The latest US employment report will be in the spotlight next week for any signs that recession worries have started to impact hiring. The dollar has lost some of its power lately and this dataset could determine whether we are in the early stages of a trend reversal. Inflation numbers from Europe will be another crucial variable for that equation. Elsewhere, the Bank of Canada is set to raise interest rates.

Hiring freeze

The risk of recession is front and center in financial markets. The US housing market is feeling the heat of rising mortgage rates and investors are running scared that the cost of living crisis is about to infect the labor market, as cooling demand forces businesses to cut back on employment.

There’s evidence that this process has already started. Major corporations such as Amazon, Microsoft, Meta (Facebook), Twitter, Uber, Salesforce, and Nvidia among many others have announced plans to slow down hiring or freeze it. Executives are looking at a slowing economy and are trying to manage costs. Smaller companies are probably struggling more.

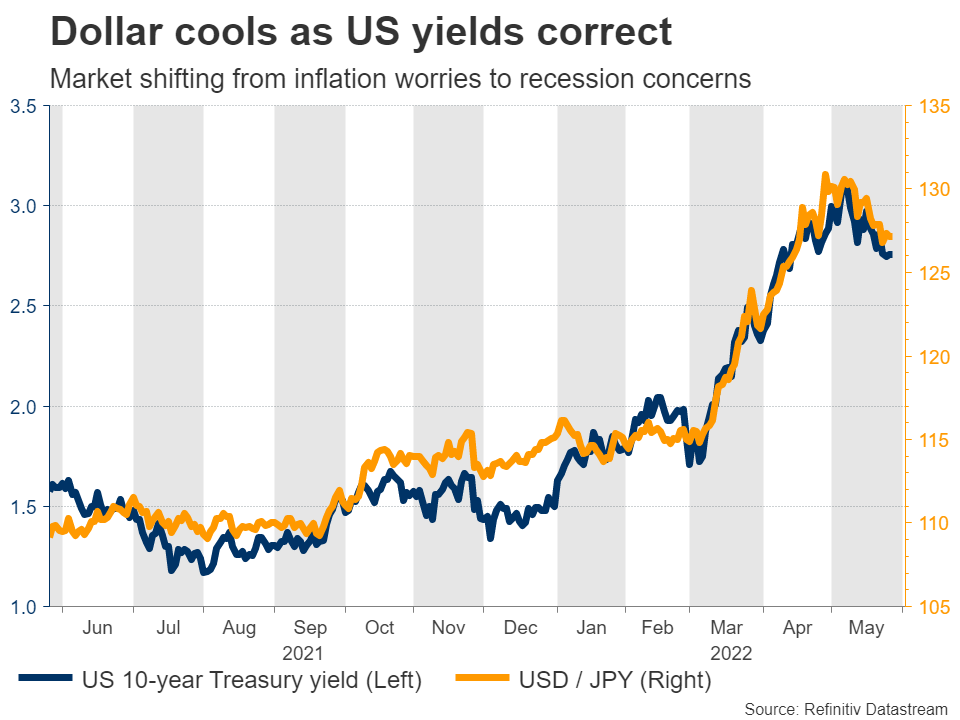

The bond market has started to price in these risks. Worries around rampant inflation have been replaced by worries around an economic slowdown, hammering Treasury yields back down and taking the shine off the dollar. The Fed could even hit the ‘pause’ button on rate increases by September if the economy slows, according to Atlanta Fed president Bostic.

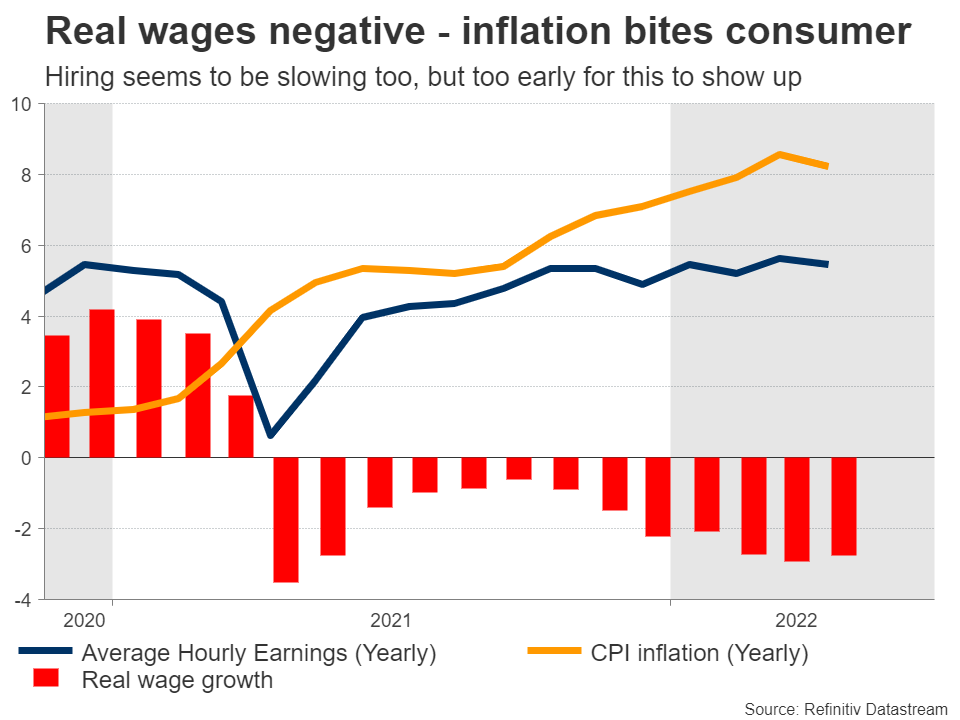

In this light, the upcoming US jobs data on Friday will be crucial for markets. Forecasts point to another solid report overall, with nonfarm payrolls expected at 350k in May and the unemployment rate forecast to drop a little further. Wage growth is expected to remain healthy.

It is probably too early for the hiring slowdown to show up in this dataset, something supported by the S&P Global services PMI, which showed companies raising employment levels at the second-fastest pace in a year. That said, first time seekers of unemployment benefits rose during the month, which is never a good sign.

As for the dollar, there are some signs of trend exhaustion, but it is still difficult to call for a reversal. Yes, euro/dollar rebounded from 1.0340 lately, a region that acted as a reversal point in the past. And with US yields retreating, the dollar no longer enjoys such a tremendous interest rate advantage.

However, the fundamental picture hasn’t changed much. The Fed is still on track to raise rates quickly, the European and Chinese economies are in far worse shape than the American economy, and a global recession would probably send safe-haven flows into the dollar.

There are three fundamental catalysts to watch for a reversal in the dollar – the Fed pauses its hiking cycle, the war in Ukraine ends, or China abandons zero-covid policies. Until then, the reserve currency is unlikely to go out of fashion.

Eurozone inflation getting hotter

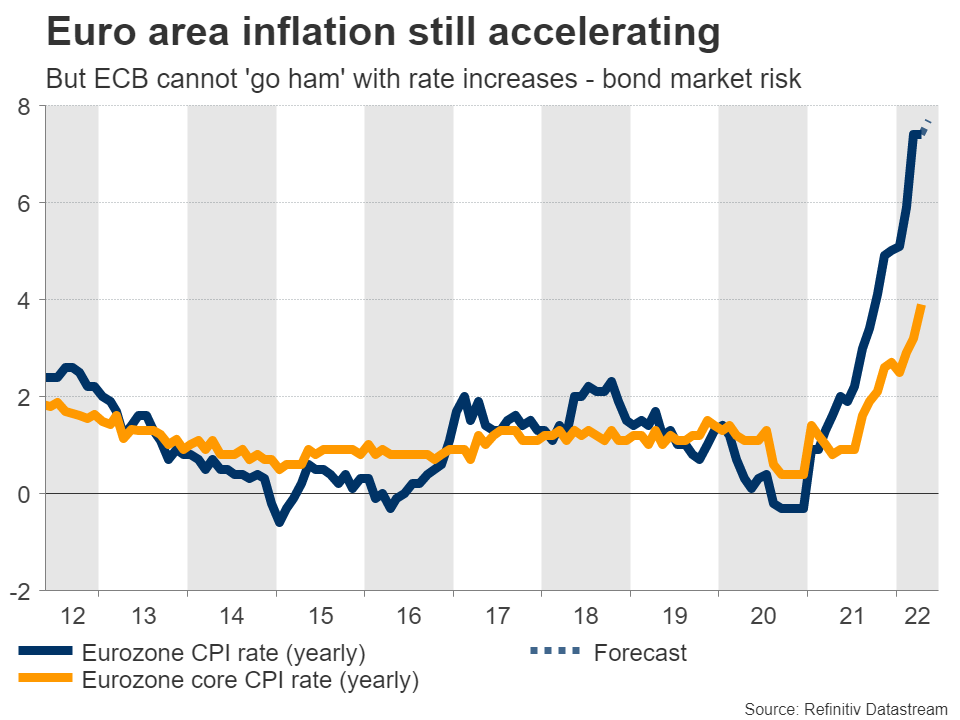

Crossing into the euro area, the latest inflation stats will be released on Tuesday. Forecasts suggest the yearly CPI rate continues to rise, hitting 7.6% in May. That is supported by the composite S&P Global PMI, which showed companies raising their selling prices at the second-sharpest pace on record.

Markets are certain the European Central Bank will raise interest rates in July but there’s a raging debate over how big the rate hike will be. A quarter-point rate hike is fully priced in and traders assign a 40% chance for a bigger, half-point move.

If inflation continues to heat up, that would tip the scales towards the bigger move, allowing the euro to extend its recovery. That said, there are limits to how fast the ECB can go. Raising rates with reckless abandon and stopping asset purchases implies huge risks for bond markets, especially in highly indebted economies like Italy.

Although the euro has bounced back, this looks mostly like a relief bounce from oversold levels. It will probably take something bigger than the ECB raising interest rates for a sustainable rally – possibly one of the three catalysts mentioned above.

BoC to raise rates, China reports PMIs

Over in Canada, the central bank meets on Wednesday and a half-percentage point rate increase (50 bps) is fully priced in. Hence, the market reaction will depend mainly on the signals for future rate hikes and the remarks around the economic outlook.

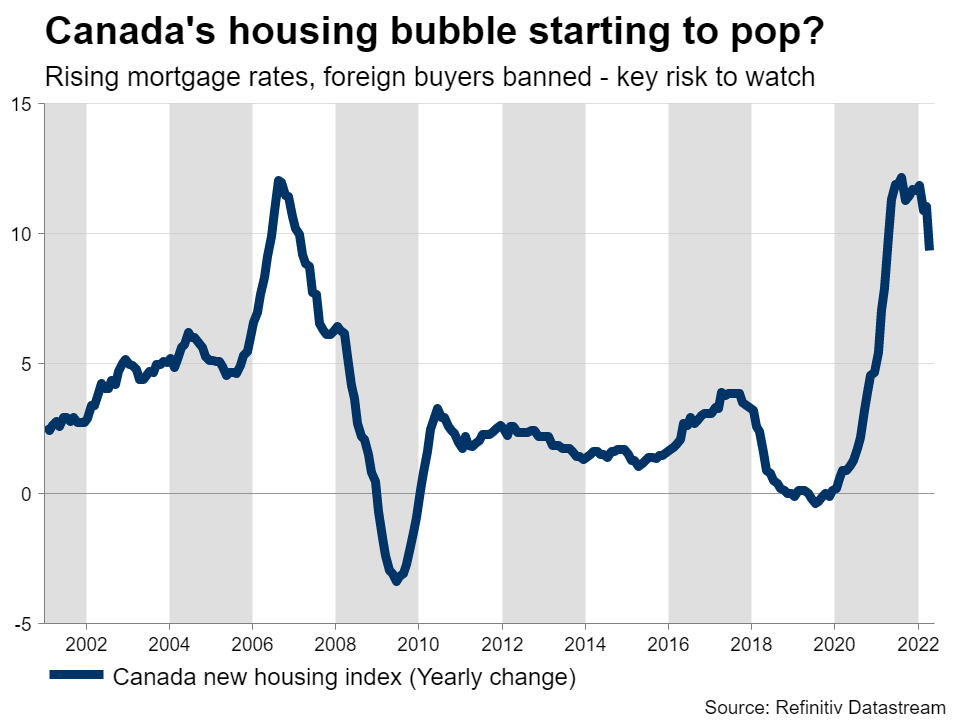

Admittedly, the Canadian economy is solid. Unemployment is at a five-decade low, inflation is sizzling hot, and consumption is healthy. The bad news is the housing market. Canadian house prices rose dramatically in recent years and with mortgage rates now going up so quickly, this ‘bubbly’ sector is in real trouble.

There are already some signs that home prices are dropping and the pain could just be getting started – something that might lead the BoC to be a little cautious, even though the broader economy is still fine.

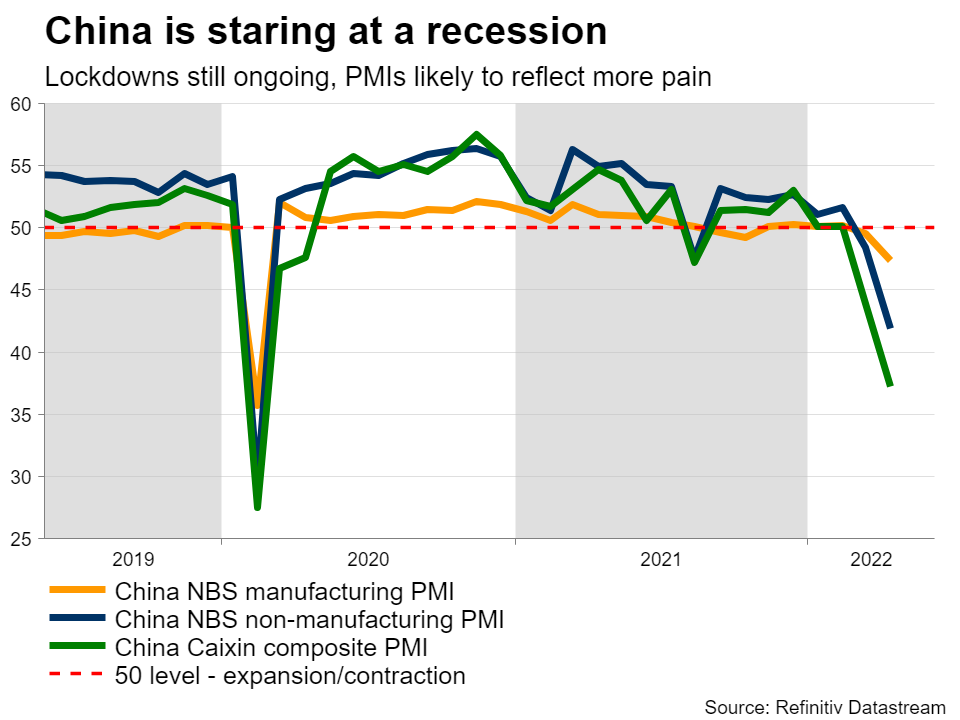

Finally in China, the official PMIs are out on Tuesday and will provide the first look at how the economy performed in May. The lockdowns in major cities continue, so it will probably be another batch of terrible numbers.

A recession looks increasingly likely, and if the upcoming data confirm that, China-sensitive currencies like the Australian dollar could take another hit. Markets are still pricing nine rate increases by the Reserve Bank of Australia this year, so there’s scope for disappointment. The nation’s GDP stats for Q1 are out on Wednesday but considering how much things have changed this quarter, these are likely outdated.

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals