Overall, market sentiment is rather stable today, with major European indexes just slightly lower, while US futures point to recovery. Benchmark treasury yields are also ticking slightly higher. WTI crude oil is retreating slightly after breaking 115 handle. Gold is gyrating in tight range above 1900. In the currency markets, Euro remains the weakest one for today, followed by Sterling. Yen also softens on recovery yields. Aussie, Swiss Franc and Dollar are the stronger ones.

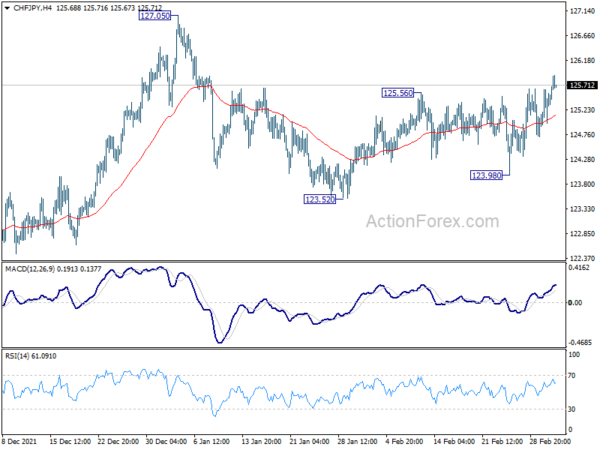

Technically, CHF/JPY is breaking out from near term range, resuming the rebound from 124.53. Further rise is mildly in favor to retest 127.05 high. With solid support from 55 day EMA too, the larger up trend could be ready to resume through 127.05. Swiss Franc might have an upper hand in safe haven flows, with help from Euro selloff.

In Europe, at the time of writing, FTSE is down -0.88%. DAX is down -0.57%. CAC is up 0.05%. Germany 10-year yield is up 0.037 at 0.066. Earlier in Asia, Nikkei rose 0.70%. Hong Kong HSI rose 0.55%. China Shanghai SSE dropped -0.09%. Singapore Strait Times rose 0.29%. Japan 10-year JGB yield rose 0.352 to 0.169.

US initial jobless claims dropped to 215k, better than expectation

US initial jobless claims dropped -18k to 215k in the week ending February 25, better than expectation of 235k. Four-week moving average of initial claims dropped -5k to 230.5k.

Continuing claims rose 2k to 1476k in the week ending February 19. Four-week moving average of continuing claims dropped -36k to 1540k, lowest since April 4, 1970.

ECB accounts: Main risk is tightening monetary policy too late

In the accounts of February ECB meeting, it was argued that monetary policy in the current environment was to “ensure that inflation expectations remained firmly anchored ” and to “avoid the risk of the prevailing high inflation becoming entrenched.”

“Caution was expressed about basing the Governing Council’s assessment on wage data which were only available with a lag. In this environment, the main risk was no longer of tightening monetary policy too early but too late,” the accounts noted.

It’s also argued that “an earlier monetary policy normalisation would reduce the risk of abrupt tightening later on, which could potentially be associated with high economic and social costs.”

“In the light of the increased uncertainty and the heightened upside risks to the inflation outlook, the general view prevailed that the Governing Council should convey its increased alertness and should monitor incoming information carefully, in particular regarding second-round effects.”

Eurozone PPI at 5.2% mom, 30.6% yoy in Jan

Eurozone PPI rose 5.2% mom, 30.6% yoy in January, above expectation of 3.0% mom, 26.9% yoy. For the month, industrial producer prices increased by 11.6% in the energy sector, by 2.7% for intermediate goods, by 2.2% for durable consumer goods, by 1.6% for non-durable consumer goods and by 1.5% for capital goods. Prices in total industry excluding energy increased by 2.2%.

EU PPI rose 4.9% mom, 30.3% yoy. The highest monthly increases in industrial producer prices were recorded in Romania (+12.0%), Belgium (+10.2%) and Slovakia (+8.7%). Decreases were observed in Ireland (-11.4%), Sweden (-0.7%), Luxembourg (-0.3%), and Finland (-0.2%).

Eurozone unemployment rate dropped to 6.8% in January, EU down to 6.2%

Eurozone unemployment rate dropped from 7.0% to 6.8% in January, better than expectation of 6.9%. EU unemployment rate dropped from 6.3% to 6.2%.

Eurostat estimates that 13.346 million men and women in the EU, of whom 11.225 million in the euro area, were unemployed in January 2022. Compared with December 2021, the number of persons unemployed decreased by 216 000 in the EU and by 214 000 in the euro area. Compared with January 2021, unemployment decreased by 2.522 million in the EU and by 2.117 million in the euro area.

Eurozone PMI composite finalized at 55.5, commensurate with GDP growth in excess of 0.6%

Eurozone PMI Services was finalized at 55.8, up from January’s 51.1. PMI Composite was finalized at 55.5, up from January’s 52.3. That’s also the strongest reading since last September.

Looking at some member states, Ireland PMI Composite rose to 59.1, 3-month high. Spain rose to 56.5, 3-month high. Germany rose to 55.6, 6-month high. France rose to 55.5 while Italy rose to 53.6.

Chris Williamson, Chief Business Economist at IHS Markit said: “The survey data for February depict a eurozone economy that was regaining robust growth momentum ahead of the invasion of Ukraine. Business activity accelerated to a pace commensurate with GDP growth in excess of 0.6%, buoyed by a relaxation of virus restrictions…

“Though it remains early days to be assessing the impact of the war, growth prospects are also likely to have been hit by heightened risk aversion and new sanctions, dampening the rebound from the pandemic. With inflation risks rising and growth prospects waning, the Ukraine conflict adds to business and household headwinds for the coming months, and exacerbates the difficult juggling act of the ECB in controlling inflation while sustaining a robust economic recovery.”

Germany PMI Services was finalized at 55.8 in February, up from January’s 52.2. PMI Composite was finalized at 55.6, up from January’s 53.8. That’s also the highest level since last August.

France PMI Services was finalized at 55.5 in February, up from January’s nine-month low of 53.1. PMI Composite was finalized at 55.5, up from January’s nine-month low of 52.7.

UK PMI services finalized at 60.5 in Feb, composite at 59.9

UK PMI Services was finalized at 60.5 in February, up from January’s 54.1. That’s the highest level since last June. PMI Composite was finalized at 59.9, up from February’s 54.2.

Andrew Harker, Economics Director at IHS Markit: “The ebbing of the Omicron wave of the COVID-19 pandemic contributed to a rebound in growth in the UK service sector in February, with rates of expansion in activity and new business up sharply… Although the latest set of PMI data were encouraging, the inflationary picture still has the potential to limit growth, while it remains to be seen what impact the Russian invasion of Ukraine will have on the service sector and wider economy.”

BoJ Nakagawa: Core inflation may briefly hit 2% on energy, food and industrial goods

BoJ board member Junko Nakagawa said “for the time being, inflationary pressure will remain strong, mainly for energy, food and industrial goods.” Core consumer prices may “briefly rise close to 2%.”

However, “even if that happens, what’s important is to scrutinise the factors and whether Japan’s economic fundamentals are strong enough to make such price rises sustainable,” she said.

“Global financial markets remain jittery due to escalating tensions in Ukraine. We’re monitoring changes in developments carefully,” she added.

China Caixin PMI composite unchanged at 50.1, still under triple pressure

China Caixin PMI Services dropped from 51.4 to 50.2 in February. PMI Composite was unchanged at 50.1.

Wang Zhe, Senior Economist at Caixin Insight Group said: “Overall, the manufacturing PMI rose in February, while the services PMI fell, but both remained in positive territory. Demand in the manufacturing sector improved, while demand in the services sector was greatly affected by the epidemic….

“Under the “triple pressure” of demand contraction, supply shocks and weakening expectations, the economy’s recovery is still not robust. Stabilizing economic growth remains an important focus of the government.”

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1074; (P) 1.1109; (R1) 1.1159; More…

Intraday bias in EUR/USD remains on the downside for the moment. Current fall is part of the down trend from 1.2348. Next target is 61.8% projection of 1.2265 to 1.1120 from 1.1494 at 1.0786. On the upside, break of 1.1273 resistance is needed to be the first sign of bottoming. Otherwise, outlook stays bearish in case of recovery.

In the bigger picture, the decline from 1.2348 (2021 high) is expected to continue as long as 1.1494 resistance holds. Firm break of 1.0635 (2020 low) will raise the chance of long term down trend resumption and target a retest on 1.0339 (2017 low) next. Nevertheless, break of 1.1494 will maintain medium term neutral outlook, and extend range trading first.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | AUD | AiG Performance of Construction Index Feb | 53.4 | 45.9 | ||

| 00:30 | AUD | Building Permits M/M Jan | -27.90% | -3.00% | 8.20% | 9.80% |

| 00:30 | AUD | Trade Balance (AUD) Jan | 12.89B | 9.10B | 8.36B | 8.82B |

| 01:45 | CNY | Caixin Services PMI Feb | 50.2 | 50.9 | 51.4 | |

| 05:00 | JPY | Consumer Confidence Index Feb | 35.3 | 35 | 36.7 | |

| 07:30 | CHF | CPI M/M Feb | 0.70% | 0.30% | 0.20% | |

| 07:30 | CHF | CPI Y/Y Feb | 2.20% | 1.80% | 1.60% | |

| 08:45 | EUR | Italy Services PMI Feb | 52.8 | 48.9 | 48.5 | |

| 08:50 | EUR | France Services PMI Feb F | 55.5 | 57.9 | 57.9 | |

| 08:55 | EUR | Germany Services PMI Feb F | 55.8 | 56.6 | 56.6 | |

| 09:00 | EUR | Eurozone Services PMI Feb F | 55.5 | 55.8 | 55.8 | |

| 09:00 | EUR | Italy Unemployment Jan | 8.80% | 9.10% | 9.00% | |

| 09:30 | GBP | Services PMI Feb F | 60.5 | 60.8 | 60.8 | |

| 10:00 | EUR | Eurozone Unemployment Rate Jan | 6.80% | 6.90% | 7.00% | |

| 10:00 | EUR | Eurozone PPI M/M Jan | 5.20% | 3.00% | 2.90% | 3.00% |

| 10:00 | EUR | Eurozone PPI Y/Y Jan | 30.60% | 26.90% | 26.20% | 26.30% |

| 12:30 | EUR | ECB Monetary Policy Meeting Accounts | ||||

| 12:30 | USD | Challenger Job Cuts Y/Y Feb | -55.90% | -76.00% | ||

| 13:30 | USD | Initial Jobless Claims (Feb 25) | 215K | 235K | 232K | 233K |

| 13:30 | USD | Nonfarm Productivity Q4 | 6.60% | 6.50% | 6.60% | |

| 13:30 | USD | Unit Labor Costs Q4 | 0.90% | 0.40% | 0.30% | |

| 14:45 | USD | Services PMI Feb F | 56.7 | 56.7 | ||

| 15:00 | USD | ISM Services PMI Feb | 60.5 | 59.9 | ||

| 15:00 | USD | ISM Services Prices Paid Feb | 82.3 | |||

| 15:00 | USD | ISM Services Employment Index Feb | 52.3 | |||

| 15:00 | USD | Factory Orders M/M Jan | 0.50% | -0.40% | ||

| 15:30 | USD | Natural Gas Storage | -138B | -129B |

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals