Sterling rebounds strongly after two BoE MPC member voted for tapering. Also, recent developments strengthened the case of modest tightening. Commodity currencies are also firmer following mild rebound in the stock markets. On the other hand, Yen, Swiss Franc and Dollar turned softer on improvement overall risk sentiment. But for now, the Pound is still the worst performing for the week while Swiss Franc is the strongest.

Technically, GBP/USD’s break of 1.3691 minor resistance suggests that fall from 1.3912 has completed, and stronger rise could be seen to retest this resistance. Similarly, GBP/JPY’s break of 150.80 minor resistance suggests that stronger rise would be seen to 152.82 resistance. Focus will be on whether EUR/GBP would break through 0.8499 to target a test on 0.8448 low. Overall, there is prospect of a turnaround in Sterling.

In Europe, at the time of writing, FTSE is down -0.09%. DAX is up 0.70%. CAC is up 0.74%. Germany 10-year yield is up 0.0432 at -0.279. Earlier in Asia, Japan was on holiday. Hong Kong HSI rose 1.19%. China Shanghai SSE rose 0.38%. Singapore Strait Times rose 0.93%.

US initial jobless claims rose to 351k, above expectations

US initial jobless claims rose 16k to 351k in the week ending September 18, above expectation of 317k. Four-week moving average of initial claims dropped -750 to 335.75k.

Continuing claims rose 131k to 2845k. Four-week moving average of continuing claims dropped -16k to 2804k, lowest since March 21, 2020.

Canada retail sales dropped -0.6% mom in Jul, estimated to rebound in August

Canada retail sales dropped -0.6% to CAD 55.8B in July, better than expectation of -1.2% mom fall. That’s the third decrease in four months, driven by lower sales at food and beverage stores (-3.4%) and building material and garden equipment and supplies dealers (-7.3%). Sales decreased in 5 of 11 subsectors. Based on advance estimates, sales rose 2.1% mom in August.

BoE stands pat, Ramsden and Saunders voted for taper

BoE voted unanimously to keep Bank Rate unchanged at 0.10%. However, it voted 7-2 to keep the government bond purchase target at GBP 895B. Dave Ramsden and Michael Saunders voted to lower purchase target to GBP 860B.

In the statement, it said that since August meeting, “the pace of recovery of global activity has showed signs of slowing”, “global inflationary pressures have remained strong”, and “there are some signs that cost pressures may prove more persistent”.

BoE reiterated that “some modest tightening of monetary policy over the forecast period was likely to be necessary”. Developments since August “appear to have strengthened that case”.

“The Committee will be monitoring closely the incoming evidence regarding developments in the labour market, and particularly unemployment, wider measures of slack and underlying pay pressures; the extent to which businesses pass on wage and other cost increases, as well as medium-term inflation expectations.”

UK PMI composite dropped to 54.1, heading towards a bout of stagflation

UK PMI Manufacturing dropped from 60.3 to 56.3 in September, below expectation of 59.0, a 7-month low. PMI Services dropped from 55.0 to 54.6, below expectation of 55.0, a 7-month low. PMI Composite dropped from 54.8 to 54.1, also a 7-month low.

Chris Williamson, Chief Business Economist at IHS Markit, said:

“The September PMI data will add to worries that the UK economy is heading towards a bout of ‘stagflation’, with growth continuing to trend lower while prices surge ever higher.

“While there are clear signs that demand is cooling since peaking in the second quarter, the survey also points to business activity being increasingly constrained by shortages of materials and labour, most notably in the manufacturing sector but also in some services firms. …

“Shortages are meanwhile driving up prices at unprecedented rates as firms pass on higher supplier charges and increases in staff pay…

“Business expectations for the year ahead are meanwhile down to their lowest since January, with concerns over both supply and demand amid the ongoing pandemic casting a shadow over prospects for the economy as we move into the autumn.”

Eurozone PMI composite dropped to 56.1, unwelcome combination of sharply slower economic growth and steeply rising prices

Eurozone PMI Manufacturing dropped from 61.5 to 58.7 in September, below expectation of 60.4, a 7-month low. PMI Services dropped from 59.0 to 56.3, below expectation of 58.4, a 4-month low. PMI Composite dropped from 59.0 to 56.1, a 5-month low.

Chris Williamson, Chief Business Economist at IHS Markit said:

“September’s flash PMI highlights an unwelcome combination of sharply slower economic growth and steeply rising prices.

“On one hand, some cooling of growth from the two-decade highs seen earlier in the summer was to be expected. On the other hand, firms have become increasingly frustrated by supply delays, shortages and ever-higher prices for inputs. Businesses, most notably in manufacturing but also now in the service sector, are being constrained as a result, often losing sales and customers.

“Concerns over high prices, stressed supply chains and the resilience of demand in the ongoing pandemic environment has consequently eroded business confidence, with expectations for the year ahead now down to the lowest since January.

“For now, the overall rate of expansion remains solid, despite slowing, but growth looks likely to weaken further in coming months if the price and supply headwinds show no signs of abating, especially if accompanied by any rise in virus cases as we head into the autumn.”

Germany PMI Manufacturing dropped from 62.6 to 58.5 in September, below expectation of 61.3, an 8-month low. PMI Services dropped from 60.8 to 56.0, below expectation of 60.3, a 4-month low. PMI Composite dropped from 60.0 to 55.3, a 7-month low.

France PMI Manufacturing dropped from 57.5 to 55.2 in September, below expectation of 57.3, lowest in 8 months. PMI Services dropped slightly from 56.3 to 56.0, below expectation of 56.0, lowest in 5 months. PMI Composite dropped from 56.9 to 55.1, lowest in 5 months.

SNB stands pat, upgrades inflation forecasts slightly

SNB kept sight deposit rate unchanged at -0.75% today. Also, it remained “remains willing to intervene in the foreign exchange market as necessary, in order to counter upward pressure on the Swiss franc.” It also reiterated that “the Swiss franc remains highly valued”.

The new conditional inflation forecast for 2021 is raised to 0.5% in 2021 (up from June’s 0.4%). For 2022, it’s raised to 0.7% (from 0.6%). For 2023, it’s kept unchanged at 0.6%. SNB said it’s “primarily due to somewhat higher prices for oil products as well as for goods affected by supply bottlenecks.”

SNB also said, in the baseline scenario, it anticipated a “continuation of the economic recovery”, assuming pandemic containment measures will not need to be tightened significantly again. GDP is expected to grow around 3% in 2021, downwardly revised, attributable to “less dynamically than expected” development of consumer-related industries. GDP is expected to return to pre-crisis level in H2. But overall production capacity will “remain underutilised for some time yet”.

Australia PMI composite rose to 46.0, early signs of a turning point

Australia PMI Manufacturing rose from 52.0 to 57.3 in September, hitting a 3-month high. PMI Services also rose from 42.9 to 44.9, staying in contraction but hit a 3-month high. PMI Composite rose from 43.3 to 46.0.

Jingyi Pan, Economics Associate Director at IHS Markit, said: “The extension of COVID-19 restrictions into September continued to dampen business conditions in the Australian private sector, although the slight easing of restrictions was picked up in the latest IHS Markit Flash Australia Composite PMI, seeing the overall Composite Output Index contracting at a slower rate in September. This may also be suggesting that we are looking at early signs of a turning point.

“The employment index meanwhile pointed to higher workforce levels, which was a positive sign following the decline recorded in August, driven by the severe COVID-19 disruptions. That said, price pressures intensified once again for Australian private sector firms while evidence of worsening supply constraints gathered, all of which remains a focal point for the Australian economy.”

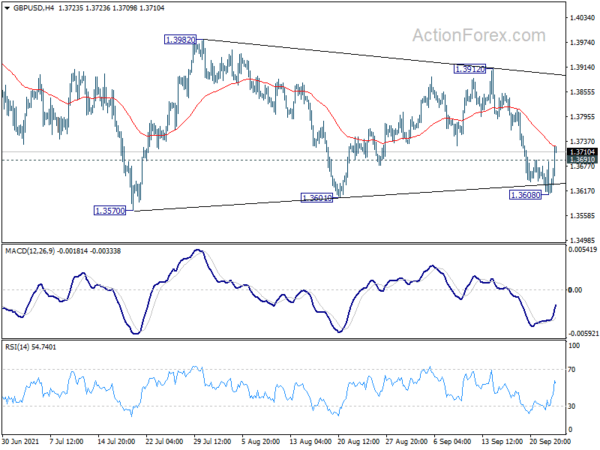

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3588; (P) 1.3639; (R1) 1.3668; More…

GBP/USD’s break of 1.3691 minor resistance argues that fall form 1.3912 might have completed at 1.3608, after defending 1.3570/3601 support zone. Intraday bias is back on the upside for 1.3912 resistance. On the downside, however, break of 1.3570 will target 1.3482 key support level. Sustained break there will carry larger bearish implication and target 1.3163 fibonacci level.

In the bigger picture, as long as 1.3482 resistance turned support holds, we’d still treat price actions from 1.4248 as a corrective move. That is, up trend from 1.1409 (2020 low) is in favor to resume. Decisive break of 1.4376 key resistance (2018 high) would indeed carry long term bullish implications. However, sustained break of 1.3482 will at least bring deeper fall to 38.2% retracement of 1.1409 to 1.4248 at 1.3164, or even further to 61.8% retracement at 1.2493.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:00 | AUD | Manufacturing PMI Sep P | 57.3 | 52 | ||

| 23:00 | AUD | Services PMI Sep P | 44.3 | 42.9 | ||

| 07:15 | EUR | France Manufacturing PMI Sep P | 55.2 | 57.3 | 57.5 | |

| 07:15 | EUR | France Services PMI Sep P | 56 | 56.1 | 56.3 | |

| 07:30 | CHF | SNB Interest Rate Decision | -0.75% | -0.75% | ||

| 07:30 | EUR | Germany Manufacturing PMI Sep P | 58.5 | 61.3 | 62.6 | |

| 07:30 | EUR | Germany Services PMI Sep P | 56 | 60.3 | 60.8 | |

| 08:00 | EUR | Eurozone Manufacturing PMI Sep P | 58.7 | 60.4 | 61.4 | |

| 08:00 | EUR | Eurozone Services PMI Sep P | 56.3 | 58.4 | 59 | |

| 08:00 | EUR | ECB Economic Bulletin | ||||

| 08:30 | GBP | Manufacturing PMI Sep P | 56.3 | 59 | 60.3 | |

| 08:30 | GBP | Services PMI Sep P | 54.6 | 55 | 55 | |

| 11:00 | GBP | BoE Interest Rate Decision | 0.10% | 0.10% | 0.10% | |

| 11:00 | GBP | BoE Asset Purchase Facility | 875B | 875B | 875B | |

| 11:00 | GBP | MPC Official Bank Rate Votes | 0–0–9 | 0–0–9 | 0–0–8 | |

| 11:00 | GBP | MPC Asset Purchase Facility Votes | 0–2–7 | 0–1–8 | 0–1–7 | |

| 12:30 | CAD | Retail Sales M/M Jul | -0.60% | -1.20% | 4.20% | |

| 12:30 | CAD | Retail Sales ex Autos M/M Jul | -1.00% | -1.50% | 4.70% | 4.80% |

| 12:30 | USD | Initial Jobless Claims (Sep 17) | 351K | 317K | 332K | 335K |

| 13:45 | USD | Manufacturing PMI Sep P | 61.1 | 61.1 | ||

| 13:45 | USD | Services PMI Sep P | 55.1 | 55.1 | ||

| 14:30 | USD | Natural Gas Storage | 76B | 83B |

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals