The forex markets are staying in consolidative mode this week so far. Aussie is steady in tight range after RBA stood pat as widely expected, even though GDP forecast was upgraded. Dollar is recovering again as the retreat overnight didn’t last long. Canadian Dollar and Yen also trade with a slightly firmer tone. On the other hand, European majors are trading mildly softer.

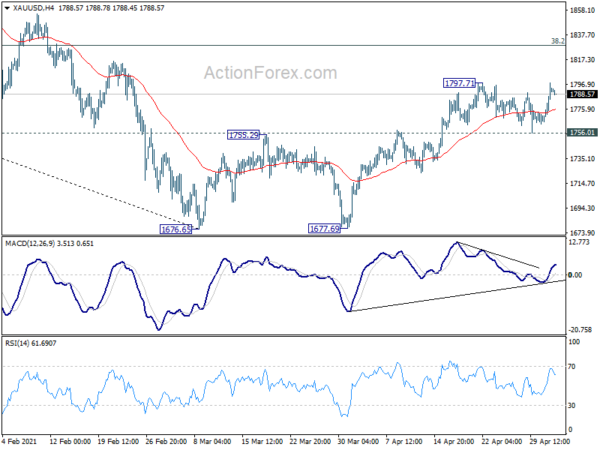

Technically, consolidative mode will probably continue for a while more. As noted before, while Dollar retreated, there is no clear sign of bullish reversal. Two levels to watch include 0.9180 minor resistance in USD/CHF and 0.7676 minor support in AUD/USD. As long as these levels holds, Dollar’s selloff should resume sooner rather than later. Meanwhile, Gold is pressing 1797.71 near term resistance for now. Break will resume the rise from 1677.69, and would be a sign of Dollar weakness.

In Asia, Hong Kong HSI is up 0.25%. Singapore Strait Times is down -0.18%. Japan and China are still on holiday. Overnight, DOW rose 0.70%. S&P 500 rose 0.27%. NASDAQ dropped -0.48%. 10-year year yield dropped -0.024 to 1.607.

RBA stands pat, upgrades GDP forecasts further

RBA maintained monetary policy settings as widely expected. Cash rate and 3-year yield target are held at 0.10%. Parameters of the Term Funding Facility and bond purchases are held unchanged too. It also maintained that the condition for raising the cash rate is unlikely to be reached until 2024 at the earliest.

At its “July meeting”, RBA will consider whether to retail April 2024 bond as the 3-year yield target, or shift to next maturity, “at its July meeting”. But the board is “not considering a change to the target of 10 basis points”. At the meeting, RBA will also consider future bond purchases after current program completes in September.

Central scenario for GDP growth was “revised up further”. RBA now sees 4.75% GDP growth over 2021, 3.50% over 2022. Unemployment rate is projected to decline to around 5% at the end of this year and further to 4.5% at the end of 2022.

But CPI data “confirmed that inflation pressures remain subdued” in most parts of the economy. Underlying inflation is expected to be 1.5% in 2021 and 2% in mid-2023, even though CPI inflation might rise temporarily to above 3% in June quarter.

Fed Williams: Don’t overreact to volatility in prices

New York Fed President John Williams said in a a speech that as the economy further reopens, “I expect inflation to run somewhat above our 2 percent longer-run goal for the remainder of this year.” But he emphasized “not to overreact to this volatility in prices resulting from the unique circumstances of the pandemic”, but focus on the “underlying trends”.

“My expectation is that once the price reversals and short-run imbalances from the economy reopening have played out, inflation will come back down to about 2 percent next year,” he added.

Williams also said the economy is now “positioned to grow quickly”. “I expect that the rate of economic growth this year will be the fastest that we’ve experienced since the early 1980s. And that’s not only a forecast—we are already seeing signs of this pivot to strong growth in the economic statistics,” he added.

Fed Barkin: We will see price pressure this year

Richmond Fed President Thomas Barkin told CNBC yesterday, “we will see price pressure this year”, with a “very strong demand situation” and “constraints in supply”. “When those things happen, you’re definitely going to see price pressure,” he added.

“Inflation is a recurring phenomenon. Prices go up this year, prices go up next year,” he said. “I think it’s fair to argue the question of whether the combination of supply chain constraints and stimulus-driven price increases actually revert next year.”

Fed Powell: Economy outlook has clearly brightened

Fed Chair Jerome Powell said in a speech, while the US economy is “not out of the woods yet”, “real progress” was being made and economic outlook has “clearly brightened”. The economy is “reopening, bringing stronger economic activity and job creation.”.

But at “street level”, lives and livelihoods have been affected in ways that vary from “person to person, family to family, and community to community”. “The economic downturn has not fallen evenly on all Americans, and those least able to bear the burden have been the hardest hit,” Powell added.

On the data front

Australia trade surplus narrowed to AUD 5.57B in March, versus expectation of AUD 8.30B. Swiss will release SECO consumer climate in European session. UK will release mortgage approvals, M4 money supply, and PMI manufacturing final.

Later in the day, Canada will release building permits and trade balance. US will release trade balance and factory orders.

AUD/USD Daily Report

Daily Pivots: (S1) 0.7724; (P) 0.7745; (R1) 0.7785; More…

AUD/USD is staying in consolidation from 0.7815 and intraday bias remains neutral first. With 0.7676 support intact, further rise is in favor. On the upside, break of 0.7815 will resume the rebound from 0.7530. Further break of 0.7848 will bring retest of 0.8006 high. However, break of 0.7667 will extend the consolidation pattern from 0.8006, and turn bias to the downside for 0.7530 support.

In the bigger picture, whole down trend from 1.1079 (2001 high) should have completed at 0.5506 (2020 low) already. Rise from 0.5506 could either be the start of a long term up trend, or a corrective rise. Reactions to 0.8135 key resistance will reveal which case it is. But in any case, medium term rally is expected to continue as long as 0.7413 resistance turned support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 1:30 | AUD | Trade Balance (AUD) Mar | 5.57B | 8.30B | 7.53B | 7.60B |

| 4:30 | AUD | RBA Rate Decision | 0.10% | 0.10% | 0.10% | |

| 7:00 | CHF | SECO Consumer Climate Q2 | -11 | -15 | ||

| 8:30 | GBP | Mortgage Approvals Mar | 85K | 88K | ||

| 8:30 | GBP | Manufacturing PMI Apr F | 60.7 | 60.7 | ||

| 8:30 | GBP | M4 Money Supply M/M Mar | 0.80% | 0.80% | ||

| 12:30 | CAD | Building Permits M/M Mar | 2.10% | |||

| 12:30 | CAD | Trade Balance (CAD) Mar | 1.0B | |||

| 12:30 | USD | Trade Balance (USD) Mar | -73.4B | -71.1B | ||

| 14:00 | USD | Factory Orders M/M Mar | 1.10% | -0.80% |

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals