Rising household demand continued to drive the economic recovery in June after an initial 4.5% bounce back in GDP in May. Statistics Canada already provided an advance estimate that retail sales rose another 24.5% in June. That would leave sales already slightly (~2%) above year-ago levels in that month, and is broadly consistent with our own tracking of credit and debit card purchases, as well an earlier-reported pickup in vehicle sales.

Despite industry reports are that auto sales continued to recover in July, further marginal gains in retail spending will be increasingly harder to come by with sales already closer to “normal” pre-COVID levels. Our tracking of card purchases is still pointing to further spending growth more broadly as well, albeit at a slower pace than in May and June.

Industrial supply chains have been slower to restart, but manufacturing sales picked up sharply in June – and were probably boosted by a further recovery in auto production in July. A jump in export and import flows in June means that wholesale trade probably increased significantly in the month as well.

Home resale markets blazed in the summer months

Reports from regional real-estate boards suggest that the Canadian Real Estate Association’s monthly update will show housing markets heated up significantly in the summer. Home resale activity was already reported as up by double-digits from a year ago in most of Canada’s major markets. New listings also increased in July, though by less than sales. That shift in market power in sellers’ favour is keeping a floor under near-term price trends.

Housing starts from the past week show similar momentum in new building activity, with starts rising to their highest level in two and a half years – and strong permit issuance suggesting there is still more strength in building activity in the near-term pipeline.

Elevated household saving and pent-up demand boost spending

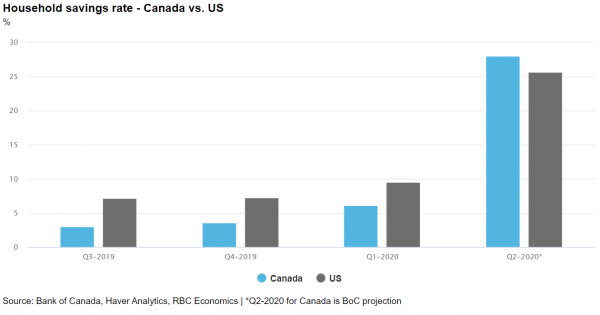

Much of the resilience in household spending to-date is thanks to unprecedented government income support programs, both in Canada and abroad. Household income probably increased significantly in Canada in Q2 (as was already reported in the United States) despite an unprecedented downturn in labour markets.

Overall spending was still very low in the second quarter with containment measures keeping consumers close to home – notwithstanding sharply higher e-commerce purchases. The net result was likely a sharp spike in the household saving rate in Canada in Q2, similar to that reported in the United States. So some of the initial bounce-back in spending to-date, particularly in housing markets, likely reflects pent-up demand from foregone earlier purchases.

Long-run outlook is still cloudy, with hot pace of recovery to cool

The real test for household spending will come once unprecedented policy supports begin to wind down later this year. Labour markets are still exceptionally soft, and are unlikely to bounce back fully before those supports begin to expire.

To-date, although spending on goods has bounced back surprisingly quickly, spending on services remains sharply reduced – particularly for anything travel/tourism-related. Notably, there were still over 400k fewer workers in accommodation & food services and entertainment jobs in July relative to February. Those remaining lost jobs will probably be among the slower to return as long as the virus threat remains.

In the US, negotiations to replace the previous $600/week federal top-up to unemployment benefits remain deadlocked in Congress, and details regarding the executive orders signed by president Trump to extend those benefits, but at a reduced rate, are still not clear.

In Canada, the first applicants of the CERB program may have already received their last $2000 cheque and details regarding plans to help the transition into either CEWS or (a likely modified version of) EI are still pending.

We continue to expect the labour market weakness to persist, and the Canadian economy to still be running at 5% below its year-ago level by the end of 2020.

And soft demand will exert downward pressure on prices, eventually…

Growth in prices likely slowed in July as well. We expect the all-item CPI index to have grown a moderate 0.4% from a year ago in July, down from 0.7% in June although still up from sub-zero readings in March and April. Gasoline prices ticked up from May and we expect food price growth held at close to 3% on a year-over-year basis. Excluding food & energy products, we assume year-over-year price growth slowed a bit in July.

We also normally see a sizeable seasonal bump for inter-city transportation and travel services this time of year. But there are obvious questions about how ‘normal’ price patterns will be this year given many travel activities have been significantly interrupted by COVID related travel restrictions. Early data that tracks aircraft movements points to a healthier than expected recovery in domestic air travel, with the volume back up to 80% of its pre-COVID peak by end of July already. But international travel is still down more than 80%. The Bank of Canada’s core measures held closer to the 2% inflation target in June, but we expect them to tick lower in July.

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals