Sterling turns generally lower in quiet holiday-mood trading today. Sellers are back in control as there appears to be no path out of the Brexit trade talk deadlocks yet. And, time is running out clearly. Overall, Yen and Dollar remain the worst performing ones of the week, on general optimism over coronavirus vaccines. New Zealand Dollar remains the strongest while Australian Dollar shrugs off China’s tariffs and stays the second best.

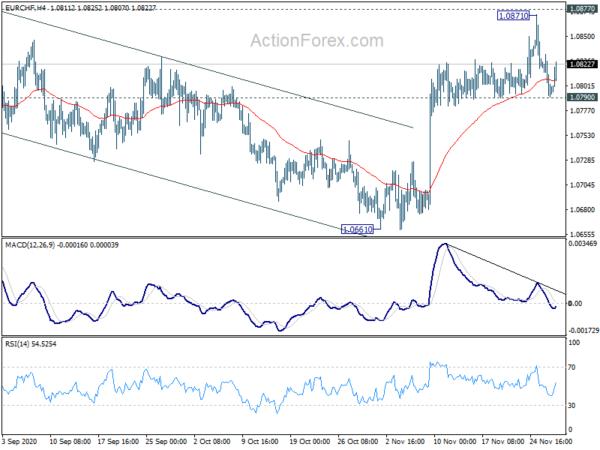

Technically, Yen’s rebound attempt quickly lost momentum while Swiss Franc is also reversing. In particular, EUR/CHF bounces off 1.0790 support, keeping near term outlook cautiously bullish. EUR/GBP also rebounds ahead of 0.8861 key support level. We’ll see if EUR/USD could ride on theses rebounds and break through 1.2011 key resistance level….. well… next week.

In Europe, currently, FTSE is down -0.50%. DAX is up 0.24%. CAC is up 0.52%. German 10-year yield is up 0.0039 at -0.581. Earlier in Asia, Nikkei rose 0.40%. Hong Kong HSI rose 0.28%. China Shanghai SSE rose 1.14%. Singapore Strait Times dropped -0.06%. Japan 10-year JGB yield rose 0.0057 to 0.030.

EU Barnier: Same significant divergences persist with UK

EU chief Brexit negotiation Michel Barnier confirmed that he’s travelling to London this evening to continue in-person trade talks with the UK over the weekend. but he also noted, “same significant divergences persist”. An unnamed EU official said Barnier told national diplomats that “the gaps on level playing-field, governance and fisheries remain large,”

On the UK side, Prime Minister Boris Johnson said, “Clearly there are substantial and important differences still to be bridged but we’re getting on with it.” He added, “the likelihood of a deal is very much determined by our friends and partners in the EU — there’s a deal there to be done if they want to do it.”

ECB Villeroy: Recalibration must focus on quality of monetary policy transmission

ECB Governing Council member Francois Villeroy de Galhau said, in face of “prolonged uncertainty” due to resurgence in coronavirus infections, “our first objective must be keeping very favorable financing conditions as long as necessary”.

But he also added, “recalibration of instruments must focus in particular not only on the level of monetary support, but also on the duration, flexibility and efficient targeting, in short, the quality of monetary policy transmission.”

Eurozone economic sentiment dropped to 87.6

Eurozone Economic Sentiment Indicate dropped markedly to 87.6 in November, down from 91.1, but beat expectation of 86.5. Employment Expectations Indicator posted the second fall in a row, down -3.3 pts to 86.6. Amongst the largest euro-area economies, the ESI plunged in Italy (-8.7) and France (-4.8), while its losses were more contained in Germany (-2.8) and Spain (-2.0). The Netherlands bucked the trend with a moderate improvement in sentiment (+1.0).

Looking at some details, industry confidence dropped from -9.2 to -10.1. Services confidence dropped from -12.1 to -17.3. Consumer confidence dropped from -15.5 to -17.6. Retail trade confidence dropped from -6.9 to -12.7. Construction confidence dropped from -8.3 to 9.3.

France GDP grew 18.7% in Q3, consumer spending rose 3.7% mom in Oct

According to the second estimate, France GDP grew 18.7% in Q3, after the -13.8% decline back in Q2. Despite the strong bounce, GDP remained well below the level it had before the pandemic. In volume terms, GDP was down -3.9% yoy.

In October, consumer spending rose 3.7% mom, much better than expectation of -1.0% mom decline. It’s 2.7% yoy higher than the level a year ago. This increase was driven by a sharp rise in food consumption (+7.1%) and energy expenditure (+6.4%). Manufactured good purchases were almost stable (-0.1%). In November CPI rose 0.2% yoy, up from 0.0% yoy in October.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3318; (P) 1.3358; (R1) 1.3394; More…

GBP/USD continues to lose upside momentum as seen in 4 hour MACD and intraday bias is turned neutral. On the upside, above 1.3397 will target 1.3498 resistance first. Decisive break of 1.3482 high will resume whole rise from 1.1409. Further rally should then be seen to 61.8% projection of 1.1409 to 1.3482 from 1.2675 at 1.3956 next. On the downside,break of 1.3195 support will turn bias back to the downside, to extend the consolidation from 1.3482 with another falling leg.

In the bigger picture, focus stays on 1.3514 key resistance. Decisive break there should also come with sustained trading above 55 month EMA (now at 1.3308). That should confirm medium term bottoming at 1.1409. Outlook will be turned bullish for 1.4376 resistance and above. Nevertheless, rejection by 1.3514 will maintain medium term bearishness for another lower below 1.1409 at a later stage.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Tokyo CPI Core Y/Y Nov | -0.70% | -0.70% | -0.50% | |

| 7:00 | EUR | Germany Import Price Index M/M Oct | 0.30% | 0.10% | 0.30% | |

| 7:45 | EUR | France Consumer Spending M/M Oct | 3.70% | -1.00% | -5.10% | -4.40% |

| 7:45 | EUR | France GDP Q/Q Q3 | 18.70% | 18.20% | 18.20% | |

| 10:00 | EUR | Eurozone Economic Sentiment Indicator Nov | 87.6 | 86.5 | 90.9 | 91.1 |

| 10:00 | EUR | Eurozone Industrial Confidence Nov | -10.1 | -10.8 | -9.6 | -9.2 |

| 10:00 | EUR | Eurozone Services Sentiment Nov | -17.3 | -15 | -11.8 | -12.1 |

| 10:00 | EUR | Eurozone Consumer Confidence Nov | -17.6 | -18 | -17.6 | -15.5 |

| 10:00 | EUR | Eurozone Business Climate Nov | -0.63 | -0.74 |

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals