Risk appetite seems to be given a lift again by words regarding US-China trade negotiations. There seems to be some consensuses and progress made even thought it’s unsure what they exactly are. Nevertheless, at least, trade talks will resume next week in Washington, which is a positive sign. Yen and Swiss Franc are back under some pressure but Euro is the weakest one for today. Commodity currencies are having a come back too while Dollar is mixed.

Technically, EUR/USD resumed recent fall again by breaking 1.1249 temporary low and is set to challenge 1.1215 low finally. USD/CHF and USD/JPY also rebounds strongly and both could take on 1.0098 and 111.13 resistance. Sterling is showing sign of recovery against Euro and Yen. But GBP/USD remains well below 1.2958 resistance and further decline is expected.

In other markets, FTSE is currently up 0.76%. DAX is up 1.89%. CAC is up 1.80%. German 10-year yield is up 0.0006 at 0.108. Earlier in Asia, Nikkei dropped -1.13%. Hong Kong HSI dropped -1.87%. China Shanghai SSE dropped -1.37%. Singapore Strait Times dropped -0.41%. Japan 10-year JGB yield dropped -0.0114 to -0.022, staying negative.

Release in US session, Empire State Manufacturing index rose to 8.8 in February, up from 3.9 and beat expectation of 7.6. Import price index dropped -0.5% mom in January, below expectation of -0.1% mom. Canada international securities transactions dropped CAD -18.96B in December.

US-China trade talks to continue in Washington next week

The session in Beijing concluded with positive words from both sides, but without much substance. China’s Xinhua news agency said the delegations discussed topics including technology transfers, intellectual property protection, non-tariff barriers, services, agriculture and the trade balance. And it claimed that both countries reached consensus is principle on a number of issues. They’re working towards a memorandum of understanding on trade and economic issues.

US Trade Representative Robert Lighthizer said “we feel we have made headway on very, very important and difficult issues. We have additional work to do but we are hopeful,” Treasury Secretary Steven Mnuchin tweeted “Productive meetings with China’s Vice Premier Liu He and @USTradeRep Amb. Lighthizer”, without any elaboration.

Trade negotiations will resume in Washington next week, as confirmed by White House spokesperson Sarah Sanders. She added that “The United States looks forward to these further talks and hopes to see additional progress.” And, “Both sides will continue working on all outstanding issues in advance of the March 1, 2019, deadline for an increase in the 10 percent tariff on certain imported Chinese goods.”

Ifo: German car exports to US could be halved on new tariffs, but EU could have clever counterstrategy

The US Commerce Department is set to deliver its recommendation to the White House regarding auto tariffs, meeting a deadline on Sunday. Ahead of that German Ifo institute warned that if US imposes 25% additional, permanent tariffs on cars, that could reduce German car experts to the US by 50% in the long run.

For Germany, according to Gabriel Felbermayr, director of the ifo Center for International Economics, total car exports could drop by -7.7%, or EUR 18.4B. But, exports from other sectors and to other countries could “slightly cushion” the overall loss. But the net result could still be EUR 11.6B loss of exports.

Felbermayr adds: “The EU can, however, develop a clever counterstrategy that would bring the effects of US tariffs on the economic performance of both sides to roughly zero. That would be tariffs on US products whose manufacturers would have to react with price reductions. This, in turn, would harm third countries whose economic output could fall by about five billion euros.” All calculations assume adjustment reactions, 90 percent of which take place within five years.

UK Leadsom: No-deal Brexit is on the table, it’s the legal default position

UK government’s leader in the House of Commons Andrea Leadsom said the government does not want no-deal Brexit. But it’s there because that is the “legal default position”. And “essentially that is what will happen if we don’t vote for a deal.” She also noted that “What the government is seeking to do is to sort out the arrangements on the backstop so that parliament can vote for the deal. That is the government’s sole focus.”

Meanwhile, Leadsom also urged EU to compromise on the Irish border backstop. She said “If the EU were to bring on the one thing that they have said they are determined to avoid, that is the risk of the UK leaving the EU without a deal at the end of March and thereby having to have some kind of hard border between Northern Ireland and Ireland. So it simply would not make sense to precipitate such a conundrum when the option of a negotiated arrangement, where the UK could put in place alternative arrangements for the backstop, would be far preferable from everybody’s point of view including from the perspective of the issue of the border between Northern Ireland and Ireland.”

UK Jan retail sales blew expectations, but store price slowed to lowest since 2016

UK January retail sales came in much stronger than expected. Including auto and fuel, sales rose 1.0% mom, 4.2% yoy versus expectation of 0.2% mom, 3.4% yoy. Excluding auto and fuel, sales rose 1.2% mom, 4.1% yoy versus expectation of 0.2% mom, 3.1% yoy. However, year-on-year average store prices growth slowed to 0.4%, lowest price increase since November 2016.

Also released in European session, Eurozone trade surplus narrowed to EUR 15.6B in December, below expectation of EUR 16.4B.

RBA Kent: Markets expect next RBA move to be down than up

RBA Assistance Governor Christopher Kent delivered a speech on “Financial Conditions and the Australian Dollar – Recent Developments” today. There he acknowledged that developments in Australian financial markets have been similar to those offshore, with falling equity prices, rising credit spreads and increased volatility. Such development is “a story of risk premia increasing from low levels and were associated with rising concerns about downside risks, both internationally and domestically.”

The outlook for domestic economy has “also shifted” with downward revision in both growth and inflation forecasts. And market expectations for the next move in cash rate have “switched signs too”. Kent noted that “markets have assessed that the next move is more likely to be down than up.”. And that’s reflected in lower bond yields.

Fall in Australian bond yields is “likely to have contributed somewhat to the modest depreciation of the Australian Dollar of late”. On the other hand, “higher commodity prices appear to have worked to limit the extent of Australian dollar depreciation”.

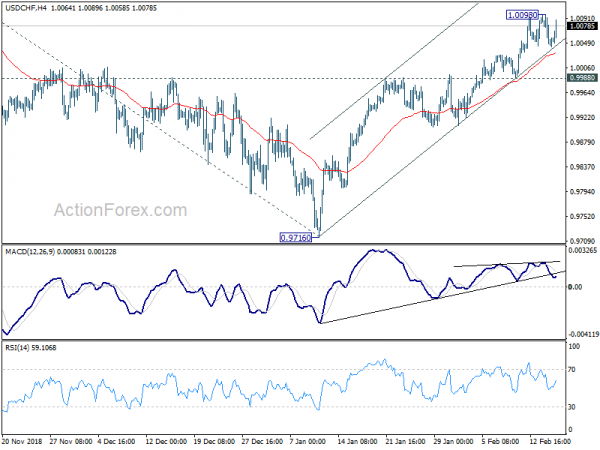

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 1.0030; (P) 1.0064; (R1) 1.0085; More….

USD/CHF rebounds strongly in early US session but stays below 1.0098 temporary top. Intraday bias remains neutral first. In any case, further rally is expected as long as 0.9988 support holds. On the upside, above 1.0098 will target 1.0128 first. Break will confirm resumption of up trend from 0.9186. Next target will be 100% projection of 0.9541 to 1.0128 from 0.9716 at 1.0303. However, break of 0.9988 will indicate rejection by 1.0128 and turn intraday bias to the downside for 0.9716 support again.

In the bigger picture, USD/CHF drew strong support from medium term trend line and rebounded. That suggests rise from 0.9186 is still in progress. Further break of 1.0128 will confirm up trend resumption and target 1.0342 key resistance. Nevertheless, break of 0.9716 will dampen this bullish view and at least bring deeper fall to 0.9541 key support.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | NZD | BusinessNZ Manufacturing PMI Jan | 53.1 | 55.1 | 54.8 | |

| 01:30 | CNY | CPI Y/Y Jan | 1.70% | 1.90% | ||

| 01:30 | CNY | PPI Y/Y Jan | 0.10% | 0.90% | ||

| 04:30 | JPY | Industrial Production M/M Dec F | -0.10% | -0.10% | -0.10% | |

| 09:30 | GBP | Retail Sales Ex Auto Fuel M/M Jan | 1.20% | 0.20% | -1.30% | -1.00% |

| 09:30 | GBP | Retail Sales Ex Auto Fuel Y/Y Jan | 4.10% | 3.10% | 2.60% | 2.90% |

| 09:30 | GBP | Retail Sales Inc Auto Fuel M/M Jan | 1.00% | 0.20% | -0.90% | -0.70% |

| 09:30 | GBP | Retail Sales Inc Auto Fuel Y/Y Jan | 4.20% | 3.40% | 3.00% | 3.10% |

| 10:00 | EUR | Eurozone Trade Balance (EUR) Dec | 15.6B | 16.4B | 15.1B | 15.8B |

| 13:30 | CAD | International Securities Transactions (CAD) Dec | -18.96B | 9.45B | 10.24B | |

| 13:30 | USD | Empire State Manufacturing Feb | 8.8 | 7.6 | 3.9 | |

| 13:30 | USD | Import Price Index M/M Jan | -0.50% | -0.10% | -1.00% | |

| 14:15 | USD | Industrial Production M/M Jan | 0.10% | 0.30% | ||

| 14:15 | USD | Capacity Utilization Jan | 78.70% | 78.70% | ||

| 15:00 | USD | U. of Mich. Sentiment Feb P | 93.9 | 91.2 | ||

| 21:00 | USD | Net Long-term TIC Flows Dec | 37.6B |

For traders: our Portfolio of forex robots for automated trading has low risk and stable profit. You can try to test results of our download forex ea

Signal2forex review

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals