Euro’s recovery was rather short-lived as selling returns after dovish comments from ECB president. Also, Austria returned to full lockdown while Germany may follow on the fourth wave of COVID-19 infections. Yen rises broadly today as risk sentiments turn sour. For the week, Euro remains the worst performer, followed by Aussie. Sterling is still the best performer, followed by Yen and then Dollar.

Technically, EUR/CHF should have taken out 1.5050 key long term support decisively. Current down trend should now target 161.8% projection of 1.1149 to 1.0694 from 1.0936 at 1.0200. We’ll now see if selling in EUR/UISD would pick up below 1.13 handle.

In Europe, at the time of writing, FTSE is down -0.59%. DAX is down -0.65%. CAC is down -0.85%. Germany 10-year yield is down -0.056 at -0.331. Earlier in Asia, Nikkei rose 0.50%. Hong Kong dropped -1.07%. China Shanghai SSE rose 1.13%. Singapore Strait Times dropped -0.14%. Japan 10-year JGB yield dropped -0.0042 to 0.079.

Canada retail sales dropped -0.6% mom in Sep, better than expectation

Canada retail sales dropped -0.6% mom to CAD 56.6B in September, better than expectation of -1.6% mom decline. The contraction was led by sales at motor vehicle and parts dealers (-1.6%) as new car dealer sales (-2.8%) continued to struggle amid global supply shortages for semiconductor chips. Sales dropped in 7 of 11 subsectors, representing 63.5% of retail trade. Excluding gasoline stations and motor vehicle and parts, sales dropped -0.3% mom. In October, advance estimate shows a 1.0% mom rebound in sales.

Also from Canada, new housing price index rose 0.9% mom in October, above expectation of 0.5% mom.

ECB Lagarde: Doesn’t make sent to react to current inflation by tightening policy

In a speech, ECB President Christine Lagarde said that the central bank focus on “medium term, not on current inflation numbers”. “When inflation pressure is expected to fade – as is the case today – it does not make sense to react by tightening policy,” she added. “The tightening would not affect the economy until after the shock has already passed.”

Lagarde also said, “supply shock” will tend to “push up inflation and depress output. In this case, “tighter monetary policy would only exacerbate the contractionary effect on the economy.” The Eurozone is facing a “mixture of shocks”, partly related to catch-up demand but has a “strong supply-driven element”. “Tightening policy prematurely would only make this squeeze on household incomes worse.”

“The conditions to raise rates are very unlikely to be satisfied next year,” she said. “Moreover, even after the expected end of the pandemic emergency, it will still be important for monetary policy – including the appropriate calibration of asset purchases – to support the recovery and the sustainable return of inflation to our target of 2%.”

Also from Eurozone, current account surplus widened to EUR 18.7B in September. Germany PPI came in at 3.8% mom, 18.4% yoy, well above expectation of 1.2% mom, 12.7% yoy.

BoE Pill: No quick fix on inflation means patience required

BoE Chief Economist Huw Pill said in a conference today that there is “no quick fix” on inflation. He added, ” lack of a quick fix means some patience will be required.” He also said he had not made up his mind whether he would vote for a rate hike in December’s meeting.

He added that policy communications was getting more complicated due to the two-side risks to both growth and inflation outlook. But, he said the central wanted to “train” the markets to focus more on the medium-term outlook and the two-side risks. Also, Some volatility was unavoidable give the uncertainty regarding the precise timing of the rate hikes.

UK retail sales rose 0.8% mom in Oct, ex-fuel sales grew 1.6% mom

UK retail sales grew 0.8% mom in October, above expectation of 0.5% mom. Ex-fuel sales jumped 1.6% mom, above expectation of 0.2% mom.

However, over the three months to October, sales volumes dropped -2.3% when compared with the previous three months. Compared with the same period a year earlier, sales volumes over the last three months dropped -0.5%.

Retail sales values, unadjusted for price changes, rose by 1.6% in October 2021, following an increase of 0.2% in September. Over the last three months to October 2021, the value of sales was up 3.3% on the same period a year earlier, reflecting an annual retail sales implied price deflator of 3.8%.

UK GfK consumer confidence rose to -14 despite higher inflation

UK GfK consumer confidence rose from -17 to -14 in November, better than expectation of -16. Expectation of personal financial situation over the next 12 months rose 1pt to 2. Expectation of general economic situation over the next 12 months rose 3 pts to -23.

Joe Staton, Client Strategy Director GfK, comments:”Headline consumer sentiment has ticked upwards this month despite decade-high inflation, fears of higher prices and worries over rising interest rates, and as the deepening cost-of-living squeeze leaves UK household finances worse off this winter.

Also released, UK public sector net borrowing dropped to GBP 18.0 in October.

Japan CPI core rose 0.1% yoy in Oct, second month of rise

Japan all-time CPI dropped from 0.2% yoy to 0.1% yoy in October. CPI core (all-item ex food) was unchanged at 0.1% yoy. CPI core-core (all-item ex food and energy), dropped further from -0.5% yoy to -0.7% yoy.

The CPI core reading is now rising for the second straight month. Overall energy prices rose 11.3%. Gasoline prices surged at highest rate in over 13 years, up 21.4%, while kerosene also rose 25.9%. Accommodation fees gained 59.1%.

But CPI core-core was negative for the seventh straight month, as weighed down by record -53.6% fall in mobile communications fees.

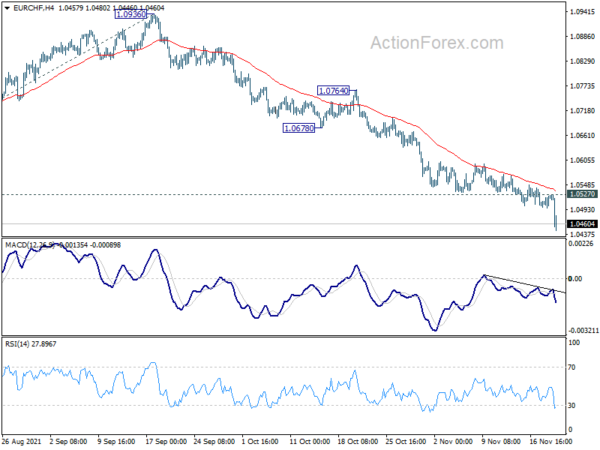

EUR/CHF Mid-Day Outlook

Daily Pivots: (S1) 1.0507; (P) 1.0517; (R1) 1.0536; More….

EUR/CHF’s down trend resumes and hits as long as 1.0446 so far. The break of 1.0505 long term support should confirm resumption of long term down trend. Intraday bias is back on the downside for 161.8% projection of 1.1149 to 1.0694 from 1.0936 at 1.0200 next. On the upside, above 1.0527 minor resistance will turn intraday bias neutral and bring consolidations first, before staging another decline.

In the bigger picture, current downside momentum argues that fall from 1.1149 is probably resuming the down trend from 1.2004 (2018 high). Focus is now on 1.0505 (2020 low). Decisive break there will confirm this bearish case and target 61.8% projection of 1.2004 to 1.0505 to 1.1149 at 1.0223 next. Strong support from 1.0505 will bring rebound first. But outlook will stay bearish as long as 1.0936 resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | National CPI Core Y/Y Oct | 0.10% | 0.10% | 0.10% | |

| 00:01 | GBP | GfK Consumer Confidence Nov | -14 | -16 | -17 | |

| 07:00 | EUR | Germany PPI M/M Oct | 3.80% | 1.20% | 2.30% | |

| 07:00 | EUR | Germany PPI Y/Y Oct | 18.40% | 12.70% | 14.20% | |

| 07:00 | GBP | Retail Sales M/M Oct | 0.80% | 0.50% | -0.20% | 0.00% |

| 07:00 | GBP | Retail Sales Y/Y Oct | -1.30% | -0.40% | -1.30% | -0.60% |

| 07:00 | GBP | Retail Sales ex-Fuel M/M Oct | 1.60% | 0.20% | -0.60% | -0.40% |

| 07:00 | GBP | Retail Sales ex-Fuel Y/Y Oct | -1.90% | -3.10% | -2.60% | -1.90% |

| 09:00 | EUR | Eurozone Current Account (EUR) Sep | 18.7B | 16.2B | 13.4B | 17.1B |

| 09:30 | GBP | Public Sector Net Borrowing (GBP) Oct | 18.0B | 22.3B | 21.0B | 19.9B |

| 13:30 | CAD | Retail Sales M/M Sep | -0.60% | -1.60% | 2.10% | |

| 13:30 | CAD | Retail Sales ex Autos M/M Sep | -0.20% | -1.00% | 2.80% | |

| 13:30 | CAD | New Housing Price Index M/M Oct | 0.90% | 0.50% | 0.40% |

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals