- ECB set to announce higher inflation target, Lagarde presser to follow

- Dollar little changed after Fed minutes, yen shines as yields crumble

- Stocks retreat amid Chinese regulatory crackdown, oil tanks

Euro braces for special ECB announcement

The European Central Bank will announce the outcome of its strategic policy review at 11:00 GMT today, with a press conference by President Lagarde to follow 90 minutes later. Reports suggest the ECB will raise its inflation target to 2% and signal it will tolerate an overshoot if the situation demands it.

This would essentially lock the ECB into negative interest rates for a longer period of time. It hasn’t been able to hit its inflation target for a decade now, so raising it further would imply it intends to keep its foot heavy on the money accelerator for years.

That’s bad news for the euro. It would crystalize the imminent divergence of monetary policy between the Eurozone and America. With the Fed moving towards higher rates but the ECB staying committed to negative rates, yield differentials could widen further in the dollar’s favor in the coming years, which argues for a lower euro/dollar over time.

The last time the world’s two biggest central banks drifted in opposite directions was in 2014-2015, a period of carnage for euro/dollar. The market impact might be smaller this time as the Fed will likely be less aggressive, but the direction seems clear.

Dollar unfazed by Fed minutes, yen powers higher

The US dollar remained near its recent highs yesterday, taking little damage from the minutes of the latest FOMC meeting. The general sense in the minutes was that the Fed is not in a rush to scale back its humongous asset purchase program, but is moving closer to doing so.

‘Various’ officials expected the conditions for tapering to be met ‘somewhat earlier’, while ‘some’ others suggested they would have the information soon to make a judgment call on the economy. Nothing new there. The Fed is still on track to announce it will dial back its asset purchases in the fall, likely after a strong warning signal in August. For all that to happen, we need a couple of scorching-hot jobs reports.

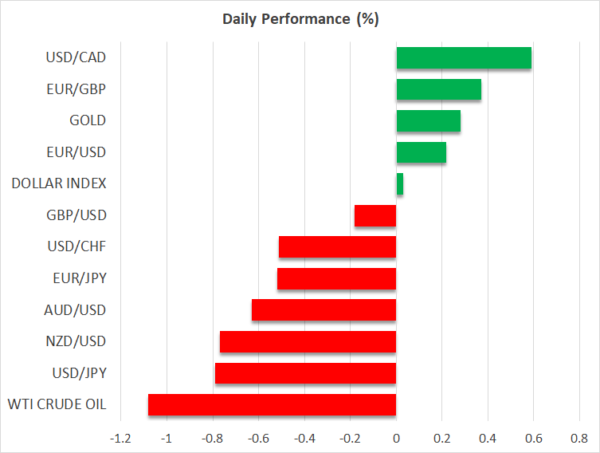

Meanwhile, the Japanese yen has been the biggest winner from the latest demolition in Treasury yields. Market participants are still mystified by what is pushing bond yields lower. Is it an epic short squeeze that’s still playing out, is it big banks swallowing up bonds for collateral purposes, or is the market really pricing slower growth and lower inflation?

We’ll find out the answer by whether the move persists or not. For now, this has lit a fire under the yen, which shines in an environment of lower rates and risk aversion. Still, with central banks across the world moving towards higher rates but the Bank of Japan not following suit, the big picture seems gloomy.

Stocks drop as Chinese regulators flex

In the stock market, the S&P 500 and Nasdaq closed at another record high yesterday, but the mood has deteriorated today. Futures point to losses of around 1% for the major US indices when Wall Street opens today, in sympathy to equities in Hong Kong which are down almost 3% after new regulations from Beijing.

Chinese regulators continue to tighten the screws on large multinationals, especially in the tech sector, announcing rules that would allow them to block companies from listing overseas. Tech heavyweights like Tencent and Alibaba are down 4% today.

Finally, oil prices remain under heavy pressure for a third session. Market participants seem to be pricing in the risk of a ‘pump at will’ endgame from OPEC as the fallout between Saudi Arabia and the UAE continues, with the latest bouts of risk aversion adding fuel to the retreat.

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals