The forex markets are generally trading in very tight range in Asian session. While DOW surged to new record high overnight, Asian indexes are just mixed. Dollar started a pull back but there is no clear follow through selling so far. At the same time, commodity currencies are generally stronger for the week, as supported by risk-on sentiment. But there is no breakout yet. The markets are still awaiting inspirations for the next committed move.

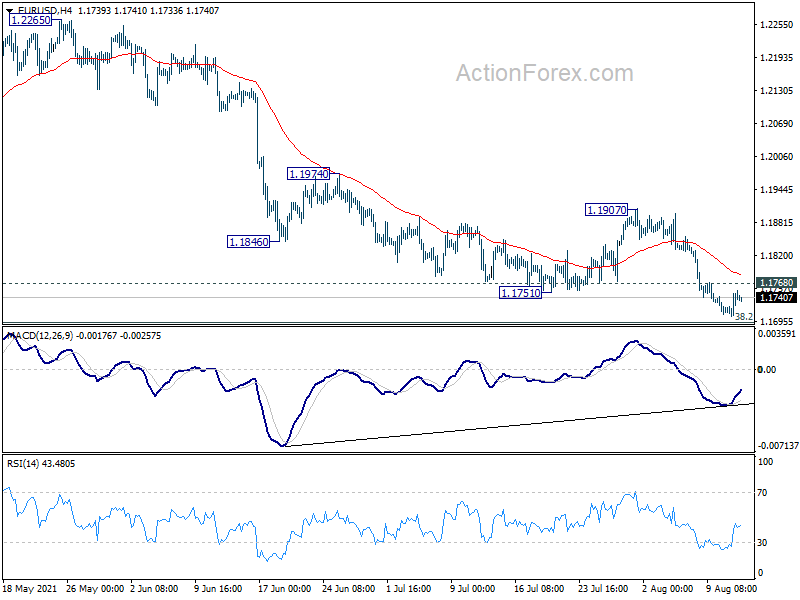

Technically, EUR/USD’s decline slowed and recovered ahead of 1.16/17 key support zone. The question is whether it could form a base around current level and stage a reversal. Immediate attention in on 1.1768 minor resistance. Break will probably bring stronger rebound back to 1.1907 near term resistance. Such development, if happens, could be an early sign of Dollar weakness elsewhere.

In Asia, at the time of writing, Nikkei is up 0.20%. Hong Kong HSI is down -0.06%. China Shanghai SSE is down -0.12%. Singapore Strait Times is up 0.38%. Japan 10-year JGB yield is down -0.0072 at 0.035. Overnight, DOW rose 0.62%. S&P 500 rose 0.25%. NASDAQ dropped -0.16%. 10-year yield dropped -0.003 to 1.39.

DOW hit new record as up trend enters into acceleration

DOW rose to close at new record high at 35484.97 overnight, up 0.62%. The slight moderation in core CPI in the US seemed to be welcome by investors. The development so far affirmed the view of the “transitory” camp in Fed. While it’s still on track for tapering, probably sooner than expected, there is still much room to wait-and-see before eventually raising interest rates, probably late next year.

Technically, the long term up trend in DOW now looks ready to enter into another near term acceleration phase. Outlook will stay bullish as long as this week’s low at 35041 holds. Next target is 61.8% projection of 26143.77 to 35091.56 from 33741.76 at 37159.81. We’ll see if DOW could hit this level within Q3.

Fed Kaplan: Could announce tapering in Sep, starts in Oct

Dallas Fed President Robert Kaplan said yesterday that if the economy unfolds between now and the September meeting as he expected, ” I would be in favor of announcing a plan at the September meeting and beginning tapering in October.”

“The reason I’m saying we ought to begin the tapering soon is I think these purchases are very well equipped to stimulate demand. But we don’t have a demand problem in the economy,” he told CNBC.

“My thought is I’d rather take the foot off the accelerator soon and reduce the RPMs,” he added. “What I don’t want to do is keeping running at this speed for too long and then we’re going to have to take more aggressive action down the road.”

Fed George: Time has come to dial back the settings

Kansas City Fed President Esther George said in a speech, “with the recovery underway, a transition from extraordinary monetary policy accommodation to more neutral settings must follow”. She added, “today’s tight economy… does signal that the time has come to dial back the settings” of monetary stimulus.

“While recognizing that special factors account for much of the current spike in inflation, the expectation of continued strong demand, a recovering labor market, and firm inflation expectations are consistent, in my view, with the Committee’s guidance regarding substantial further progress toward its objectives. I support bringing asset purchases to an end under these conditions,” she said.

Fitch affirms Japan rating at A with negative outlook

Fitch affirmed Japan’s Long-Term Foreign-Currency Issuer Default Rating (IDR) at ‘A’ with a “negative” outlook. The ratings “balance the strengths of an advanced and wealthy economy, with correspondingly robust governance standards and public institutions, against weak medium-term growth prospects and very high public debt”. The negative outlook reflected “uncertainty about the medium-term macroeconomic and fiscal outlook from the continuing pandemic”.

The rating agency expects economic growth of 22.5% in 2021 and 3.0% in 2022. But risks are to the downside, as the ongoing fifth Covid-19 wave may further delay recovery. Inflation is likely to “remain subdued”, averaging 0.3% in 2021 and 0.7% in 2022. Fitch also said BoJ is likely to maintain its current monetary policy settings over the “next few years”.

Looking ahead

UK data will take center stage today, with GDP, production and trade balance. Eurozone will release industrial production. Later in the day, US will release PPI and jobless claims.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1714; (P) 1.1733; (R1) 1.1761; More…

Intraday bias in EUR/USD remains neutral at this point. We’d continue to look for strong support from 1.1602/1703 support zone to bring rebound. On the upside, above 1.1768 minor resistance will turn bias back to the upside for 1.1907 resistance first. However, sustained break of 1.1602 will argue that it’s already reversing the trend from 1.1603, and target 61.8% retracement of 1.1603 to 1.2348 at 1.1289.

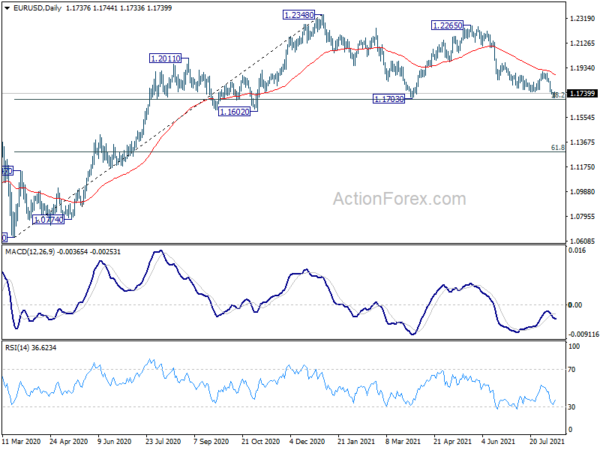

In the bigger picture, rise from 1.0635 is seen as the third leg of the pattern from 1.0339 (2017 low). Further rally could be seen to cluster resistance at 1.2555 next, (38.2% retracement of 1.6039 to 1.0339 at 1.2516). This will remain the favored case as long as 1.1602 support holds. Reaction from 1.2555 should reveal underlying long term momentum in the pair. However sustained break of 1.1602 will argue that the rise from 1.0635 is over, and turn medium term outlook bearish again.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | RICS Housing Price Balance Jul | 79% | 77% | 83% | 82% |

| 23:50 | JPY | PPI Y/Y Jul | 5.60% | 5.10% | 5.00% | |

| 01:00 | AUD | Consumer Inflation Expectations Aug | 3.30% | 3.70% | ||

| 03:00 | NZD | RBNZ Inflation Expectations Q/Q Q3 | 2.27% | 2.05% | ||

| 06:00 | GBP | GDP Q/Q Q2 P | 4.80% | -1.60% | ||

| 06:00 | GBP | GDP M/M Jun | 1.00% | 0.80% | ||

| 06:00 | GBP | Index of Services 3M/3M Jun | 5.50% | 3.90% | ||

| 06:00 | GBP | Industrial Production M/M Jun | 0.30% | 0.80% | ||

| 06:00 | GBP | Industrial Production Y/Y Jun | 9.20% | 20.60% | ||

| 06:00 | GBP | Manufacturing Production M/M Jun | 0.40% | -0.10% | ||

| 06:00 | GBP | Manufacturing Production Y/Y Jun | 29.50% | 27.70% | ||

| 06:00 | GBP | Goods Trade Balance (GBP) Jun | -10.1B | -8.5B | ||

| 09:00 | EUR | Eurozone Eurozone Industrial Production M/M Jun | 0.30% | -1.00% | ||

| 12:30 | USD | PPI M/M Jul | 0.60% | 1.00% | ||

| 12:30 | USD | PPI Y/Y Jul | 7.40% | 7.30% | ||

| 12:30 | USD | PPI Core Y/Y Jul | 5.70% | 5.60% | ||

| 12:30 | USD | PPI Core M/M Jul | 0.60% | 1.00% | ||

| 12:30 | USD | Initial Jobless Claims (Aug 6) | 367K | 385K | ||

| 13:00 | GBP | NIESR GDP Estimate (3M) Jul | 4.80% | |||

| 14:30 | USD | Natural Gas Storage | 47B | 13B |

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals