Summary

United States: Growth Comes with a Price

- Whether it is businesses struggling to get their hands on the physical inputs needed to complete production or the labor to facilitate operations, supply continues to have difficulty meeting the robust pace of demand and this is giving way to price pressure across a number of sectors.

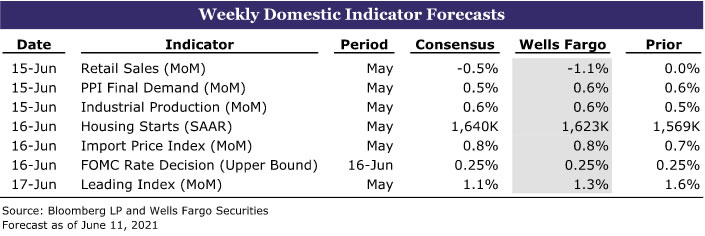

- Next week: Retail Sales (Tuesday), Industrial Production (Tuesday), Housing Starts (Wednesday)

International: Onward and Upward for the U.K. Economy

- The U.K. reported more evidence of a strong rebound as April GDP rose 2.3% month-over-month, on top of a large March gain, with services activity especially strong. The Eurozone economy is also in recovery; albeit after a sluggish start to the year, the European Central Bank is continuing with its accelerated pace of bond purchases for the time being.

- Next week: China Retail Sales & Industrial Output (Wednesday), New Zealand GDP (Thursday), U.K. Retail Sales (Friday)

Interest Rate Watch: Is the Heat on in the Eccles Building?

- We do not expect the FOMC to make any major policy changes at its meeting that concludes on June 16. However, the recent increase in inflation could induce some committee members to bring forward their forecasts of future rate hikes and open the discussion regarding the pace of asset purchases.

Credit Market Insights: Revolving Credit Data Newest Sign of Recreation Renaissance

- Lockdowns and uncertainty deterred consumers from taking on additional credit risk during the pandemic, but in the months after, revolving and nonrevolving credit went down significantly different paths.

Topic of the Week: Another Nail in the Coffin of Globalization?

- This past week, the U.S. Senate overwhelmingly passed the “Innovation and Competition Act of 2021.” What will be the effects if globalization starts to go into reverse?

U.S. Review

Growth Comes with a Price

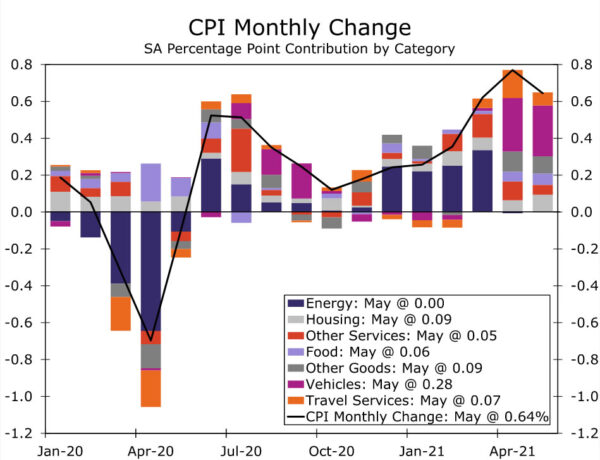

In what was a relatively light week for new economic data, the May report on consumer prices took center stage. Consumer price inflation continued to tear higher in May, with prices up 0.6% on the month, and the year-over-year rate leaping to 5.0%. A handful of categories, most closely tied to the reopening of the service sector (airfares, hotel and apparel prices) and supply bottlenecks (rental car and vehicle prices), again accounted for an outsized share of the rise in prices (see chart). But, May’s strength cannot be completely attributed to one-off temporary gains, nor low-base effects flattering year-ago comparisons.

The long-awaited pickup in housing costs has arrived, as the scorching price increases in the purchase market over the past year are starting to feed into the CPI. Owner’s equivalent rent (OER) rose 0.3% in May, which was the largest gain since mid-2019. Since this component accounts for 30% of the core CPI, a sustained turnaround in price growth will supply another sizable and longer-lasting boost to inflation. There were also signs of firming rental prices. Rents rose 0.2% (0.24%), the strongest monthly increase since the pandemic struck and consistent with the continued rise in market measures of daily asking rents.

The outsized gains in a few select sectors support the Fed’s view that the current degree of price pressures are temporary. But, we see signs of inflationary pressures broadening out, which we believe will keep monthly price gains from merely falling back to their pre-pandemic trend after the current flurry of activity. In our monthly forecast update released this week, we upgraded our expectations for inflation and now forecast the CPI to run over 4.0% on a year-ago basis between now and the first quarter of next year.

We also upgraded our full-year GDP growth forecast to 7.3% from 7.0% previously. If this above-consensus forecast comes to fruition, it would be the strongest year of growth since 1951. But, such a strong pace of growth comes with its challenges, and there is increasing evidence economic activity could be even stronger if not for supply shortages hampering most sectors of the economy.

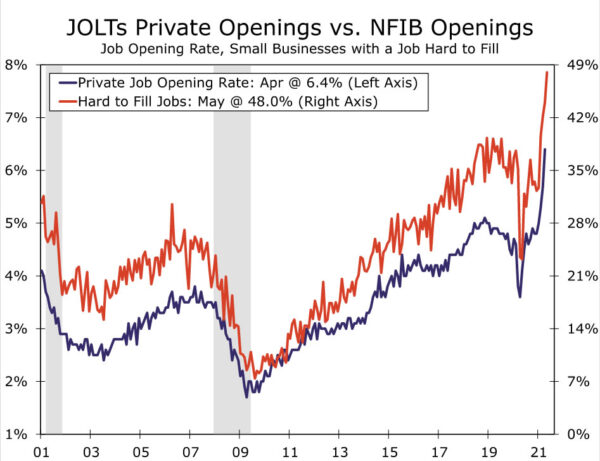

In addition to the shortage of key inputs ranging from semiconductors to building materials, labor shortages are becoming a growing concern. In the latest National Federation of Independent Business (NFIB) report, nearly half of small business owners had open positions they were unable to fill, and job openings continue to soar (see chart). Job openings blew past previous records to reach an all-time high of 9.3 million in April. High levels of openings, while millions are still out of the labor force, speaks to the current disconnect between supply and demand. Quits also rose to a new high and, along with increased wage pressures, indicate workers are gaining the upper hand in the jobs market. Shortages are causing price pressures to broaden as higher wages and input costs challenge firms trying to protect profit margins.

Data this week continued to demonstrate what you may be tired of hearing: We have a supply problem. Whether its businesses struggling to get their hands on the physical inputs needed to complete production or the labor to facilitate operations, supply continues to have difficulty meeting the robust pace of demand and this is giving way to price pressure across a number of sectors.

U.S. Outlook

Retail Sales • Tuesday

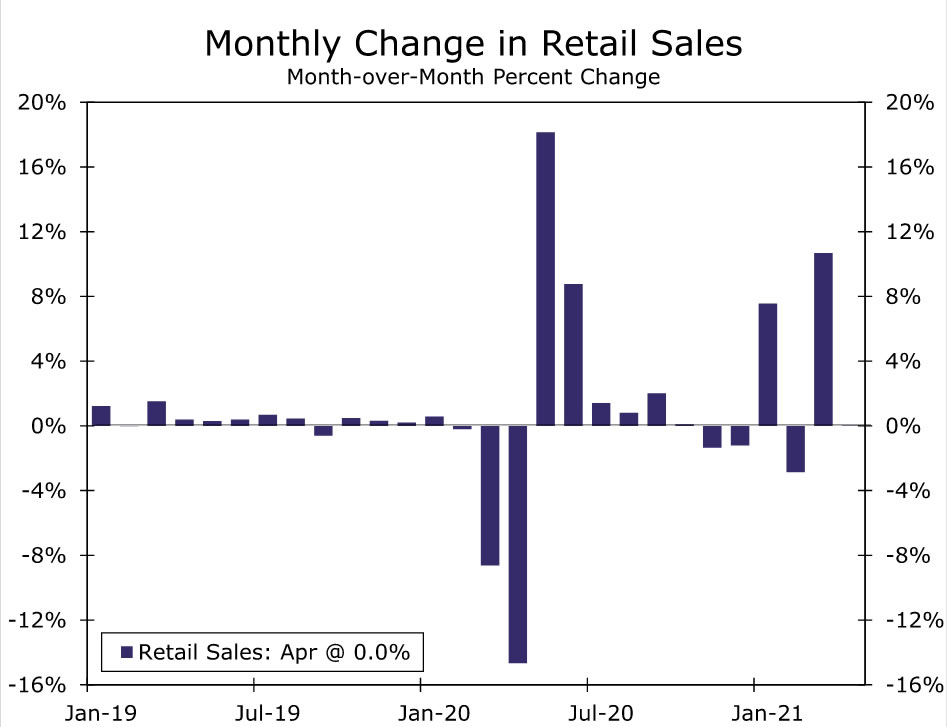

Retail sales were unchanged in April after stimulus checks in the prior month drove the second-largest increase on record. The monthly retail sales figures are typically a good proxy for consumer spending more broadly, but because of the unique characteristics of this cycle and where we are in that cycle at the moment, it may not be the best barometer.

Most of the heavy lifting when it comes to consumer spending will be done on the services side. Services do show up in some places in retail sales; one of the first lines we will be checking is the line for spending at bars and restaurants. But because the report is a better reflection of goods spending, we expect it to be hit and miss for the next several months. May, for example, could be a miss as supply chain problems hold back auto sales resulting in headline decline for the month. Excluding autos, sales should post a modest gain, but even if they do not, it will not portend anything of much consequence to our expectation for a recreation renaissance this summer.

Industrial Production • Tuesday

It will be a double header for economic data on Tuesday morning with the retail sales report being followed 45 minutes later with Industrial Production. Although core capital goods orders are already well-above their pre-pandemic peak, output still has a long way to go. Again, the culprit here is long wait times for deliveries and the lack of critical input components.

We expect the May figures for industrial production to show an increase of 0.6%. If realized, that would be roughly in line with last month’s gain, but the bigger point here is how much faster production could be ramping up were it not for these kinks in the supply pipeline. Just as autos may hold back retail sales, they could have an outsized influence on manufacturing production as well. But with mixed reports about auto plant closures at one major auto-maker and planned reopenings at another, a swing in either direction would not be surprising. This dynamic will be compounded in coming months by the seasonal adjustment process and the difficulty of incorporating the summer shutdowns. Bottom line: The speed limit for production growth is being set by the availability of scarce resources.

Housing Starts • Wednesday

Rising prices and the limited availability of lumber and building materials have weighed on residential construction. Housing starts fell 9.5% in April as single-family starts tumbled, while apartment development picked up. Building permits, which typically lead starts by a couple of months, held up better. Overall permits rose 0.3%, with all the gain coming from projects with five units or more. Despite the decline in starts, we suspect that demand for housing, and single-family homes in particular, remains white-hot.

Supply shortages are one of the greatest challenges for builders at present. Lumber prices have eased in recent days, but labor and other key inputs remain in short supply, which will continue to be a major headwind until at least this fall. That said, builder confidence, as indicated by the NAHB/Wells Fargo Housing Market Index (HMI), remains solid. The HMI has hovered near historic highs this year signaling that new residential construction will likely continue at a fairly robust pace, despite supply-side headwinds. Bearing that in mind, we look for starts to strengthen in May and come in at around a 1.6 million-unit pace.

International Review

European Central Bank Signals It’s Too Early to Taper

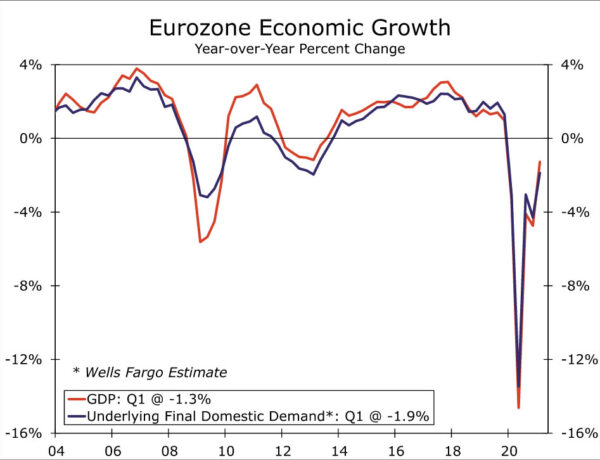

The European Central Bank (ECB) held monetary policy steady at this week’s meeting, signaling that it was too early to slow the pace of its bond purchases. The ECB kept its Deposit Rate at -0.50% and maintained the size of its Pandemic Emergency Purchase Program (PEPP) at €1.85 trillion, saying that it expects that purchase program to run until at least March 2022. There was some focus ahead of the meeting on whether the ECB might slow the pace of its bond purchases. However, the ECB indicated it was too early for such a move, saying that it “expects net purchases under the PEPP over the coming quarter to continue to be conducted at a significantly higher pace than during the first months of the year.”

The ECB also provided updated economic projections and sees faster Eurozone GDP growth and CPI inflation than previously. The ECB forecasts GDP growth of 4.6% for 2021 (compared to 4.0% in March) and 4.7% for 2022 (4.1% in March). On inflation, the ECB expects the CPI to rise 1.9% in 2021 (compared to 1.5% in March) and 1.5% in 2022 (1.2% in March). ECB President Lagarde also said the risks to the growth outlook were now broadly balanced. While confidence surveys certainly point to stronger growth ahead, that comes after a sluggish start for the Eurozone economy in 2021. Revised Q1 GDP figures did show a smaller than previously reported decline, of just 0.3% quarter-over-quarter. However, domestic activity remains somewhat subdued as consumer spending fell 2.3% quarter-over-quarter, and our estimate of underlying final domestic demand fell 1.1%. At this stage, as long as the Eurozone economy shows a perceptible firming in growth in the months ahead, we expect the ECB to announce a slower pace of bond purchases from Q4-2021 at its September meeting.

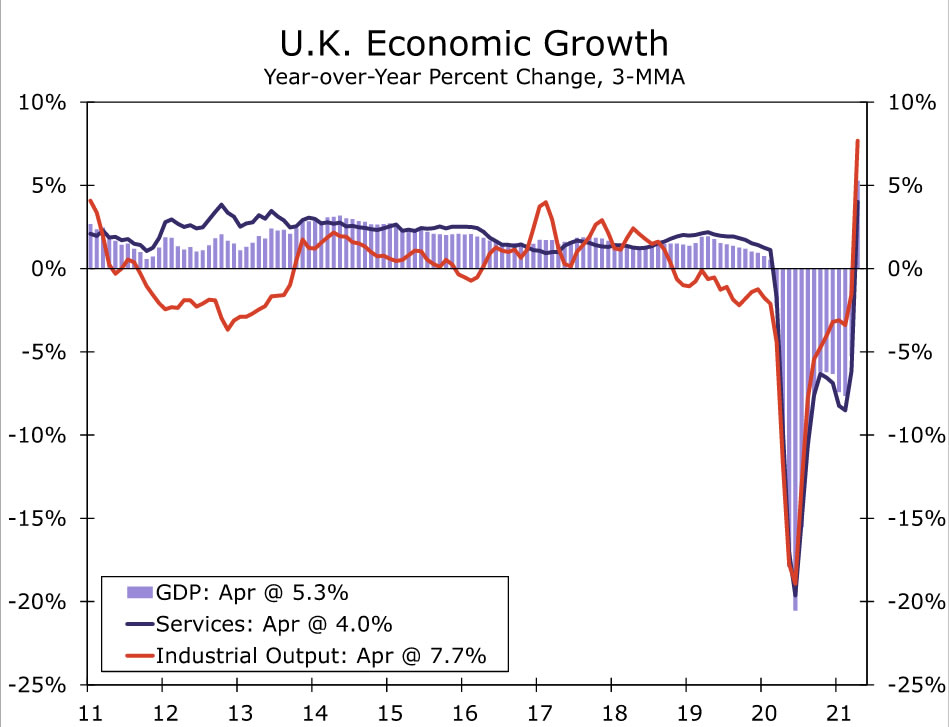

Onward and Upward for the U.K. Economy

The waiting is already over for the U.K. economy, which is reporting evidence of a strong rebound as the government’s progress in vaccinating the population against COVID has allowed the economy to reopen. April GDP rose 2.3% month-over-month, coming on top of a 2.1% increase in March. Service sector activity was particularly strong, rising 3.4%, although industrial output fell 1.3%. With the April increase, the level of U.K. GDP is 4% above its Q1 average, putting the economy on course for a very strong gain in GDP in Q2. With PMI surveys suggesting that momentum will continue, there could even be upside risk to our full-year 2021 GDP growth forecast of 7.0%. The strong rebound in activity also underscores the Bank of England’s decision to slow the pace of its bond purchases at its May monetary policy meeting, and why we expect a further slowing in bond purchases to be announced at the August monetary policy meeting.

Inflation Remains Elevated in Latin America

This week’s price data from Latin America pointed to still-elevated inflation, keeping pressure on the region’s central banks to raise policy interest rates. Of particular note, Brazil’s May CPI quickened more than expected to 8.06% year-over-year, with higher commodity prices and higher electricity prices contributing to the outcome. The increase in the CPI is more than double the central bank’s 3.75% inflation target for 2021. Brazil’s central bank has already raised its Selic rate by a cumulative 150 bps this year to 3.50%, and the consensus forecast is for another 75-bp rate increase at next week’s monetary policy announcement. Mexico’s May CPI inflation eased slightly to 5.89% year-over-year, although the core CPI actually quickened to 4.37%—both well above the Bank of Mexico’s 3% inflation target. Mexico’s central bank has not raised interest rates so far this year—in fact, it cut interest rates 25 bps as recently as February—but given elevated inflation, the Bank of Mexico appears likely to begin raising interest rates in the months ahead.

International Outlook

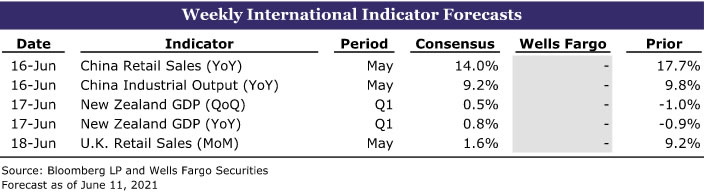

China Retail Sales and Industrial Output • Wednesday

Next week’s Chinese activity data for May are expected to show a further moderation in growth, reflecting both waning base effects as well as some back and forth in economic activity so far this year. In early 2020, activity plunged in Q1 before bouncing back strongly in Q2. Thus in terms of year-over-year comparisons in the early part of 2021, very strong growth in Q1 has given way to somewhat slower growth in Q2.

In addition, some renewed localized outbreaks in COVID cases have weighed on activity at times in China during the early part of this year, while confidence surveys have also been slightly mixed, even if they have been solid overall. It is against this backdrop that the consensus forecast is for May retail sales growth to slow further to 14.0% year-over-year, while growth in industrial output is expected to slow to 9.2%. Even with some slowing in activity China’s full-year 2021 GDP growth should be very respectable, with our forecast for China’s economy to grow 9%.

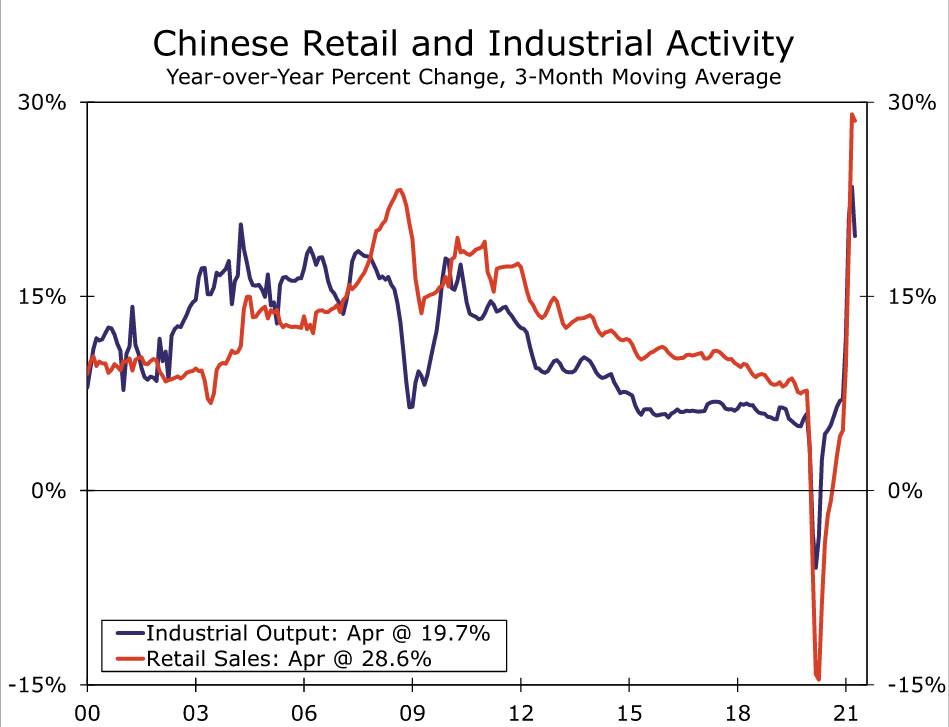

New Zealand GDP • Thursday

New Zealand’s first quarter GDP figures are released next week, which may still have some implications for the policy outlook, despite being a bit dated. Economic indicators have been somewhat mixed heading into the release. Q1 real retail sales were a significant upside surprise, showing an unexpected 2.5% quarter-over-quarter gain. Other activity indicators have been less compelling as Q1 employment rose 0.6% and real manufacturing activity rose 0.4%, while the indications are net exports likely subtracted from GDP growth during the quarter. Given the mixed signals, the consensus forecast is for Q1 GDP to rise a moderate 0.5% quarter-over-quarter.

Despite the slowish start to the year the Reserve Bank of New Zealand has turned modestly hawkish, signaling at its most recent monetary policy announcement that it could begin to raise interest rates from late next year. We also note that more recent data suggest a noticeable pickup in Q2 activity, including gains in retail card spending and firming business confidence. Thus, while the Q1 GDP figures are dated, an unexpectedly strong Q1 increase combined with more recent signs of a pickup could bring forward the point at which the central bank begins to raise interest rates.

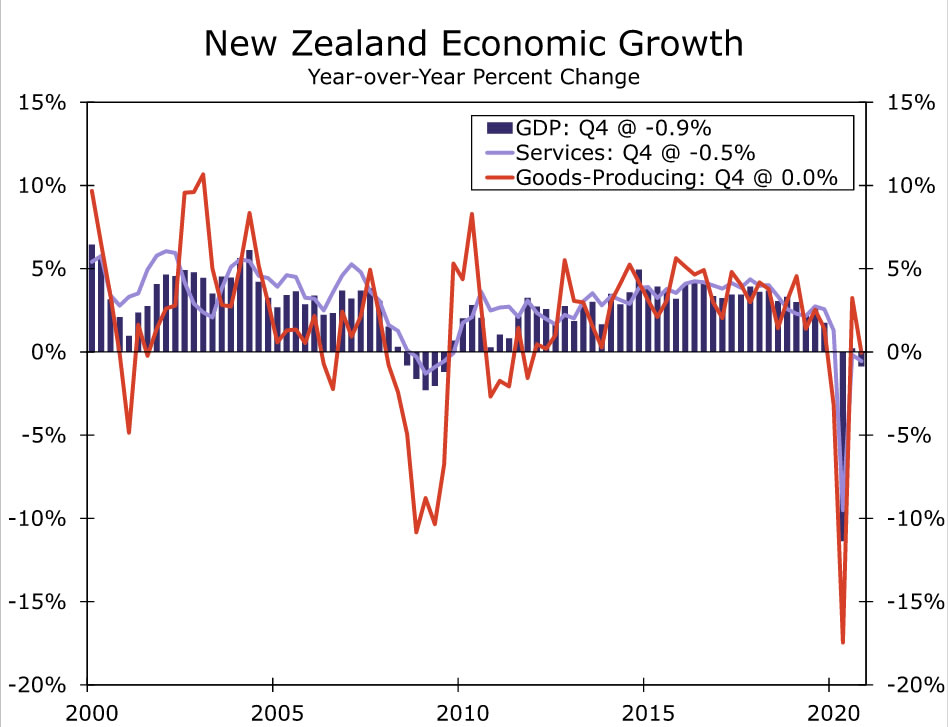

U.K. Retail Sales • Friday

After a soft start to 2021, the U.K. has shown a strong rebound in activity as the government has made good progress in vaccinating the U.K. population against COVID, allowing the economy to reopen. Next week’s May retail sales will be closely watched for evidence of whether that momentum has continued. The available retail indicators for May are mixed, with consumer confidence increasing, but a U.K. retailers’ survey showing a drop in the reported sales balance, and like-for-like sales slowing. Nonetheless, the consensus forecast is for a further 1.6% month-over-month gain in May retail sales, even after a 9.2% increase in April.

The retail sales figures are not the only significant data on next week’s schedule. U.K. employment is forecast to rise by 150,000 for the three months to April compared to the prior three months, which would be the largest increase since February 2020. May CPI figures should also show some quickening of inflation, though not to the same extent as in the United States. The consensus forecast is for the May CPI to rise 1.8% year-over-year, while the core CPI is expected to rise 1.5%.

Interest Rate Watch

Is the Heat on in the Eccles Building?

The Federal Open Market Committee (FOMC) will hold its next regularly scheduled policy meeting on June 15-16. While we do not anticipate any major policy changes will be announced at the conclusion of next week’s meeting, the accompanying statement and press conference could provide an update on how committee members’ views are evolving regarding the pace of asset purchases.

The Fed is currently buying $80 billion worth of Treasury securities and $40 billion worth of mortgage-backed securities (MBS) every month. The mantra from the Fed has been that it would continue its current rate of asset purchases “until substantial further progress has been made toward the Committee’s maximum employment and price stability goals.” As prices have ripped higher over the past two months, policymakers have mostly highlighted the recent acceleration’s transitory nature. Until Fed officials drop references to transitory inflation, we maintain that the labor market would need to strengthen significantly before the FOMC starts to more publicly contemplate tapering its asset purchases. If the 559,000-job increase that we saw in May proves to be sustainable, then we anticipate Fed officials will warm up to eventual tapering of asset purchases later this year with an eye toward implementation of that tapering on a conditional basis early in 2022.

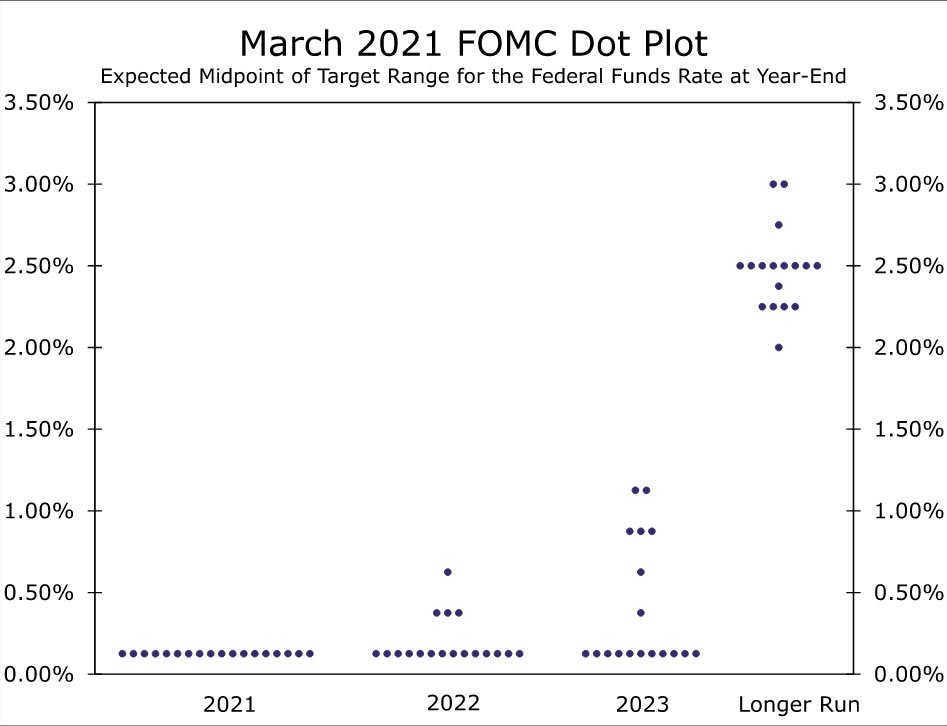

Next week, we also expect the committee to upgrade its assessment of the current state of the economy relative to the April 18 meeting statement and its assessment of the outlook in its updated Summary of Economic Projections (SEP). These changes may also provide a view into how committee members are thinking about inflation. Inflation has come on stronger and faster than the Fed expected only a few months ago, and we expect to see hefty upward revisions to 2021 inflation forecasts. Forecasts of inflation in 2022 and 2023 will be more important for the path of the fed funds rate, however, and those forecasts are still likely to convey that the FOMC sees the current strength in inflation as transitory. Even as the current degree of inflation is expected to subside over 2022 and 2023, the recent strength and growing belief that the labor market is likely tighter than conventional measures would suggest means a few Fed officials could very well pull forward projections for when interest rates are likely to rise. In March, 11 of 18 officials expected the fed funds rate to remain on hold through 2023, but we would not be surprised to see the number slip toward around half.

Credit Market Insights

Revolving Credit Data Newest Sign of Recreation Renaissance

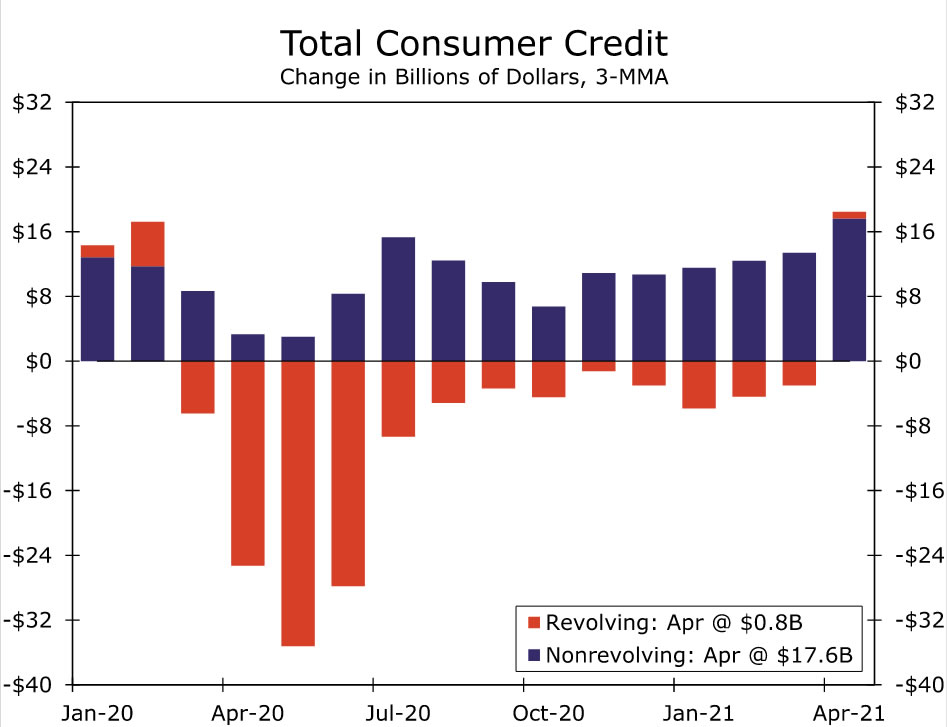

April’s consumer credit release marked exactly a year since revolving credit tumbled a record-breaking $57.3 billion and nonrevolving credit fell $6.3 billion in a month, its first monthly decline since late 2015, as consumers grappled with the fallout from the pandemic. Lockdowns and uncertainty deterred consumers from taking on additional credit risk during that time, but in the months after, revolving and nonrevolving credit went down significantly different paths. The less volatile, nonrevolving credit eked out a gain in every one of the past 12 months and posted a 4.9% year-over-year growth rate in April. Auto loans in particular have been a driver of the category due to both the increase in sales volume and the upward price pressure, which has made auto purchases more expensive. Meanwhile, revolving credit fell in nine out of the past 12 months due to a combination of consumers’ habits shifting away from typical spending patterns (forced thrift) and savings allowing many consumers to diligently pay down debt, as credit card charge-off rates dropped to their lowest since 1985.

Source: Federal Reserve Board and Wells Fargo Securities

However, some of these trends may have already started to reverse this spring. April was the first month since the start of the pandemic that revolving credit increased on a three-month moving average basis (see chart). Credit card charge-off rates also increased after back-to-back quarterly declines. Along with strong personal spending figures this quarter, this is yet another sign of a consumer who is willing to spend. The transition to revolving credit is closely linked to the trends that we discussed in our recent piece, Recreation Renaissance. Consumers did not shy away from “staples” services spending during the pandemic, which includes categories such as housing & utilities, financial services & insurance and health care, but did pull back on “discretionary” services spending (food services & accommodation, recreation services, transportation services and other services). In the next couple of months, decreased uncertainty and more discretionary spending options could lead to a pickup in revolving credit as consumer spending picks up at its fastest annual pace since 1951 this year.

Topic of the Week

Another Nail in the Coffin of Globalization?

On June 8, the U.S. Senate overwhelmingly passed the “Innovation and Competition Act of 2021.” The proposed legislation is intended to beef up the nation’s technology to better able the manufacturing sector to compete with China. Among other things, the bill allocates money for scientific research and subsidies for semiconductor chip manufacturers, and it overhauls the National Science Foundation. The bill now heads to the House of Representatives. If the bill clears the House, it will then head to the White House where President Biden likely will sign it into law.

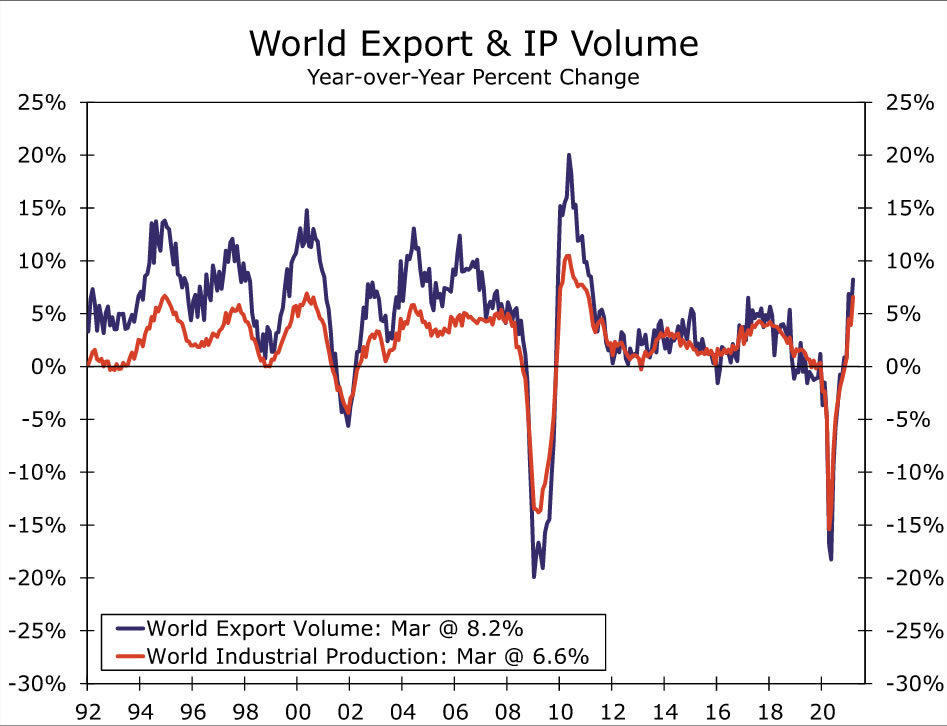

The lopsided margin of passage—the bill was approved by a 68-32 vote—indicates that Democrats and Republicans today generally view China as a strategic threat, if not geopolitically then at least economically. An earlier generation of lawmakers generally held the view that China’s rise could be beneficial to the United States, and these years were characterized by a deepening degree of globalization. As shown in the following chart, global trade grew roughly twice as fast as global industrial production (IP) in the 1990s and in the first decade of the 21st Century. NAFTA was ratified and went into effect in the early 1990s, and China joined the World Trade Organization in 2001. The production process, which once occurred largely in one country, was internationalized, and inputs were shipped around the world. But, the Trump administration viewed China in more antagonistic terms, and the Biden administration is unlikely to remove the tariffs that President Trump imposed on China anytime soon.

What will be the effects if globalization starts to go into reverse? For starters, global trade likely will continue to grow more or less in line with global IP, rather than faster. Therefore, global export volumes, which have shot up in recent months as some major economies have started to reopen, likely will decelerate in coming years as the global economy settles back to “normal.”

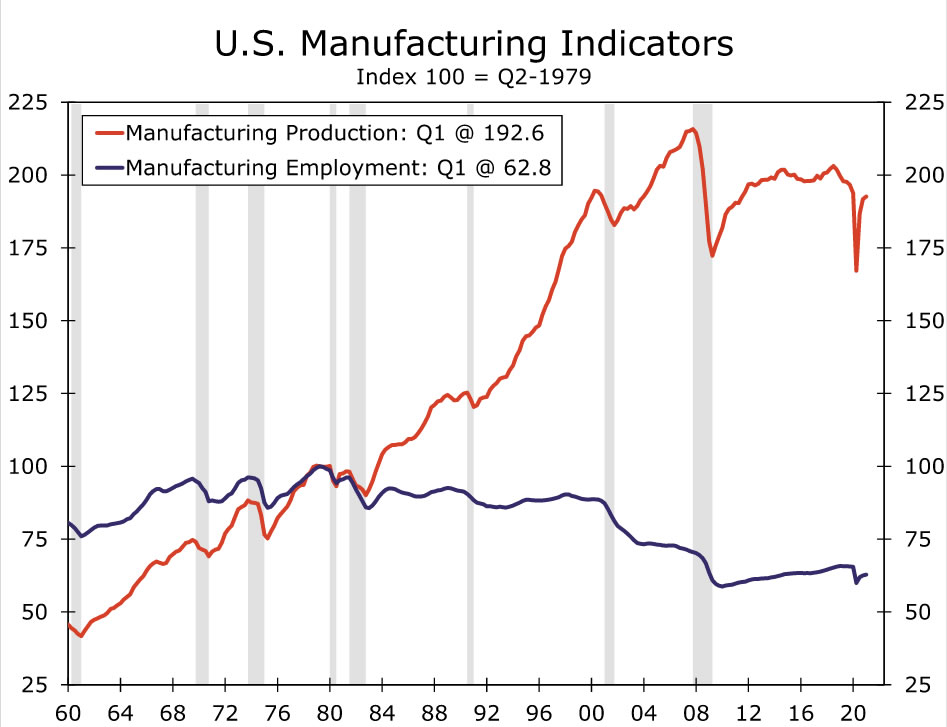

Some observers believe that re-shoring of American manufacturing production will lead to a boom in manufacturing employment in the United States. But, we do not share this view. As shown below, manufacturing employment in the country peaked in Q2-1979 at 19.5 million workers. It has subsequently declined by nearly 40% on balance. Meanwhile, American manufacturing production has essentially doubled over that intervening 42-year period. In other words, American manufacturers have been able to double production by productivity gains via more automation. Re-shoring, should it occur, could lead to strong growth in American manufacturing production in coming years. But in our view, most of this increased production would be accomplished through even more automation rather than via a significant increase in manufacturing employment. In our view, the number of factory jobs in the United States is not likely to return to its 1979 peak anytime soon.

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals