPI Y/Y Jul P | 0.20% | 0.90% | ||

| 12:30 | USD | Initial Jobless Claims (Jul 24) | 1450K | 1416K | ||

| 12:30 | USD | GDP Annualized Q2 A | -35.00% | -5.00% | ||

| 12:30 | USD | GDP Price Index Q2 A | 1.20% | 1.60% | ||

| 14:30 | USD | Natural Gas Storage | 25B | 37B |

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals