U.S. Highlights

- Fiscal policy (or lack thereof) drove much of the news cycle this week. On the same day the Federal Reserve Chair made the case for more fiscal support, President Trump tweeted that negotiations were being cut off.

- Trump changed his mind later in the week, and talks appear to have restarted. Still a deal will require the support of Senate Republicans, and with just over three weeks until the election, time is running out.

Canadian Highlights

- This week’s employment report was encouraging, showing an acceleration in employment growth in September. The Canadian economy added 334k jobs in the month, most of them full time and the unemployment fell 1.2 percentage points to 9.0%.

- The pace of homebuilding eased in September. Housing starts dropped to a still-healthy 209k (annualized) units in September, down from August’s robust pace of 261.5k.

- In his speech this week, Governor Tiff Macklem acknowledged that policy actions have helped to keep financial risks at bay so far. However, long-term risks remain and with the economic recovery entering a slower and more uncertain phase, policy markets will need to remain both supportive and vigilant to a potential build up in vulnerabilities.

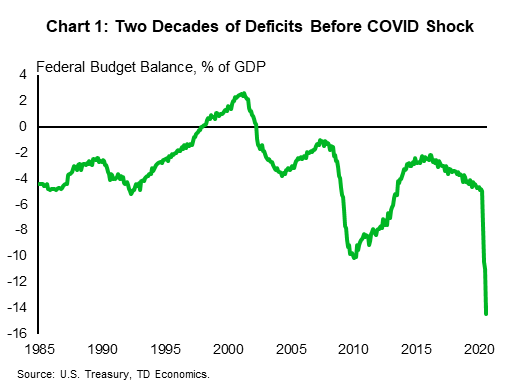

U.S. – Fiscal Deal or No Deal

It was a raucous week news wise and in financial markets. As it has been for the past several weeks, fiscal policy (or lack thereof) was front and center. Arriving back to the White House early in the week, President Trump tweeted that stimulus talks were being cut off and any fiscal package would have to wait until after election. Later in the week he reversed course, suggesting the possibility of standalone bills on specific measures, such as support for airlines, the Payroll Protection Program or stimulus checks. The latest word is that the administration is now pushing hard for a more comprehensive deal.

Assuming a deal can be done between the Trump administration and the House Democrats, it may still have difficulty passing the Senate. On Friday, Senate Majority Leader, Mitch McConnell expressed his doubts, saying he still thought a deal was unlikely over the next three weeks.

For his part, Federal Reserve Chair Powell made a strong case for additional fiscal support in a speech this week. He noted that despite the rebound seen so far, the economy is still in a precarious state. Any slowing in the pace of recovery at this stage risks triggering “typical recessionary dynamics, as weakness feeds on weakness.” It would also exacerbate inequalities, a tragedy in the Fed chair’s view, “especially in light of our country’s progress on these issues in the years leading up to the pandemic.”

In pressing for additional fiscal supports, the Fed Chair noted that there is little risk of doing too much in the current environment. With interest rates falling to record lows, the cost of servicing the federal debt is shrinking even as the stock grows. While the U.S. budget deficit is hardly on a sustainable path – something the Fed Chair also recognized – it has not been for some time. The time will come for hard decisions on the longstanding mismatch between what the federal government takes in revenue and what it spends. However, the near and present risk of cascading bankruptcies and permanent job losses is clearly much bigger than the risk of a future debt crisis.

Indeed, there is much to laud in the fiscal policy response to date. Looking back on the last several months, the success of monetary and fiscal policy in supporting the recovery is everywhere to be seen in the economic data. The support to household income allowed for a swift recovery in goods consumption and production. Retail sales are now higher than pre-pandemic levels – a forecast few would have had a few months ago. While the recovery in service consumption has lagged, this is due to health crisis itself, which makes it impossible to go back to normal in close-contact businesses like restaurants, gyms, movie theatres.

For what its worth, our economic forecast assumed a modest fiscal deal that allows for another round of relief checks and additional unemployment benefits of $300 per week (half the amount under the CARES Act) to be delivered before the end of the year. This still seems possible – the fireworks this week notwithstanding – but if it does not occur, economic growth could get dangerously close to stall speed in the quarters ahead. Activity could still bounce back, particularly if a vaccine becomes widely available by mid-year, but the downside risks are clearly higher the longer it takes for policy makers to reach an agreement.

Canada – Recovery Continues, But Rising COVID Cases Pose a Risk

North American financial markets were upbeat this week on the news that U.S. congressional leaders and White House officials have rekindled their negotiations on a comprehensive economic support package. Additional fiscal help is much-needed stateside, and the renewed negotiations are the latest sign that the two sides are feeling the pressure to act. Increased optimism that the stimulus package will eventually be passed helped to boost equities and crude, with TSX ending the week 2.1% higher and the benchmark WTI prices rising above $40/barrel.

In Canada, significant government help for firms and households remains largely in place, helping to support the economic recovery. This week all eyes were on the September employment report, which, encouragingly, showed an acceleration in job growth in the month, with employment rising by 334k (2.1%). The unemployment rate declined for the fourth consecutive month, falling by 1.2 percentage points to 9.0%. Since April, more than three quarters of the jobs lost during the initial lockdown phase have now been recovered, an impressive outcome particularly when compared to the U.S. where the recovery rate is only slightly above the 50% threshold.

In other good news, with schools re-opening, employment improved for parents in September. Both mothers and fathers saw employment return to pre-COVID levels. Nonetheless, the number of mothers working less than half their usual hours was still 70% higher than what it was in February. The recovery is also uneven in other ways: employment for youth and older adults, as well as low-wage workers still remains significantly below pre-pandemic levels.

While the labor market continued to advance in September, homebuilding activity took a step back. After rapid gains over the summer months, housing starts dropped to 209k (annualized) units in September, still solid, but down from August’s robust 261.5k pace. The decline was driven by multi-starts (-27% m/m), while single-detached starts increased 3.4% (Chart 2). Going forward, strong pre-construction sales and low mortgage rates should ensure that starts remain robust through next year.

All in all, economic data released this week suggests the Canadian economy remained on the recovery path in September. However, the initial burst in activity brought about by re-opening is now behind us. The next phase of the recovery will likely be more challenging, particularly amid the resurgence of COVID-19 cases in Canada’s two largest provinces. This has already led to additional restrictions and renewed calls for increased social distancing from the provinces’ leaders.

This sentiment was corroborated by Bank of Canada Governor Tiff Macklem in a speech this week. He acknowledged that thanks to the policy actions of government and regulators, financial risks – such as widespread credit losses – have so far been contained. Still, he warned that vigilance and policy support will be needed as the economy continues through the recuperation phase of the recovery.

U.S: Upcoming Key Economic Releases

U.S. Consumer Price Index- September

Release Date: October 13, 2020

Previous: 0.4% m/m, 1.3% y/y

TD Forecast: 0.2% m/m, 1.4% y/y

Consensus: 0.2% m/m, 1.4% y/y

We view the COVID-19 shock as disinflationary, on balance, but with positive as well as negative effects, as will likely be evident once again in the September CPI report: We expect strength in used vehicle prices to lead to an above-trend 0.3% rise in the core index, but with an unwinding of earlier strength in food-at-home prices helping hold the rise in the overall CPI to 0.2%. Demand for used vehicles has been boosted by efforts to avoid mass transit. Our forecast implies 1.8% y/y for core prices, up from 1.7% in August and as low as 1.2% in June but still down from 2.4% in February. The y/y change in the overall index probably rose to 1.4% from 1.3% in August; it was 2.3% in February.

U.S. Retail Sales – September

Release Date: October 16, 2020

Previous: 0.6% m/m total, 0.7% ex-autos

TD forecast: 1.5% m/m total, 1.6% ex autos

Consensus: 0.8% total, 0.4% ex-autos

Retail sales will probably show broad-based acceleration in September, even with employment growth slowing and fiscal stimulus fading. Strengthening has already been reported for auto sales. We suspect the seasonal factors are exaggerating gains, with consumer spending patterns changing in the COVID-19 crisis, but the report should add to already strong Q3 GDP growth calculations. Not seasonally adjusted retail sales will likely show a sizable decline in September.

Canada: Upcoming Key Economic Releases

Canadian Manufacturing Sales – August

Release Date: October 16

Previous: 7.0%

TD Forecast: -1.5%

Consensus: NA

Manufacturing sales are forecast to decline by 1.5% in August on a pullback in motor vehicle shipments that will offset gain elsewhere and put a temporary halt to the recovery. This comes after a return to full auto production levels in July, and a 6.8% decline in motor vehicle exports. Ex-transportation shipments should see modest gains, consistent with the continued recovery in manufacturing PMI and labour market strength. Real manufacturing sales should post a slightly larger decline, owing to higher factory prices in August.

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals