Dollar retreats mildly in quiet Asian session today, but loss is limited. Some consolidations will likely be seen and further rally in the greenback is still likely to follow. Yen is also slightly softer after worse than expected GDP data. On the other hand, Swiss Franc and Euro are trading mildly higher while Aussie is also recovering. Overall, Asian stocks are treading water, WTI oil is defending 80 handle while Gold is in sideway consolidation.

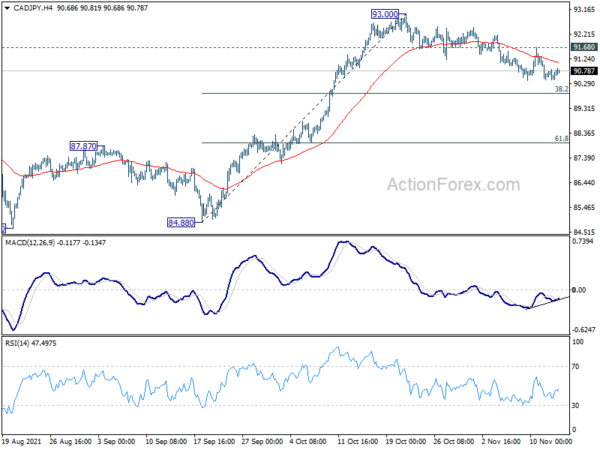

Technically, one focus for the week is whether commodity-yen crosses would finish near term corrective fall and stage rebounds this week. AUD/JPY is defending 55 day EMA and break of 84.16 minor resistance will likely bring stronger rise back to retest 86.24 high. Similarly, break of 91.68 minor resistance in CAD/JPY will suggest completion of pullback from 93.00, and bring retest of this high.

In Asia, at the time of writing, Nikkei is up 0.43%. Hong Kong HSI is down -0.08%. China Shanghai SSE is down -0.29%. Singapore Strait Times is up 0.20%. Japan 10-year JGB yield is down -0.0062 at 0.070.

Japan GDP contracted -0.8% qoq, -3.0% annualized in Q3

Japan GDP contracted -0.8% qoq in Q3, much worse than expectation of -0.2% qoq. In annualized term, GDP dropped -3.0% qoq, much worse than expectation of -0.8%.

Capital expenditure dropped -0.8% qoq, versus expectation of -0.6% qoq. External demand rose 0.1% qoq, versus expectation of 0.0% qoq. Private consumption dropped -1.1% qoq, versus expectation of -0.5% qoq. GDP price index dropped -1.1%, slightly better than expectation of -1.2%.

Economy minister Daishiro Yamagiwa said pace of pickup in the economy is weakening and policy support is needed. He also warned of downside risks from the global supply constraints. Prime Minister Fumio Kishida is expected to reveal a stimulus package “worth several tens of trillion yen” later this week on November 19.

BoJ Kuroda: Recovery mechanism maintained, inflation to hit 1% mid 2022

In a speech with business leaders, BoJ Governor Haruhiko Kuroda said that CPI is likely to “increase moderately in positive territory for the time being”, reflecting rise in energy prices. Thereafter, “it is projected to increase gradually to about 1 percent as the output gap turns positive around the middle of next year.”

He noted that economic recovery in Japan has been “somewhat slower than initially expected”. Nevertheless “the mechanism for economic recovery has been maintained.”

Real GDP is expected to recovery to pre-pandemic level in the first half of 2022. Thereafter, “as the resumption of economic activity progresses while public health is being protected, Japan’s economy is expected to follow a growth path that outpaces its potential growth rate, supported by relatively high growth in overseas economies and accommodative financial conditions.”

China industrial production rose 3.5% yoy in Oct, retail sales up 4.9% yoy

China industrial production rose 3.5% yoy in October, above expectation of 3.0% yoy. Retail sales rose 4.9% yoy, versus expectation of 3.8% yoy. Fixed asset investment rose 6.1% ytd yoy, versus expectation of 6.2%.

“The national economy was generally stable and maintained the trend of recovery,” the NBS said in a statement. “However, we must be aware that the international environment is still complicated and severe with many unstable and uncertain factors.”

Inflation and retail sales to highlight the week

Inflation data will catch most attention this week, with CPI from UK, Canada and Japan featured. UK, Germany and will New Zealand release PPI. Additionally, eyes will be on retail sales from US, UK and Canada. Other data to watch include a batch of data from China, regional Fed surveys and UK employment.

Here are some highlights for the week:

- Monday: Japan GDP; China retail sales, fixed asset investment, industrial production; Eurozone trade balance; Canada manufacturing sales, wholesale sales; US Empire State manufacturing index.

- Tuesday: RBA minutes; Japan tertiary industry index; UK employment; Eurozone GDP, employment; Canada housing starts; US retail sales, import prices, industrial production, business inventories, NAHB housing index.

- Wednesday: New Zealand PPI; Australia wage price index; Japan trade balance, machine orders; UK CPI, PPI; Eurozone CPI final; Canada CPI; US building permits and housing starts.

- Thursday: New Zealand inflation expectations; Swiss trade balance; US Philly Fed manufacturing index, jobless claims.

- Friday: Japan CPI; UK Gfk consumer sentiment, retail sales, public sector net borrowing; Germany PPI; Eurozone current account; Canada retail sales, new housing price index.

AUD/USD Daily Report

Daily Pivots: (S1) 0.7294; (P) 0.7314; (R1) 0.7352; More…

Intraday bias in AUD/USD remains neutral for the consolidation above 0.7275 temporary low. But further decline is in favor as long as 0.7431 minor resistance holds. Rebound from 0.7105 could be complete with three waves up to 0.7555, and fall from 0.8006 is still in progress. On the downside, below 0.7275 will target 0.7169 support first, and then 0.7105. However, break of 0.7431 resistance will turn bias back to the upside for retesting 0.7555.

In the bigger picture, with 0.6991 cluster support (38.2% retracement of 0.5506 to 0.8006 at 0.7051) intact, we’re seeing price action from 0.8006 as a correction only. That is, up trend from 0.5506 low would resume after the correction completes. In that case, main focus will be 0.8135 key resistance (2018 high). Sustained break there will carry larger bullish implications. However, sustained break of 0.6991 will argue that the whole medium term trend has indeed reversed.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | GDP Q/Q Q3 P | -0.80% | -0.20% | 0.50% | |

| 23:50 | JPY | GDP Price Index Q3 P | -1.10% | -1.20% | -1.10% | |

| 00:01 | GBP | Rightmove House Price Index M/M Nov | -0.60% | 1.80% | ||

| 02:00 | CNY | Retail Sales Y/Y Oct | 4.90% | 3.80% | 4.40% | |

| 02:00 | CNY | Industrial Production Y/Y Oct | 3.50% | 3.00% | 3.10% | |

| 02:00 | CNY | Fixed Asset Investment YTD Y/Y Oct | 6.10% | 6.20% | 7.30% | |

| 04:30 | JPY | Industrial Production M/M Sep F | -5.40% | -5.40% | -5.40% | |

| 10:00 | EUR | Eurozone Trade Balance (EUR) Sep | 12.5B | 11.1B | ||

| 13:30 | CAD | Manufacturing Sales M/M Sep | -3.00% | 0.50% | ||

| 13:30 | CAD | Wholesale Sales M/M Sep | 1.10% | 0.30% | ||

| 13:30 | USD | Empire State Manufacturing Index Nov | 20.2 | 19.8 |

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals