Dollar drops broadly overnight and stays weak, even though Fed acknowledged that progress has already been made in the economy. Uncertainty in the risk markets is keeping Aussie soft too. But Canadian Dollar is apparently rebounding with resilience in oil prices. Sterling is also strong with Swiss Franc while Euro under performs them. Focus will now turn to US GDP report.

Technically, GBP/USD’s break of 1.3908 resistance suggests completion of recent fall from 1.4248. USD/CHF’s break of 0.9116 also affirms that rebound from 0.8925 has completed at 0.9273 already. A major focus is now on the relatively weak Euro. Break of 1.1880 resistance in EUR/USD should also confirm short term bottoming at 1.1751. That would solidify the case of more Dollar selling for the near term at least.

In Asia, at the time of writing, Nikkei is up 0.76%. Hong Kong HSI is up 2.74%. China Shanghai SSE is up 1.04%. Singapore Strait Times is up 0.50%. Japan 10-year JGB yield is up 0.0049 at 0.021. Overnight, DOW dropped -0.36%. S&P 500 dropped -0.02%. NASDAQ rose 0.70%. 10-year yield rose 0.027 to 1.261.

Fed acknowledged that progress has been made

FOMC acknowledged in the statement that “the economy has made progress toward” the “maximum employment and price stability goals”. Chair Jerome Powell noted that Fed discussed the pace and composition of tapering but did not make any final decisions. Powell also noted that here is “little support” for tapering MBS purchases first, and that participants have mixed views on tapering MBS purchases faster. Next focus is the minutes which will be released in 3 weeks’ time.

In the mean time, Fed officials would likely share more of their view over tapering ahead. Key events leading to the September meeting are the July meeting minutes and Jackson Hole symposium in late August. We also expect more detailed information about tapering will be released in September, alongside updated economic projections and median dot plots. A formal tapering announcement will then be made in December.

More in: FOMC Review: Economy Moving Toward Inflation and Employment Goals. FOMC Minutes and Jackson Holes in Focus

Suggested readings:

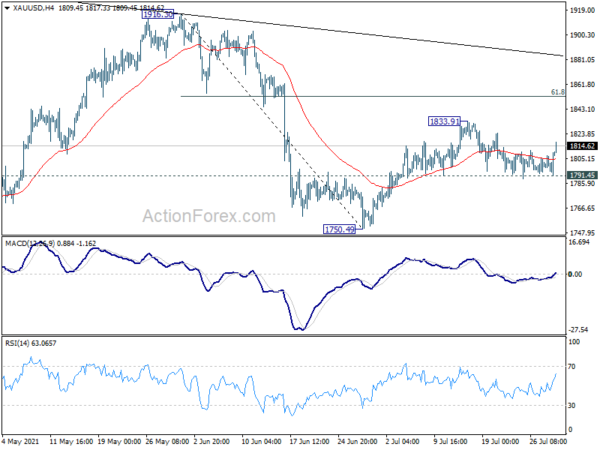

Gold back about 1800, following Dollar selloff

Gold rebounded notably and reclaimed 1800 handle, following Dollar’s post FOMC selloff. The development suggests that 1791.45 support could have been defended well, keeping the rise from 1750.49 alive. Focus is now back on 1833.91 resistance. Break there will target 61.8% retracement of 1916.30 to 1750.49 at 1852.96 next.

Overall, we’d need to see Gold breaking 1916.30 resistance firmly, to give us more confidence that the corrective pattern from 2074.84 has completed. Otherwise, outlook will stay neutral for now.

New Zealand ANZ business confidence dropped to -3.8, time to start normalizing monetary conditions

New Zealand ANZ business confidence dropped from -0.6 to -3.8 in July. Own activity outlook also dropped from 31.6 to 26.3. Looking at some more details, expect intentions dropped from 13.4 to 7.6. Investment intentions dropped from 25.5 to 17.4. Employment intentions rose from 19.7 to 21.4. Cost expectations rose from 86.2 to 88.2. Pricing intentions dropped slightly from 62.8 to 61.3. Inflation expectations rebounded from 2.41 to 2.70.

ANZ said, “the combination of clear upside for the activity and inflation starting point, but downside risks in the (quite possibly not far off) future, do, on the face of it, present a conundrum for the Reserve Bank… “If they raise rates now, the odds are indeed uncomfortably high that they’ll end up reversing course before long… Inflation pressures provide an excellent reason to raise interest rates now, despite downside risks… inaction comes with risks too. It’s time to start normalising monetary conditions, even if trouble might lie closer ahead than we hope.”

Looking ahead

Germany unemployment and CPI flash, Eurozone economic sentiment, UK M4 money supply will be released in European session. US GDP will take center stage later in the day, with jobless claims and pending home sales.

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3862; (P) 1.3887; (R1) 1.3929; More….

GBP/USD’s break of 1.3908 suggests that fall from 1.4248 has completed at 1.3570 already. Corrective pattern from 1.4240 might have finished too. Intraday bias is back on the upside for retesting 1.4248 high next. On the downside, below 1.3841 minor support will turn intraday bias neutral and bring retreat first, before staging another rally.

In the bigger picture, as long as 1.3482 resistance turned support holds, up trend from 1.1409 should still continue. Decisive break of 1.4376 resistance will carry larger bullish implications. However, firm break of 1.3482 support will argue that the rise from 1.1409 has completed. GBP/USD would then be seen in another leg of long term range pattern between 1.1409 and 1.4376. Deeper fall could then be seen to 61.8% retracement of 1.1409 to 1.4248 at 1.2493, and even below.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 1:00 | NZD | ANZ Business Confidence Jul | -3.8 | -0.6 | ||

| 1:30 | AUD | Import Price Index Q/Q Q2 | 1.90% | 0.20% | 0.20% | |

| 7:55 | EUR | Germany Unemployment Rate Jul | 5.80% | 5.90% | ||

| 7:55 | EUR | Germany Unemployment Change Jul | -25K | -38K | ||

| 8:30 | GBP | Net Lending to Individuals (GBP) Jun | 6.8B | 6.9B | ||

| 8:30 | GBP | Mortgage Approvals Jun | 85K | 88K | ||

| 8:30 | GBP | M4 Money Supply M/M Jun | 0.30% | 0.40% | ||

| 9:00 | EUR | Eurozone Economic Sentiment Indicator Jul | 118.8 | 117.9 | ||

| 9:00 | EUR | Eurozone Services Sentiment Jul | 19.5 | 17.9 | ||

| 9:00 | EUR | Eurozone Industrial Confidence Jul | 13 | 12.7 | ||

| 9:00 | EUR | Eurozone Consumer Confidence Jul F | -4.4 | -4.4 | ||

| 9:00 | EUR | Eurozone Business Climate Jul | 1.71 | |||

| 12:00 | EUR | Germany CPI M/M Jul P | 0.50% | 0.40% | ||

| 12:00 | EUR | Germany CPI Y/Y Jul P | 3.20% | 2.30% | ||

| 12:30 | USD | Initial Jobless Claims (Jul 23) | 365K | 419K | ||

| 12:30 | USD | GDP Annualized Q2 P | 8.20% | 6.40% | ||

| 12:30 | USD | GDP Price Index Q2 P | 5.40% | 4.30% | ||

| 14:00 | USD | Pending Home Sales M/M Jun | 0.80% | 8.00% | ||

| 14:30 | USD | Natural Gas Storage | 49B |

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals