Dollar trades generally higher today as rebound continues. Yen and Swiss Franc are following as the next strongest so far. Commodity currencies are generally lower as led by Australian Dollar. The picture might imply risk aversion but there is no clear selloff in Asian markets. At the time of writing, Asian stocks are just mixed, with Japan on holiday.

It remains to be seen if some traders are jumping out of risk markets early, on pandemic concerns. Japan reported on Sunday a new coronavirus variant from Brazilian travelers. The UK variant was found in Northern Mexico already. China recorded the biggest daily infections in over five months. But there’s no information yet on whether the coronavirus cases found in China was the same as the one in Wuhan a year ago, which started the pandemic. Or, some new variants are re-entering into China.

Technically, EUR/USD’s break of 1.2214 support last week was a sign of bottoming in Dollar. USD/JPY’s break of 103.89 resistance was another. Focuses will be on 1.3428 support in GBP/USD, 0.7641 support in AUD/USD. 0.8918 resistance in USD/CHF and 1.2797 resistance in USD/CAD.

In Asia, currently, Hong Kong HSI is up 0.72%. China Shanghai SSE is down -0.23%. Singapore Strait Times is down -0.32%. Japan is on holiday today.

China CPI turned positive in Dec, PPI deflation flowed to -0.4% yoy

China’s CPI turned positive to 0.2% yoy, up from -0.50% yoy, above expectation of 0.1% yoy. Core CPI, excluding food and energy, stood at 0.4% yoy, down from 0.5% yoy.

“Ahead of New Year’s Day and the Spring Festival, consumer demand increased, and feed costs also rose,” said Dong Lijuan, a senior statistician at the NBS. “At the same time, affected by unusual weather and rising costs, the CPI turned from a decline into an increase.”

PPI dropped to -0.4% yoy in December, up from November’s -1.5% yoy, higher than expectation of -0.8% yoy. That’s also the slowest factory gate deflation since last February.

Australia retail sales rose 7.1% mom in Nov, up 2.6% excluding Victoria

Australia retail sales grew 7.1% mom in November, revised up from preliminary result of 7.0% mom, followed 1.4% mom rise in October. Ben James, Director of Quarterly Economy Wide Surveys, said: “The rise is led by Victoria (22.4%) as Melbourne retail stores were able to trade for a full month in November. Excluding Victoria, turnover rose 2.6%.”

Other states and territories to record an increase in turnover were Queensland (4.5%), New South Wales (2.3%), Western Australia (1.2%), Tasmania (3.4%), the Australian Capital Territory (2.5%), and the Northern Territory (2.2 per cent). The brief lockdown in South Australia (-0.2%) led to a relatively flat result, as falls in most industries were offset by a rise in food sales.

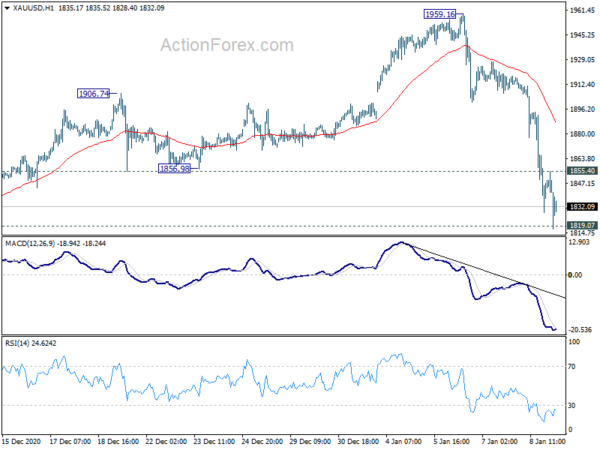

Gold dips to 1817, decline slowing a bit but no bottoming yet

Gold edged lower to 1817.05 in Asian session but selloff appears to be slowing a little bit. Though, bias will remain on the downside as long as 1865.40 minor resistance holds. Current fall from 1959.16 is seen as another falling leg in the corrective pattern from 2075.18. Break of 1819.05 would target 1764.31 support and below.

Economic data to start to take back the spotlights

With most political risks now behind, focus should gradually turn back to economic data. Eurozone Sentix investor confidence, Canada business outlook survey, Fed’s Beige book report and U of Michigan consumer sentiment could catch more attention then others. Meanwhile, US CPI, jobless claims and retail sales, UK GDP and productions, Eurozone productions and China trade balance will also be watched. ECB will also release monetary policy meeting accounts.

- Monday: Australia retail sales; China CPI, PPI; Eurozone Sentix investor confidence; Canada BoC business outlook survey.

- Tuesday: Japan current account, economy watchers sentiment; US NFIB small business index.

- Wednesday: Japan M2, machine tool orders; Germany WPI; Italy industrial production, Eurozone industrial production; US CPI, Fed’s Beige Book report.

- Thursday: Japan machine orders, PPI; China trade balance; UK RICS house balance; ECB meeting accounts; US jobless claims, import prices.

- Friday: Japan tertiary industry index; UK GDP, productions, trade balance; Eurozone trade balance; US retail sales, PPI, industrial production, business inventories, U of Michigan sentiment.

AUD/USD Daily Report

Daily Pivots: (S1) 0.7730; (P) 0.7764; (R1) 0.7800; More…

AUD/USD dips further today but stays above 0.7641 support. Intraday bias remains neutral first and another rise remains mildly in favor. On the upside, break of 0.7819 will resume larger up trend form 0.5506 to 0.7413 from 0.6991 at 0.8170. However, break of 0.7641 will indicate short term topping, on bearish divergence condition in 4 hour MACD. Intraday bias will be turned back to the downside for deeper correction to 0.7461 support first.

In the bigger picture, whole down trend from 1.1079 (2001 high) should have completed at 0.5506 (2020 low) already. Rise from 0.5506 could either the start of a long term up trend, or a corrective rise. Reactions to 0.8135 key resistance will reveal which case it is. But in any case, medium term rally is expected to continue as long as 0.7413 resistance turned support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | AUD | Retail Sales M/M Nov | 7.10% | 7.00% | 7.00% | |

| 01:30 | CNY | CPI Y/Y Dec | 0.20% | 0.10% | -0.50% | |

| 01:30 | CNY | PPI Y/Y Dec | -0.40% | -0.80% | -1.50% | |

| 09:30 | EUR | Eurozone Sentix Investor Confidence Jan | 2 | -2.7 | ||

| 14:30 | CAD | BoC Business Outlook Survey |

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals