Euro is under some pressure today after a heavy ECB official indicated the readiness to response to surging yields. But Swiss Franc is not too far behind. The forex markets are mixed elsewhere. Dollar is currently the stronger one, together with Aussie and Sterling. Meanwhile, Kiwi is the weaker commodity currencies. Canadian Dollar is mixed, as partly dragged down by oil price.

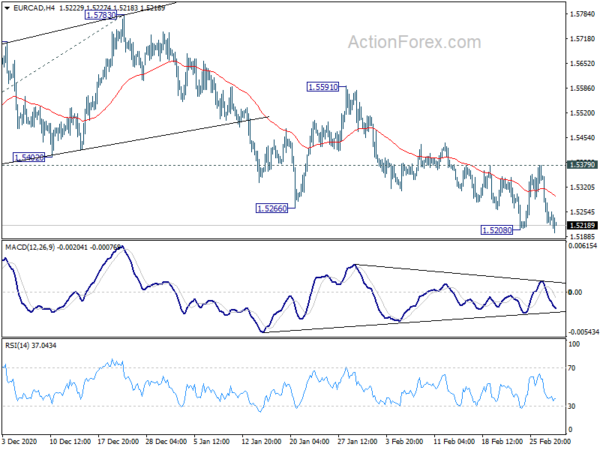

Technically, a focus is now on how far and widely Euro’s fall would develop into. EUR/JPY and EUR/GBP appear to be safe for now as both are holding well above 127.48 support and 0.8537 low. But 1.1951 support in EUR/USD and 1.5250 support in EUR/AUD could be tested. EUR/CAD has indeed breached 1.5208 temporary low already, after completing the recovery at 1.5379.

In Europe, currently, FTSE is up 0.53%. DAX is up 0.41%. CAC is up 0.46%. German 10-year yield is up 0.0136 at -0.320. Earlier in Asia, Nikkei dropped -0.86%. Hong Kong HSI dropped -1.21%. China Shanghai SSE dropped -1.21%. Singapore Strait Times rose 0.03%. Japan 10-year JGB yield dropped -0.0264 to 0.130.

Canada GDP grew 0.1% mom in Dec, advanced information points to 0.5% mom rise in Jan

Canada GDP grew 0.1% mom in December, matched expectations, following 0.8% mom rise in November. That’s the eighth consecutive monthly increase. Still total economic activity was about -3% below February’s pre-pandemic level. Goods-producing industries were up 0.6% mom while services-producing industries edged down -0.1% mom. 12 of 20 industrial sectors grew in the month.

At the same time, advanced information indicates an approximate 0.5% mom increase in real GDP in January. The wholesale trade, manufacturing and construction sectors led the increase while retail trade declined.

ECB de Guindos open to recalibration on negative impact of rising yields

ECB Vice-President Luis de Guindos told Portuguese newspaper Público, “We will have to see whether this increase in nominal yields will have a negative impact on financing conditions.”

“If we reach the conclusion that it will, then we are totally open to recalibrating our programme, including the envelope of our Pandemic Emergency Purchase Programme if necessary,” he added. “We have room for manoeuvre, and we have ammunition.”

Eurozone CPI unchanged at 0.9% yoy in Feb, core CPI slowed to 1.1% yoy

Eurozone CPI was unchanged at 0.9% yoy in February, below expectation of 1.0% yoy. CPI core slowed to 1.1% yoy, down from 1.4% yoy, matched expectations.

Looking at the main components, food, alcohol & tobacco is expected to have the highest annual rate in February (1.4%, compared with 1.5% in January), followed by services (1.2%, compared with 1.4% in January), non-energy industrial goods (1.0%, compared with 1.5% in January) and energy (-1.7%, compared with -4.2% in January).

From Germany, unemployment rose 9k in January, versus expectation of 15k decline. Retail sales dropped -4.5% mom in January, below expectation of 0.9% mom.

RBA stands pat, recovery stronger than earlier expected

RBA left monetary policy unchanged as widely expected. Cash rate and 3-year yield target are held at 0.10%. Parameters of the Term Funding Facility and the government bond purchase program are kept unchanged too. The central bank also keep the pledge to “maintaining highly supportive monetary conditions until its goals are achieved”. The conditions for raising cash rate is not expected to be met “until 2024 at the earliest”.

The bond purchases were “brought forward this week to assist with the smooth functioning of the market”. A cumulative AUD 74B of government bonds has been purchased under the initial AUD 100B program. A further AUD 100B will be purchases after the current program completes. And RBA is “prepared to do more if that is necessary”.

Globally, RBA noted that longer-term bond yields increased “considerably over the past month”. That “partly reflects a lift in expected inflation over the medium term to rates that are closer to central banks’ targets”. The movement in yields have been associated with volatility in other asset prices including foreign exchange rates, Australian Dollar “remains in the upper end of the range of recent years”.

Australian economic recovery is “well under way” and has been “stronger than was earlier expected”. GDP is expected to grow3.5% over both 2021 and 2022. Also GDP is expected to return to its end-2019 level “by the middle of this year”. But wage and prices pressures “subdued” and are expected to “remain so for some years”. CPI is expected to be at 1.25% over 2021 and 1.50% over 2022. CPI inflation is expected to “rise temporarily because of the reversal of some COVID-19-related price reductions.”

Also from Australia, current account surplus widened to UAD 14.5B in Q4, above expectation of AUD 13.B. Building permits dropped -19.4% mom in January, versus expectation of -3.0% mom.

Suggested readings on RBA:

RBNZ Hawkesby: We are in no hurry to remove stimulus

RBNZ Assistant Governor Christian Hawkesby said today that the central bank is in no rush to remove monetary stimulus. “Markets are keen to get ahead of central banks but there will inevitably be false starts,” he said. “And that is why we are seeing some of the volatility in bond markets at the moment.”

“Our approach is to continually remind markets that we are going to be patient, and we are in no hurry to remove stimulus,” he emphasized. The comment was consistent with the central bank’s message last week, about keeping easy monetary policy for a prolonged period of time.

While New Zealand has reopened earlier than many other countries, “there are pockets, regions and sectors that are still struggling”, Hawkesby said.

Also from New Zealand, terms of trade index rose 1.3% in Q4, matched expectations.

Japan unemployment at unchanged at 2.9%, job availability ratio improved

Japan unemployment rate was unchanged at 2.9% in January, slightly better than expectation of 3.0%. Job availability ratio rose to 1.10, up from 1.05. The data suggested that new job offers are rebounding, leading to resumption of recovery later in the quarter. “We can’t deny that the impact of the pandemic was felt but concerns that the state of emergency would worsen (the jobless rate) did not materialize,” an official of the internal affairs ministry said.

Capital spending dropped -4.8% in Q4, much worse than expectation of -2.0%. That’s the third straight quarter of decline, after the sharp -10.6% contraction in Q3. The data argued there might be downward revision in the 12.7% annualized Q4 GDP growth.

Also released, monetary base rose 19.6% yoy in February, versus expectation of 20.1% yoy rise.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9093; (P) 0.9126; (R1) 0.9181; More….

USD/CHF rises to as high as 0.9192 so far today. Break of 100% projection of 0.8756 to 0.9044 from 0.8869 at 0.9157 suggests some upside acceleration. Firm break of 0.9181 support turned resistance will target 161.8% projection at 0.9335 next. On the downside, break of 0.9093 resistance turned support is needed to indicate short term topping. Otherwise, further rally will remain in favor in case of retreat.

In the bigger picture, decline from 1.0237 is seen as the third leg of the pattern from 1.0342 (2016 high). There is no clear sign of completion yet. Next target will be 138.2% projection of 1.0342 to 0.9186 from 1.0237 at 0.8639. In any case, break of 0.9295 resistance is needed to signal medium term bottoming. Otherwise, outlook will remain bearish in case of rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Terms of Trade Index Q4 | 1.30% | 1.30% | -4.70% | |

| 23:30 | JPY | Unemployment Rate Jan | 2.90% | 3.00% | 2.90% | |

| 23:50 | JPY | Capital Spending Q4 | -4.80% | -2.00% | -10.60% | |

| 23:50 | JPY | Monetary Base Y/Y Feb | 19.60% | 20.10% | 18.90% | |

| 00:30 | AUD | Current Account Balance (AUD) Q4 | 14.5B | 13.1B | 10.0B | 10.7B |

| 00:30 | AUD | Building Permits M/M Jan | -19.40% | -3.00% | 10.90% | 12.00% |

| 03:30 | AUD | RBA Interest Rate Decision | 0.10% | 0.10% | 0.10% | |

| 07:00 | EUR | Germany Retail Sales M/M Jan | -4.50% | 0.90% | -9.60% | |

| 08:55 | EUR | Germany Unemployment Change Jan | 9K | -15K | -41K | -37K |

| 08:55 | EUR | Germany Unemployment Rate Jan | 6% | 6% | 6% | |

| 10:00 | EUR | Eurozone CPI Y/Y Feb P | 0.90% | 1.00% | 0.90% | |

| 10:00 | EUR | Eurozone CPI Core Y/Y Feb P | 1.10% | 1.10% | 1.40% | |

| 13:30 | CAD | GDP M/M Dec | 0.10% | 0.10% | 0.70% | 0.80% |

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals