Euro rebounds strongly today on hope of positive development out of negotiation between Ukraine and Russia. Top Russian negotiator Vladimir Medinsky was quoted saying that talks were constructive and a Putin-Zelenskyy meeting is possible. BBC also quoted Russian deputy defence minister Alexander Fomin saying they will “radically reduce” military activity outside Kyiv and Chernihiv. Additionally, the common currency is lifted by rising German 10-year bund yield, which is above 0.7% handle for the first time since 2018. On the other hand, Swiss Franc is sold off broadly on reverse safe-haven flow, followed by Dollar.

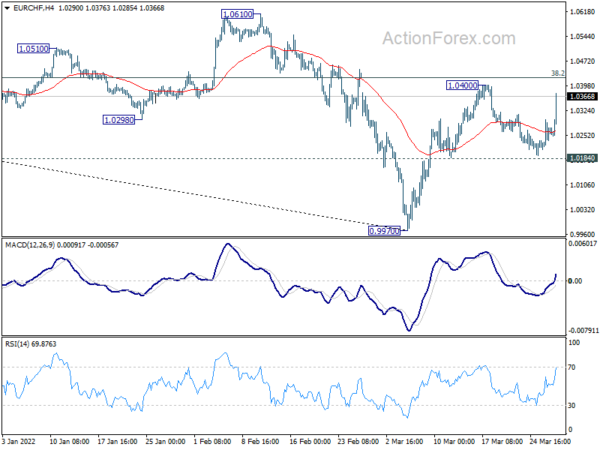

Technically, immediate focus in now on some levels in Euro pairs to confirm the underlying rebound. The levels include 1.1120 resistance in EUR/USD, 0.8456 temporary top in EUR/GBP. More importantly, break of 1.0400 resistance in EUR/CHF will resume the rebound from 0.9970 to 1.0610 key structural resistance. Further break there will be a sign of larger bullish reversal.

In Europe, at the time of writing, FTSE is up 1.33%. DAX is up 2.67%. CAC is up 2.99%. Germany 10-year yield is up 0.118 at 0.700. Earlier in Asia, Nikkei rose 1.10%. Hong Kong HSI rose 1.12%. China Shanghai SSE dropped -0.33%. Singapore Strait Times rose 0.06%. Japan 10-year JGB yield dropped -0.0072 to 0.252.

Germany Gfk consumer sentiment dropped to -15.5, hopes vanished into thin air

Germany Gfk consumer sentiment for April dropped sharply from -8.5 to -15.5. In March, economic expectations dived from 24.1 to -8.9, lowest since May 2020 during the first lockdown at -10.4. Income expectations tumbled from 3.9 to -22.1, hitting the lowest value since 2009, which was at -22.9. Propensity to buy dropped slightly from 1.4 to -2.1.

“In February hopes were still high that consumer sentiment would recover significantly with the foreseeable easing of pandemic-related restrictions. However, the start of the war in Ukraine caused these hopes to vanish into thin air. Rising uncertainty and sanctions against Russia have caused energy prices in particular to skyrocket, putting a noticeable strain on general consumer sentiment,” explains Rolf Bürkl, GfK consumer expert.

Also released, import price index rose 1.3% mom in February, below expectation of 2.1% mom.

BoJ opinions emphasize importance to maintain monetary easing

In the Summary of Opinions of the March 17-18 meeting, BoJ noted, “unlike the United States and the United Kingdom, Japan is not in a situation where the inflation rate will likely exceed the price stability target of 2 percent in a continuous manner.” Hence, “it is important for the Bank to continue with monetary easing to support the economic recovery from the pandemic.”

Situations surrounding Ukraine have “caused price rises of energy and other items”, and this will “push down domestic demand while raising the CPI.” Under these circumstances, it is “necessary to improve labor market conditions and provide stronger support for wage increases”.

One member warned that “if downward pressure on economic activity and prices increases, the economy may instead be in danger of falling into deflation again. If it becomes difficult to achieve the price stability target, the Bank should act nimbly and without hesitation.”

Released from Japan, unemployment rate dropped from 2.8% to 2.7% in February, better than expectation of 2.8%.

Australia retail sales rose 1.8% mom in Feb, hitting second highest on record

Australia retail sales rose 1.8% mom to AUD 33.09B in February, well above expectation of 1.0% mom.

Director of Quarterly Economy Wide Statistics, Ben James, said February’s result saw retail sales reach their second highest level on record after November 2021 and turnover continuing to regain lost momentum caused by the peak of the Omicron outbreak in January.

“Lower COVID-19 case numbers in February, alongside the further easing of restrictions over the month, saw consumer spending return to similar behaviour seen previously as states and territories come out of a COVID-19 wave,” James said.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0954; (P) 1.0977 (R1) 1.1008; More…

EUR/USD rebounds strongly today and immediate focus is now on 1.1120 support turned resistance. Sustained break there will argue that it’s at least correcting the decline from 1.2265. Intraday bias will be back to the upside for 38.2% retracement of 1.2265 to 1.0805 at 1.1363. On the downside, however, break of 1.0943 support will retain near term bearishness, and bring retest of 1.0805 low.

In the bigger picture, the decline from 1.2348 (2021 high) is expected to continue as long as 1.1494 resistance holds. Firm break of 1.0635 (2020 low) will raise the chance of long term down trend resumption and target a retest on 1.0339 (2017 low) next. Nevertheless, break of 1.1494 will maintain medium term neutral outlook, and extending term range trading first.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Unemployment Rate Feb | 2.70% | 2.80% | 2.80% | |

| 23:50 | JPY | BoJ Summary of Opinions | ||||

| 00:30 | AUD | Retail Sales M/M Feb | 1.80% | 1.00% | 1.80% | |

| 06:00 | EUR | Germany Gfk Consumer Confidence Apr | -15.5 | -12 | -8.1 | -8.5 |

| 06:00 | EUR | Germany Import Price Index M/M Feb | 1.30% | 2.10% | 4.30% | |

| 08:30 | GBP | Mortgage Approvals Feb | 71K | 73K | 74K | |

| 08:30 | GBP | M4 Money Supply M/M Feb | 1.00% | 0.50% | 0.10% | |

| 13:00 | USD | S&P/Case-Shiller Home Price Indices Y/Y Jan | 18.40% | 18.60% | ||

| 13:00 | USD | Housing Price Index M/M Jan | 1.40% | 1.20% | ||

| 14:00 | USD | Consumer Confidence Mar | 107.9 | 110.5 |

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals