The forex markets turned mixed in Asian session. Dollar is taking a breather after yesterday’s selloff, but remains the worst performing one for the week. Australian Dollar retreats mildly after strong employment data. But the Aussie is still the second strongest for the week, just after New Zealand Dollar. Canadian Dollar attempted to follow upside breakout in oil price overnight, but there is no follow through buying so far. Attentions will now turn to a bunch of data from the US, including retail sales, and jobless claims.

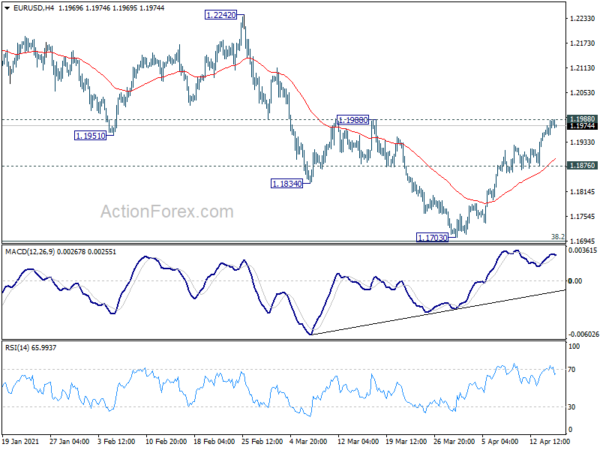

Technically, EUR/USD is now pressing 1.1988 resistance. Decisive break there will add to the case that correction from 1.2348 (Jan high) has completed with three waves down to 1.1703. Further rise would be seen to 1.2242/2348 resistance zone. To gauge the underlying strength in Euro, we’ll see if EUR/CHF could extend the rebound from 1.0973 and accelerates towards 1.1116/1149 resistance zone. To gauge Dollar’s weakness, we’ll see if USD/CAD could break through 1.2501 support and accelerates towards 1.2363 low.

In Asia, at the time of writing, Nikkei is up 0.01%. Hong Kong HSI is down -0.94%. China Shanghai SSE is down -1.03%. Singapore Strait Times is up 0.06%. Japan 10-year JGB yield is down -0.0024 at 0.088, back below 0.1% handle. Overnight, DOW rose 0.16%. S&P 500 dropped -0.41%. NASDAQ dropped -0.99%. 10-year yield rose 0.015 to 1.638.

Fed: Economic activity accelerated to a moderate pace

Fed Beige Book report noted that national economic activity “accelerated to a moderate pace from late February to early April. Consumer spending “strengthened” and reports on tourism were “more upbeat”. Auto sales also “grew”. The picture in non-financial services “generally improved”. Manufacturing activity “expanded further” despite widespread supply chain disruptions. Outlooks were “more optimistic” thanks to acceleration in vaccinations.

Employment growth “picked up” with most Districts noting “modest to moderate” increase in headcounts. But pace of job growth “varied by industry”. Employment expectations were “generally bullish” and wage growth “accelerated slightly over all”. Prices “accelerated slightly” with many Districts reporting “moderate price increase”. There were “widespread reports” of increased selling prices too.

Fed Powell: Tapering would in all likelihood be well before rate hikes

Fed Chair Jerome Powell said yesterday that “we will reach the time at which we will taper asset purchases when we have made substantial further progress towards our goals”. He added that tapering would, “in all likelihood be before, well before,” Fed considers rate hikes and “that is the sense of the guidance”.

Separately, Vice Chair Richard Clarida said that if inflation expectations “drift up persistently”, policy would need to be adjusted. For example, if wages start to grow consistently faster than productivity, that would set the stage for a “sustained increase in inflation”. He added, “we are going to be very attentive to what we are seeing in the nexus between wages, productivity, prices and markups.

New York Fed President John Williams said, “the economy is coming back pretty strong right now.” “There’s a lot of things that are uncertain,” he added. “But I think the economy will be able to get back to full strength.” But he also acknowledged, “we’re a little bit in a race between the vaccinations and the new variants of the coronavirus.”

BoJ downgrades assessment of Hokkaido and Tohoku regions

In BoJ’s Regional Economic Report, assessments for two regions, Hokkaido and Tohoku, were downgraded. Hokkaido’s economy has “remained in a severe situation” and has been “more or less flat. Tohoku’s economy has “picked up as a trend” but impact of resurgence of coronavirus appears to be “growing recently”. Assessments of Hokuriku, Kanto-Koshinetsu, Tokai, Kinki, Chugoku, Shikoku and Kyushu-Okinawa were left unchanged.

Overall, BoJ said, “many regions — while noting that their economy had remained in a severe situation due to the impact of the novel coronavirus (COVID-19), primarily in consumption of services — reported that, on the whole, it had been on a pick-up trend or had started to pick up.”

Governor Haruhiko Kuroda said at the quarterly meeting of regional branch managers, “the pace of the recovery will be modest as caution over the pandemic remains.” Also, “services consumption will remain under pressure for the time being due to a resurgence in COVID-19 infections since last autumn.”

Australia employment grew 70.7k in Mar, hours worked back at pre-pandemic level

Australia employment grew 70.7k in March, double of expectation of 35.0k. However, growth was mainly driven by part-time jobs, which increased 91.5k to 4.20m. Full-time jobs contracted by -20.8k to 8.87m. Unemployment rate dropped to 5.6%, down from 5.8%, better than expectation of 5.7%. participation rate rose 0.2% to 66.3%, a record high. Monthly hours worked rose 2.2% mom or 38m hours, back to pre-pandemic levels.

Looking ahead

Germany will release March CPI final. Canada will release ADP employment and manufacturing sales. US will release Empire State and Philly Fed manufacturing index, retail sales, jobless claims, industrial production, business inventories and NAHB housing index.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1957; (P) 1.1972; (R1) 1.1996; More….

Intraday bias in EUR/USD stays on the upside for the moment. Decisive break of 1.1988 resistance should affirm the case that correction from 1.2348 has completed at 1.1703. Further rally should then be seen to retest 1.2242/2348 resistance zone. On the downside, below 1.1876 minor support will dampen the bullish case, and turn bias back to the downside for 38.2% retracement of 1.0635 to 1.2348 at 1.1694.

In the bigger picture, rise from 1.0635 is seen as the third leg of the pattern from 1.0339 (2017 low). Further rally could be seen to cluster resistance at 1.2555 next, (38.2% retracement of 1.6039 to 1.0339 at 1.2516). This will remain the favored case as long as 1.1602 support holds. However, sustained break of 1.1602 will argue that whole rise from 1.10635 has completed. Deeper fall would be seen to 61.8% retracement of 1.0635 to 1.2348 at 1.1289.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 1:00 | AUD | Consumer Inflation Expectations Apr | 3.20% | 4.10% | ||

| 1:30 | AUD | Employment Change Mar | 70.7K | 35.0K | 88.7K | |

| 1:30 | AUD | Unemployment Rate Mar | 5.60% | 5.70% | 5.80% | |

| 6:00 | EUR | Germany CPI M/M Mar F | 0.50% | 0.50% | ||

| 6:00 | EUR | Germany CPI Y/Y Mar F | 1.70% | 1.70% | ||

| 12:30 | CAD | Manufacturing Sales M/M Feb | 3.10% | |||

| 12:30 | CAD | ADP Employment Change Mar | -100.8K | |||

| 12:30 | USD | Empire State Manufacturing Index Apr | 18.2 | 17.4 | ||

| 12:30 | USD | Initial Jobless Claims (Apr 9) | 700K | 744K | ||

| 12:30 | USD | Retail Sales M/M Mar | 5.50% | -3.00% | ||

| 12:30 | USD | Retail Sales ex Autos M/M Mar | 4.80% | -2.70% | ||

| 12:30 | USD | Philadelphia Fed Manufacturing Survey Apr | 43 | 51.8 | ||

| 13:15 | USD | Industrial Production M/M Mar | 2.80% | -2.20% | ||

| 13:15 | USD | Capacity Utilization Mar | 75.60% | 73.80% | ||

| 14:00 | USD | Business Inventories Feb | 0.40% | 0.30% | ||

| 14:00 | USD | NAHB Housing Market Index Apr | 83 | 82 | ||

| 14:30 | USD | Natural Gas Storage | 20B |

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals