Dollar’s post CPI selloff continues today and remains generally weak. For now, Swiss Franc is the second worst performer for the week, followed by Euro. Commodity currencies are the strongest, with Aussie overtaking Canadian. Sterling is mixed for now. Other markets are mixed for now, with Asian stocks lacking a clear direction. Global benchmark yields are retreating slightly. Gold and Silver, though, are firm together with oil.

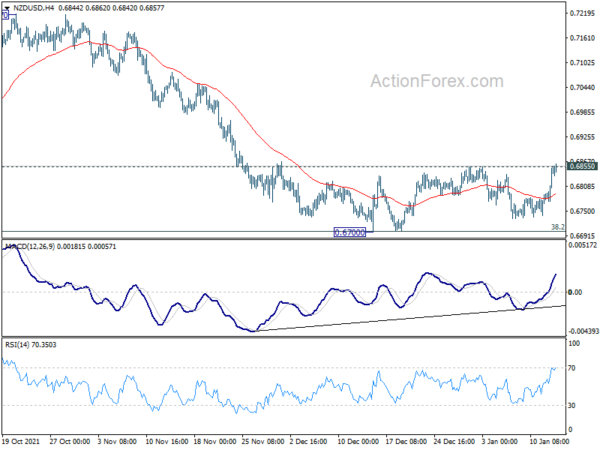

Technically, USD/CAD took the lead by breaking through 1.2619 support to resume the fall from 1.2963 earlier in the week. AUD/USD followed yesterday by breaking 0.7277 resistance to resume the rebound from 0.6992. Now, it’s NZD/USD’s turn to break through 0.6855 resistance firmly to resume the rebound from 0.6700.

In Asia, at the time of writing, Nikkei is down -0.77%. Hong Kong HSI is down -0.09%. China Shanghai SSE is down -0.50%. Singapore Strait Times is down -0.08%. Japan 10-year JGB yield is up 0.0041 at 0.133. Overnight, DOW rose 0.11%. S&P 500 rose 0.28%. NASDAQ rose 0.23%. 10-year yield dropped -0.021 to 1.725.

Dollar breaks 95 in steep fall, to draw support from 93.97 fib level

Dollar index tumbled sharply overnight and dived through 55 day EMA to close at 94.91. At this point, price actions from 96.93 are seen as a correction only. Hence, we’d look for strong support at 38.2% retracement of 89.20 to 96.93 at 93.97 to contain downside. The level is also close to 55 week EMA at 93.77. That would set the base for resuming the up trend from 89.20 through 96.93 at a later stage.

However, sustained break of 93.97 will argue that rise from 89.20 has already completed at 96.93. The three wave structure in turn suggests that it’s a correction to the down trend from 102.99. Such development, together with the index back below 55 week EMA, would be rather bearish and could set up another medium term fall through 89.20 later in the year.

Fed Bullard: March hike is a definite possibility

St. Louis Fed President James Bullard said Fed “could begin increasing the policy rate as early as the March meeting in order to be in a better position to control inflation.” He added, ” it makes sense to get going sooner rather than later and so I think March would be a definite possibility.”

“We need to risk manage here. We need to be prepared for the case where inflation does not moderate as much as hoped and instead the Fed has to come in and move inflation closer to the 2% target. How much the Fed has to do and how much natural moderation there will be is very much an open question,” he said.

Separately, Bullard also told WSJ, “I actually now think we should maybe go to four hikes in 2022.”

Fed Daly: Time to start removing policy accommodation

San Francisco Fed President Mary Daly said inflation is “uncomfortably high” in the US. And, it’s time to “start removing some of the accommodation we’ve been giving to the economy,”

“I definitely see rate increases coming, as early as March even,” she noted. But she didn’t want to predict the number of rate hikes needed for this year.

Fed Brainard: Policy focused on getting inflation back down to 2%

In the nomination hearing for Fed Vice Chair position, Lael Brainard said, “we are seeing the strongest rebound in growth and decline in unemployment of any recovery in the past five decades.”

“But inflation is too high, and working people around the country are concerned about how far their paychecks will go,” she added. “Our monetary policy is focused on getting inflation back down to 2% while sustaining a recovery that includes everyone. This is our most important task.”

Looking ahead

ECB will release monthly economic bulletin today. US will release PPI and jobless claims.

AUD/USD Daily Report

Daily Pivots: (S1) 0.7226; (P) 0.7259; (R1) 0.7318; More…

AUD/USD’s rebound from 0.6992 resumed by breaking through 0.7277 resistance. The development revives the case that correction form 0.8006 has completed after defending 0.6991. Intraday bias is back on the upside for 100% projection of 0.6992 to 0.7277 from 0.7128 at 0.7413 first. For now, further rally will remain in favor as long as 0.7128 support holds, in case of retreat.

In the bigger picture, strong rebound from 0.6991 key structural support will retain medium term bullishness. That is, whole up trend from 0.5506 is still in progress. Firm break of 0.7555 resistance will target 0.8006 high and above. However, sustained break of 0.6991 will argue that the whole up trend from 0.5506 might be finished at 0.8006, after rejection by 0.8135 long term resistance. Deeper decline would then be seen back to 61.8% retracement of 0.5506 to 0.8006 at 0.6461.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Building Permits M/M Nov | 0.60% | -2.00% | -2.10% | |

| 23:50 | JPY | Money Supply M2+CD Y/Y Dec | 3.70% | 3.90% | 4.00% | |

| 06:00 | JPY | Machine Tool Orders Y/Y Dec P | 64.00% | |||

| 09:00 | EUR | ECB Economic Bulletin | ||||

| 13:30 | USD | PPI M/M Dec | 0.40% | 0.80% | ||

| 13:30 | USD | PPI Y/Y Dec | 9.80% | 9.60% | ||

| 13:30 | USD | PPI Core M/M Dec | 0.40% | 0.70% | ||

| 13:30 | USD | PPI Core Y/Y Dec | 8.00% | 7.70% | ||

| 13:30 | USD | Initial Jobless Claims (Jan 7) | 213K | 207K | ||

| 15:30 | USD | Natural Gas Storage | -175B | -31B |

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals