Euro jumps notably today, as supported by highest inflation reading in a decade, and hawkish comments from an ECB official, as well as rise in German yields. Though, it’s slightly outshone by Kiwi, Aussie and Swiss Franc for now. On the other hand, Dollar’s selloff continues to pick up momentum and even dips against Yen. Canadian Dollar also stays weak, getting little support from GDP data that matched expectations.

Technically, EUR/GBP’s break of 0.8592 minor resistance suggests resumption of the rebound from 0.8448. That’s affirming Euro’s underlying strength. But as EUR/CHF appears to be rejected by 1.0839 resistance, Euro’s rally is somewhat capped elsewhere. We’ll keep on monitoring European crosses to gauge the potential of more upside acceleration in EUR/USD and EUR/JPY.

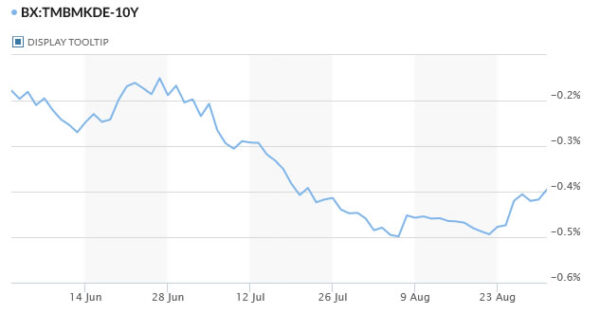

In Europe, at the time of writing, FTSE is down -0.62%. DAX is down -0.37%. CAC is down -0.41%. Germany 10-year yield is up 0.0209 at -0.396, back above -0.4 handle. Earlier in Asia, Nikkei rose 1.08%. Hong Kong HSI rose 1.33%. China Shanghai SSE rose 0.45%. Singapore Strait Times dropped -1.52%. Japan 10-year JGB yield rose 0.0064 to 0.026.

Canada GDP grew 0.7% mom in Jun, to contract -0.4% mom in Jul

Canada GDP grew 0.7% mom in June, matched expectations. Total economic activity was -1.5% below February 2020’s pre-pandemic level. Overall, 15 of 20 industrial sectors were up. Services-producing industries rose 0.7% mom while goods-producing industries rose 0.9% mom.

Statistics Canada said preliminary information indicates an approximate -0.4% decline in real GDP for July. The main decreases were in manufacturing, construction and retail trade.

ECB Holzmann will advise to slow down asset purchases in Q4, more so in Q1

ECB Governing Council member Robert Holzmann said in an interview, “we are now in a situation where we can think about how to reduce the pandemic special programs — I think that’s an assessment we share.””We have the opportunity to discuss how do we close the pandemic part and focus on the inflation part,” he added.

“If enough people share my opinion, we will certainly advise the Executive Board to slow down purchases in the fourth quarter and more so in the first,” Holzmann said. “We will spend as much as needed.”

Eurozone CPI jumped to 3.0% yoy in Aug, core CPI rose to 1.6% yoy

Eurozone CPI accelerated to 3.0% in August, up sharply from 2.2% yoy, above expectation of 2.8% yoy. CPI core rose to 1.6% yoy, up from 0.7% yoy, above expectation of 0.5% yoy.

Looking at the main components of euro area inflation, energy is expected to have the highest annual rate in August (15.4%, compared with 14.3% in July), followed by non-energy industrial goods (2.7%, compared with 0.7% in July), food, alcohol & tobacco (2.0%, compared with 1.6% in July) and services (1.1%, compared with 0.9% in July).

France consumer spending dropped -2.2% mom in Jul, GDP rose 1.1% qoq in Q2

France consumer spending dropped -2.2% mom in July, below expectation of 0.7% mom rise. This decrease came from the fallback in purchases of manufactured goods (–2.7%) and the sharp drop in food consumption (–2.9%). Energy expenditure, meanwhile, increased moderately (+1.0%).

France GDP grew 1.1% qoq in Q2 in volume term better than expectation of 0.9% qoq. GDP closed one quarter of the gap to is pre-crisis level at the end of 2020. It stood -3.2% below its level in Q4 2019.

Also released, Germany unemployment rate dropped from 5.6% to 5.5% in August, below expectation of 5.6%.

From UK, mortgage approvals dropped to 75k in July, below expectation of 79k. M4 money supply rose 0.1% mom, below expectation of 0.6% mom.

Japan industrial production dropped -1.5% mom in Jul, but expected to bounce back ahead

Japan industrial production dropped -1.5% mom in July, better than expectation of -2.5% mom. The overall output was back below pre-pandemic levels already. The Ministry of Economy, Trade and Industry expects, however, a bounce back of 3.4% in production in August, and 1.0% in September.

Unemployment rate ticked down to 2.8%, better than expectation of 2.9%. Housing starts rose 9.9% yoy in July versus expectation of 4.8% yoy. Consumer confidence dropped slightly to 36.7 in August, below expectation of 37.4.

China PMI manufacturing dropped to 50.1, services tumbled to 47.5

China’s official PMI Manufacturing dropped slightly from 50.4 to 50.1 in August, below missed expectation of 50.2. PMI Non-Manufacturing dropped sharply from 53.3 to 47.5, well below expectation of 52.8, back in contraction for the first time since Q1 last year.

“This epidemic in multiple provinces and locations was a fairly big shock to the services industry, which is still in recovery,” said Zhao Qinghe, of China’s National Bureau of Statistics.

New Zealand ANZ business confidence dropped to -14.2 on Delta lockdown

New Zealand ANZ Business Confidence dropped sharply from -3.8 to -14.2 in August. Own Activity Outlook dropped from 26.3 to 19.2. Looking at some more details, export intentions ticked down from 7.6 to 7.4. Investment intentions dropped from 17.4 to 14.4. Employment intentions dropped from 21.4 to 17.0. Profit expectations dropped from 0.0 to -5.5. Inflation expectations, however, rose further from 2.70 to 3.05, above RBNZ’s target band. ANZ said that the “initial responses after level 4 lockdown look encouragingly robust”.

Also released, New Zealand building permits rose 2.1% mom in July.

From Australia, current account surplus widened to AUD 20.5B in Q2, versus expectation of AUD 21.0B. Private sector credit rose 0.7% mom in July versus expectation of 0.5% mom. Building permits dropped -8.6% mom, versus expectation of -5.0% mom.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1783; (P) 1.1797; (R1) 1.1810; More…

Intraday bias in EUR/USD stays on the upside at this point. Rebound from 1.1663 short term bottom is on track to 1.1907 resistance. Decisive break there will indicate that fall from 1.2265, as well as the consolidation pattern from 1.2348, have completed. Near term outlook will be turned bullish for 1.2265/2348 resistance. On the downside, break of 1.1782 minor support will mix up the near term outlook and turn intraday bias neutral first.

In the bigger picture, rise from 1.0635 is seen as the third leg of the pattern from 1.0339 (2017 low). Further rally remains in favors long as 1.1602 support holds, to cluster resistance at 1.2555 next, (38.2% retracement of 1.6039 to 1.0339 at 1.2516). However sustained break of 1.1602 will argue that the rise from 1.0635 is over, and turn medium term outlook bearish again. Deeper fall would be seen to 61.8% retracement of 1.0635 to 1.2348 at 1.1289 and below.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Building Permits M/M Jul | 2.10% | 3.80% | 4.00% | |

| 23:30 | JPY | Unemployment Rate Jul | 2.80% | 2.90% | 2.90% | |

| 23:50 | JPY | Industrial Production M/M Jul P | -1.50% | -2.50% | 6.50% | |

| 01:00 | CNY | NBS Manufacturing PMI Aug | 50.1 | 50.2 | 50.4 | |

| 01:00 | CNY | Non-Manufacturing PMI Aug | 47.5 | 52.8 | 53.3 | |

| 01:00 | NZD | ANZ Business Confidence Aug | -14.2 | -3.8 | ||

| 01:30 | AUD | Current Account Balance (AUD) Q2 | 20.5B | 21.0B | 18.3B | 18.9B |

| 01:30 | AUD | Private Sector Credit M/M Jul | 0.70% | 0.50% | 0.90% | |

| 01:30 | AUD | Building Permits M/M Jul | -8.60% | -5.00% | -6.70% | -5.50% |

| 05:00 | JPY | Housing Starts Y/Y Jul | 9.90% | 4.80% | 7.30% | |

| 05:00 | JPY | Consumer Confidence Index Aug | 36.7 | 37.4 | 37.5 | |

| 06:45 | EUR | France Consumer Spending M/M Jul | -2.20% | 0.70% | 0.30% | |

| 06:45 | EUR | France GDP Q/Q Q2 | 1.10% | 0.90% | 0.90% | |

| 07:55 | EUR | Germany Unemployment Rate Aug | 5.50% | 5.60% | 5.70% | 5.60% |

| 07:55 | EUR | Germany Unemployment Change Aug | -53K | -34K | -91K | -90K |

| 08:30 | GBP | Mortgage Approvals Jul | 75K | 79K | 81K | |

| 08:30 | GBP | M4 Money Supply M/M Jul | 0.10% | 0.60% | 0.50% | 0.60% |

| 09:00 | EUR | Eurozone CPI Y/Y Aug P | 3.00% | 2.80% | 2.20% | |

| 09:00 | EUR | Eurozone CPI Core Y/Y Aug P | 1.60% | 1.50% | 0.70% | |

| 12:30 | CAD | GDP M/M Jun | 0.70% | 0.70% | -0.30% | |

| 13:00 | USD | S&P/Case-Shiller Composite-20 HPI Y/Y Jun | 17.50% | 17.00% | ||

| 13:00 | USD | Housing Price Index M/M Jun | 2.10% | 1.70% | ||

| 13:45 | USD | Chicago PMI Aug | 69.8 | 73.4 | ||

| 14:00 | USD | Consumer Confidence Aug | 123.3 | 129.1 |

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals