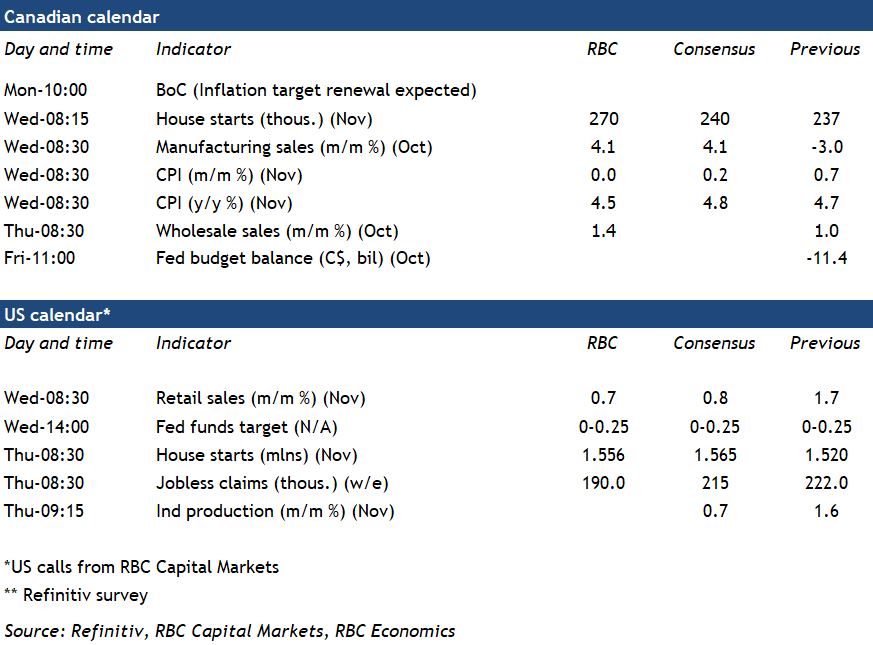

Last month’s year-over-year growth rate in Canadian CPI likely ticked down to 4.5% from 4.7% in October, when it hit a two-decade high. Gas prices have eased from October, but were still up more than 40% from a year ago in November. That accounts for more than a quarter of the growth rate we’re anticipating. Meat prices could pull back from very high levels—wholesale beef prices dropped 18% over September and October, for example. But we expect food price growth to be little changed at close to 4% overall. Annual growth in prices ex-food and energy products will likely stay just above 3%, as tight housing markets keep pressure on housing replacement costs and realtor/broker fees.

Distortions from pandemic base-effects (unusually low year-ago prices) continue to influence the inflation reading and accounted for around 2% of the total 4.7% annual price growth in October. Those anomalies will fade next year, but the share of the consumer price basket growing at a rate above the Bank of Canada’s 2% inflation target has also been edging higher compared to pre-pandemic levels. Barring major disruptions from Omicron, we expect household demand to continue to firm—backstopped by tightening labour markets and a large stockpile of pandemic savings. That will keep a floor under price growth. The Bank of Canada is expected to announce an updated policy mandate on Monday that will reiterate a commitment to the current 2% inflation target. The new mandate will also reportedly include more explicit language around how the central bank is considering labour market conditions in policy decisions. But labour markets have already improved dramatically, and with inflation running hotter, the number of reasons to keep interest rates at emergency low levels is getting very small. We continue to expect the central bank to begin hiking interest rates starting in April.

Week ahead data watch:

- US FOMC meeting: The Federal Reserve Board will release new economic projections and a rate decision next week. No change in the fed funds target range is expected, but we’ll be watching for any change in the expected timing and pace of future rate hikes.

- Canadian manufacturing sales: preliminary estimates for October manufacturing sales showed a 4.1% increase driven by a rebound in motor vehicle shipments (+61%) from sharply reduced levels in September when the global semiconductor shortage forced factories to temporarily stop production.

- Canadian home resales: early reports out of major regional markets are pointing to rising prices with strong demand for purchases held back by limited supply available.

US retail sales are expected to have ticked up again in November on firm holiday shopping and a jump in gasoline prices that should push gas station receipts higher.

reports.

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals