Dollar’s rebound gains much momentum in early US session with a little help from much stronger than expected retail sales data. Canadian Dollar is following as second strongest for today, riding on rally resumption in oil prices. On the other hand, Euro is suffering some steep selling together with Swiss Franc, and Sterling. Yen is mixed for the momentum, awaiting some guidance from stock markets and risk sentiments.

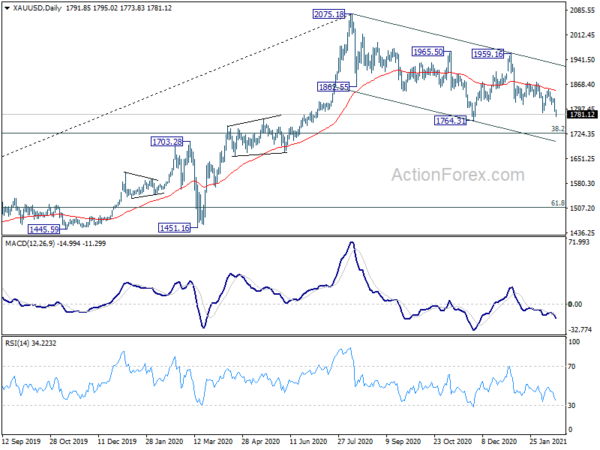

Technically, EUR/USD’s break of 1.2080 support dampened out original bullish view and argues that corrective pattern form 1.2348 is extending with another falling leg. Similarly, USD/CHF’s break of 0.8939 minor resistance also indicates that corrective pattern from 0.8756 is extending with another rising leg. Adding to that, Gold also dives further after taking out 1800 handle yesterday. It’s now extending the third leg of the corrective pattern from 2075.18 high, to 1764.31 support and below.

In Europe, currently, FTSE is down -0.15%. DAX is down -0.48%. CAC is down -0.03%. Germany 10-year yield is down -0.003 at -0.346. Earlier in Asia, Nikkei dropped -0.58%. Hong Kong HSI rose 1.10%. Singapore Strait Times dropped -0.51%. Japan 10-year JGB yield rose 0.0182 to 0.098, another step closing to 0.1% handle.

US retail sales surged 5.3% in Jan, ex-auto sales rose 5.9%

US retail sales rose sharply by 5.3% mom to USD 568.2B in January, above expectation of 1.1% mom. Ex-auto sales rose 5.9% mom, higher than expectation of 0.9% mom. Ex-gasoline sales rose 5.4% mom. Ex-auto, ex-gasoline sales rose 6.1% mom.

Also released, PPI rose 1.3% mom, 1.7% yoy in January, above expectation of 0.4% mom, 0.9% yoy. PPI core rose 1.2% mom, 2.0% yoy, above expectation of 1.2% mom, 1.2% mom.

Canada CPI at 0.6% mom, 1.0% yoy in Jan, above expectation

Canada CPI rose 0.6% mom in January above expectation of 0.5% mom. Annually, CPI accelerated to 1.0% yoy, up from 0.7% yoy, above expectation of 0.9% yoy.

CPI common was unchanged at 1.3% yoy, below expectation of 1.4% yoy. CPI median slowed to 1.4% yoy, down from 1.8% yoy, below expectation of 1.8% yoy. CPI trimmed rose to 1.8% yoy, up from 1.6% yoy, above expectation of 1.6% yoy.

UK CPI rose to 0.7% yoy in Jan, core CPI unchanged at 1.4% yoy

UK CPI accelerated to 0.7% yoy in January, up from 0.6% yoy, above expectation of 0.5% yoy. Core CPI was unchanged at 1.4% yoy, above expectation of 1.3% yoy. RPI also accelerated to 1.4% yoy, up from 1.2% yoy, above expectation of 1.2% yoy. PPI input came in at 0.7% mom, 1.3% yoy. PPI output was at 0.4% mom, -0.2% yoy. PPI output core was at 0.3% mom, 1.4% yoy.

RBA Kent: Aussie could be 5% higher without RBA policy

RBA Assistant Governor Christopher Kent said in a speech that some factors have contributed to the appreciation of the Australian Dollar since November. The factors include “general improvement in the outlook for global growth” and a “marked increase in many commodity prices”.

Iron ore prices “has increased by around 40 per cent” since early November. And, “historical relationships with commodity prices would have implied a much larger appreciation of the Australian dollar than what’s actually occurred,” he added.

“While history only provides a rough guide, this difference suggests that the Bank’s policy measures have contributed to the Australian dollar being as much as 5 per cent lower than otherwise (in trade-weighted terms),” Kent said.

Australia leading index rose to 4.48% in Jan, points to above trend growth in 2021

Australia Westpac leading index rose from 4.24% to 4.48% in January. The data points to “above trend growth in the Australian economy through 2021”. Westpac expects 4% GDP growth in 2021, led by consumer spending, which contributes to around 3% to the overall growth rate.

As for RBA policy, Westpac expects the bond buying program to be extended beyond October. Yield curve control will be maintained through 2021. However, the Term Funding Facility will be “largely scaled back” after June.

Japan’s export surged 6.4% yoy in Jan, imports dropped -9.5% yoy

Japan’s export rose 6.4% yoy to JPY 5780B in January. By region, exports to China jumped a massive 37.5% yoy, largest annual gain since April 2010. Exports to the US, on the other hand, dropped -4.8% yoy. Imports dropped -9.5% yoy to JPY 6104B. Trade deficit came in at JPY -324B.

In seasonally adjusted term, exports rose 4.4% mom to JPY 6362B. Imports rose 6.9% mom to JPY 5969B. Trade surplus narrowed to JPY 393B, below expectation of JPY 480B.

Also from Japan, machine orders unexpectedly rose 5.2% mom in December, versus expectation of -6.2% mom decline.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2077; (P) 1.2124; (R1) 1.2152; More…

EUR/USD’s strong break of 1.2080 minor support argues that recovery from 1.1951 has completed at 1.2168. The development also suggests that corrective pattern from 1.2348 is extending with a third leg down. Intraday bias is back on the downside for 1.1951 support first. Break there will target 100% projection of 1.2348 to 1.1951 from 1.2168 at 1.1771. For now, risk will stay on the downside as long as 1.2168 resistance holds.

In the bigger picture, rise from 1.0635 is seen as the third leg of the pattern from 1.0339 (2017 low). Further rally could be seen to cluster resistance at 1.2555 next, (38.2% retracement of 1.6039 to 1.0339 at 1.2516). This will remain the favored case as long as 1.1602 support holds. We’d be alerted to topping sign around 1.2516/55. But sustained break there will carry long term bullish implications.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | AUD | Westpac Leading Index M/M Jan | 0.30% | 0.10% | ||

| 23:50 | JPY | Trade Balance (JPY) Jan | 0.39T | 0.48T | 0.48T | 0.51T |

| 23:50 | JPY | Machinery Orders M/M Dec | 5.20% | -6.20% | 1.50% | |

| 07:00 | GBP | CPI M/M Jan | -0.20% | -0.40% | 0.30% | |

| 07:00 | GBP | CPI Y/Y Jan | 0.70% | 0.50% | 0.60% | |

| 07:00 | GBP | Core CPI Y/Y Jan | 1.40% | 1.30% | 1.40% | |

| 07:00 | GBP | RPI Y/Y Jan | 1.40% | 1.20% | 1.20% | |

| 07:00 | GBP | RPI M/M Jan | -0.30% | 0.50% | 0.60% | |

| 07:00 | GBP | PPI Input M/M Jan | 0.70% | 0.70% | 0.80% | |

| 07:00 | GBP | PPI Input Y/Y Jan | 1.30% | 1.00% | 0.20% | |

| 07:00 | GBP | PPI Output M/M Jan | 0.40% | 0.20% | 0.30% | |

| 07:00 | GBP | PPI Output Y/Y Jan | -0.20% | -0.60% | -0.40% | |

| 07:00 | GBP | PPI Core Output M/M Jan | 0.30% | 0.10% | ||

| 07:00 | GBP | PPI Core Output Y/Y Jan | 1.40% | 1.20% | ||

| 13:30 | CAD | CPI M/M Jan | 0.60% | 0.50% | -0.20% | |

| 13:30 | CAD | CPI Y/Y Jan | 1.00% | 0.90% | 0.70% | |

| 13:30 | CAD | CPI Common Y/Y Jan | 1.30% | 1.40% | 1.30% | |

| 13:30 | CAD | CPI Median Y/Y Jan | 1.40% | 1.80% | 1.80% | |

| 13:30 | CAD | CPI Trimmed Y/Y Jan | 1.80% | 1.60% | 1.60% | |

| 13:30 | USD | Retail Sales M/M Jan | 5.30% | 1.10% | -0.70% | -1.00% |

| 13:30 | USD | Retail Sales ex Autos M/M Jan | 5.90% | 0.90% | -1.40% | -1.80% |

| 13:30 | USD | PPI M/M Jan | 1.30% | 0.40% | 0.30% | |

| 13:30 | USD | PPI Y/Y Jan | 1.70% | 0.90% | 0.80% | |

| 13:30 | USD | PPI Core M/M Jan | 1.20% | 0.20% | 0.10% | |

| 13:30 | USD | PPI Core Y/Y Jan | 2.00% | 1.20% | 1.20% | |

| 14:15 | USD | Industrial Production M/M Jan | 0.40% | 1.60% | ||

| 14:15 | USD | Capacity Utilization Jan | 74.80% | 74.50% | ||

| 15:00 | USD | Business Inventories Dec | 0.50% | 0.50% | ||

| 15:00 | USD | NAHB Housing Market Index Feb | 83 | 83 | ||

| 19:00 | USD | FOMC Minutes |

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals