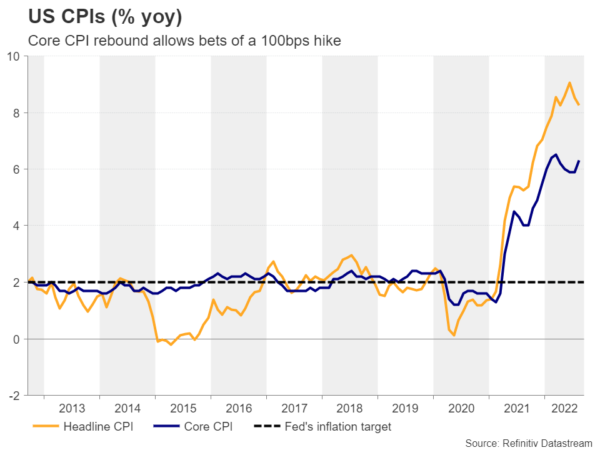

We have a very busy week ahead of us with four central bank meetings on the agenda, but the one to stand out may be the FOMC decision, scheduled on Wednesday at 18:00 GMT. Following last week’s hotter-than-expected CPIs for August, market participants have put on the table a full percentage point hike. But will the Fed really step on the brakes harder this time around, and how will the outcome affect the dollar?

How did investors get to the 100bps bet?

At its latest meeting in July, the FOMC delivered its second consecutive 75pbs hike, but Fed Chair Powell said that it may become appropriate to slow the pace of future increases, painting a picture that stood far from today’s reality. The Committee did not meet in August, but investors had the opportunity to hear again from the Fed chief at the Jackson Hole economic symposium. There, Powell appeared in his hawkish suit, saying that they will raise interest rates as high as needed and keep them there “for some time”. While he acknowledged that this could hurt economic growth as well as labor market conditions, he added that these are the “unfortunate costs of reducing inflation,” and since then, many of his colleagues agreed, with Cleveland Fed President Loretta Mester adding that interest rates should rise to slightly above 4%.

All this encouraged market participants to add to their bets over a more forceful Fed, but the icing on the cake was last week’s hotter-than-expected CPI data, which disappointed those expecting inflationary pressures to ease in the months to come and allowed others to place bets over a full percentage point rate increase at this gathering. According to the Fed funds futures, market participants are now assigning a 20% chance for such an action, with the remaining 80% pointing to a 75bps increase. This may have increased the risk of disappointment and thereby the chances for a setback in the dollar, even in the still very hawkish case of a third 75bps hike.

New ‘dot plot’ to determine the dollar’s faith

Yet, a trend reversal in the dollar’s prevailing uptrend remains very doubtful. Wednesday’s decision will be accompanied by updated economic projections and a new ‘dot plot’. Thus, investors’ choices will largely depend on that as well. Currently, market participants agree that interest rates could rise above 4%, expecting a peak at around 4.4% in March, but they oppose the assessment that they should stay there for some time. They are pricing in a 25bps reduction by September. For that reason, a new plot pointing to a peak near 4.4%, but no cuts for the remainder of the year – in line with many officials’ recent remarks– could add fuel to the dollar’s engines and allow it to claw back any hike-related losses.

Euro/dollar could jump slightly higher in case the Fed hikes by 75bps, but a hawkish narrative and a dot plot pointing to no rate cuts next year could allow the bears to jump back into the action from near the downside line drawn from the high of February 10 or near the 1.0200 zone, marked by the highs of September 12 and 13. The down wave may result in a break below the 0.9860, thereby confirming a lower low and taking the pair into territories last tested in 2002. The next support could be found at 0.9615, marked by the lows of August 6 and September 17 of that year, the break of which could carry extensions towards the inside swing high of September 17, 2001, at around 0.9335.

For the dollar to enter in a defensive mode against its European counterpart, a break above 1.0370 may be needed. Euro/dollar would be already above the aforementioned downside line, while the move would confirm a higher high on the weekly chart. This may encourage the bulls to climb towards the 1.0615 or even the 1.0770 barriers, marked by the highs of June 27 and 9 respectively.

Inflation expectations add to no-cut narrative

The latter scenario appears to be the least likely, as another factor arguing against any rate cuts next year is that inflation expectations indicators, even though they have come off their highs lately, still point to a rate well above the Fed’s objective of 2% in a year’s time. Over and above that, with the Fed adopting an average inflation targeting in 2020, just hitting 2% may not be enough. Officials may opt to hook inflation there for some time, or even push it briefly below target.

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals