U.S. Review

Throw Out the Textbook

- Oil prices went negative for the first time in history on Monday as the evaporation of demand collided with a supply glut.

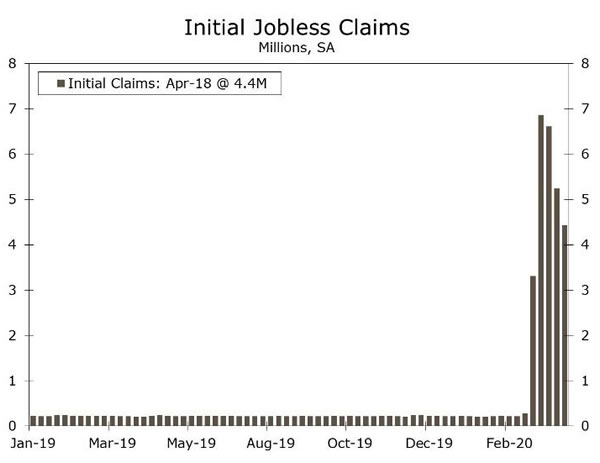

- In the past five weeks, 26.5 million people have filed for unemployment insurance, or more than one out of every seven workers.

- Congress has passed its fourth major relief package, including an additional $320 billion for the PPP.

- The Fed continues to do what it can, with its balance sheet rising an astounding $2.4 trillion in just two months.

Throw Out the Textbook

The economic ramifications of COVID-19, as well as the size and scope of the policy response, continued to rewrite the textbook this week. Oil prices went negative for the first time in history on Monday as the evaporation of demand collided with supply that literally can’t be shut off quickly enough. Specifically, the expiring front-month WTI contract price fell below zero, as holders of the security squirmed to avoid having to take physical delivery with oil storage space scarce and expensive. Yet it would be a mistake to write this collapse off as merely the result of technical factors, or the over-financialization of commodities markets. The evaporation of demand is very real—TSA screenings are running -95% yearover- year, as just one example—and the plunging price of the world’s most economically important natural resource is surely telling us something. If there was any doubt, further out contracts also plunged in price this week, to levels well below breakevens for most domestic producers (For more on oil, see Topic of the Week).

Meanwhile, the depth and duration of the hit to demand becomes clearer by the day. In the past five weeks, 26.5 million people have filed for unemployment insurance, or more than one out of every seven workers. The flow of workers into employment has slowed for three straight weeks, but that is unsurprising and not insightful—entire sectors of the economy were forced to shut down at once; that obviously can’t repeat. We are instead focusing on the cumulative number of layoffs and are watching to see how broadly the labor market collapse spreads beyond the most directly affected industries of leisure & hospitality and retail. We will also be watching the eventual flow out of unemployment—people dropping off of continuing claims—to get a sense of employers’ willingness and ability to get their operations back up and running in coming months. The good news is that the augmented unemployment benefits under the CARES Act should be helping the 16.0 million—and counting—people already receiving unemployment benefits the week ended April 11. There’s also the hope that many of these workers will be rehired to meet the conditions of PPP loan forgiveness.

Recognizing the strong demand for PPP loans, Congress has passed its fourth major relief package, including an additional $320 billion for the PPP, $75 billion for hospitals and $25 billion for COVID-19 testing. Reports suggest demand for loans remains voracious, and Congress will likely have to return to the negotiating table again. Assistance to state and local governments was noticeably absent from this package and increasingly appears to be a political sticking point. The Fed continues to do what it can, with its balance sheet rising an astounding $2.4 trillion in just two months to $6.6 trillion.

Capital spending plans clearly took a hit in March, with durable goods orders falling 14.4%. The weakness was centered in transportation, but core capital goods orders, which fared surprisingly well, will fall markedly in coming months. Residential real estate transactions were also smothered by stay-at-home orders, as existing and new home sales fell by 8.5% and 15.4%, respectively. Both should fall even more sharply in April.

U.S. Outlook

First Quarter GDP • Wednesday

The U.S. economy came to a grinding halt in March as workers were sent home and asked to stay there as the nation battled COVID-19. Prior to the domestic outbreak, economic activity was fairly strong at the start of the year. But the suspension of activity in March was so abrupt and far-reaching that we think it was enough to pull first quarter growth negative. There is no corner of the economy that is sheltered from this public health crisis. Personal consumption expenditures will likely be modestly negative in Q1 as consumers began to withdraw themselves from the economy. Business investment spending will be weak, as businesses likely grew cautious and began to pare back spending even before lockdowns were officially put in place. Residential investment may be one of the only sources of strength in Q1, but any momentum likely dried up by quarter-end. In many ways market participants are already looking ahead as the bulk of the COVID-19 hit is expected in Q2.

Previous: 2.1% Wells Fargo: -1.2% Consensus: -3.7% (Quarter-over-Quarter, Annualized)

Personal Income & Spending • Thursday

All indications point to an awful March personal income & spending report. Income should be pretty bleak, with transfer payments likely the only component to see a significant rise, as millions of Americans began filing for unemployment insurance in late March.

Weak income growth coupled with people being confined to their homes is a nasty backdrop for consumption. March was the worst month on record for many retailers, which suggests spending on goods plummeted, with outsized gains at grocery stores washed by massive declines for autos and clothing. High frequency data also suggest steep declines in services outlays. Outside of your rent/mortgage, utilities, internet or a take-out meal, have you made a service outlay in the past 30 days? This is daunting. As activity has stalled, areas of the economy which are typically quite resilient (services) are getting squeezed. There is hope, however, for a sizeable consumption rebound once the economy ‘re-opens’.

Previous: 0.6%; 0.2% Wells Fargo: -4.4%; -6.9% Consensus: -1.5%; -5.0% (Month-over-Month, Inc; Spend)

ISM Manufacturing Index • Friday

Weak demand and safety precautions have caused factories to shutter in the wake of COVID-19. Next week’s report is for April, the first full month that stay-at-home orders have been in place. In March the ISM manufacturing index fell to 49.1, an indication of only a modest contraction in activity. But the new orders component—an indication of future activity—declined to 42.2 in March, the fastest pace of contraction in bookings since 2009.

We expect the ISM index to fall further to 38.7 in April. Regional Fed Purchasing Managers Indices suggest a pronounced drop-off in activity. The New York Fed’s Empire Manufacturing index fell to -78.2 in April, while the comparable measure from the Philly Fed’s survey hit -56.6. These two regional surveys alone suggest an ISM print less than 35. The Kansas City Fed’s survey also hit a record low of -30 in April. Expect manufacturing activity to remain bleak until business confidence is restored and economic activity resurfaces.

Previous: 49.1 Wells Fargo: 39.7 Consensus: 36.7

Global Review

Eurozone and U.K. PMIs Paint an Ugly Picture

- This week we received a bit more insight into how COVID-19 is impacting major economies around the world. The Eurozone April manufacturing and services PMIs fell to record lows, which could indicate a sharper Eurozone contraction this year than originally anticipated.

- Similar dynamics took place in the U.K. as well, as the April manufacturing and services PMIs fell deeper into contraction territory. As of now, we expect a recession in the UK economy in 2020, and while the Bank of England and U.K. government have moved forward with stimulus measures, we do not believe it will be enough to avoid an annual GDP contraction.

Eurozone and U.K. PMIs Sink Deeper

On Thursday morning, the outlook for the Eurozone darkened a bit more as April PMI data were released. While the outlook for the Eurozone has turned sharply negative amid the COVID-19 outbreak, the April PMI data suggest the economy could be in much worse shape than originally anticipated. The manufacturing PMI, which had already hit a low in March, fell to yet another new low, dropping to 33.6, below the consensus forecast of 38.0. As underwhelming as the manufacturing PMI was, the services PMI was especially concerning, falling to 11.7, a new record low as well, and also lower than consensus estimates of 22.8. For years, the Eurozone consumer had been supporting the Eurozone economy; however, given the lockdown measures implemented across the region, it seems as if the consumer may not be in a position to provide ample support to the economy. In response to the broad slowdown, the European Central Bank (ECB) has taken action to support the economy, including extending its asset purchase program, and just recently, opting to receive non-investment grade bonds as collateral in its liquidity operations. The next key data for the Eurozone will be Q1 GDP, set to be released next week. We forecast a contraction in Q1, and as of now, expect the Eurozone economy to contract 5.5% for the full-year 2020.

April PMI data in the United Kingdom were released Thursday morning as well and were also underwhelming relative to consensus forecasts. The manufacturing PMI fell to 32.9 in April, down from 47.8 in March, and much lower than consensus forecasts of 42.0. The decline pushed it further into contraction territory, where it has now been for two consecutive months. Similar to the Eurozone, the April services PMI fell significantly, dropping to a record low of 12.3, much lower than the March survey of 34.5 and below the consensus forecast of 27.8. While Q1 GDP will not be released until mid-May, the PMI data suggest the U.K. economy will likely also contract over the first three months of the year. In an effort to offset the economic impact of COVID-19, the Bank of England (BoE) has taken numerous monetary policy measures, including reducing its main policy rate 65 bps to 0.10% and restarting a quantitative easing program with an extra £200B in asset purchases. In addition, the U.K. government announced a large fiscal stimulus program worth around 3% of GDP that includes tax cuts, subsidies and cash payments for citizens who have lost their job. While the monetary easing and fiscal stimulus programs should cushion the economic impact, we forecast the U.K. economy will fall into recession this year.

Ultimately, we think the U.K. will contract around 5% for the fullyear, with the largest contraction coming in Q2 as lockdown measures remain in place for the next few months. In addition, we expect inflationary pressures to subside as consumer activity slows and oil prices remain low for an extended period of time. As of our latest forecasts, we expect annual inflation to slow to 0.5%, which is a notable slowdown from close to 2.0% last year.

Global Outlook

China Manufacturing PMI • Wednesday

Chinese PMI data for the month of April will be released next week, and should provide insight into how China’s recovery is progressing. A few weeks ago, Q1 GDP data were released, with the takeaway being that the Chinese economy experienced a significant growth shock over the first few months of the year. China’s economy contracted 9.8% on a sequential basis, and 6.8% year-over-year. Heading into the second quarter, however, Chinese authorities have started to open up the economy, which means it should begin to recover. Reports of manufacturing plants operating again should support growth in the second quarter and also help keep the manufacturing PMI in expansionary territory for the time being. Following a significant decline earlier in the year, the manufacturing PMI jumped back to 52.0 in March; and given the worst of the outbreak is likely over for China, we expect the manufacturing PMI to stay in expansion in April as well.

Previous: 52.0 Consensus: 51.0

Eurozone GDP • Thursday

Activity and sentiment data across the Eurozone have nosedived over the past few months as COVID-19 spread across many countries in the region. Both the manufacturing and services PMIs declined significantly in March, while other activity data such as car registrations softened notably as well. With lockdowns and social distancing measures in place in Italy, Germany, France and Spain, it is likely that the Eurozone experienced a sharp contraction in Q1. As of now, consensus forecasts suggest the Eurozone contracted 3.5% q/q, while we expect the contraction to be a bit less severe and forecast a 2.0% q/q decline. We also forecast the Eurozone economy to fall into recession this year and contract around 5.5% on a full year basis in 2020. While the ECB has taken measures to support the economy and multiple governments within the Eurozone have implemented fiscal stimulus, we ultimately do not think it will be enough to avoid an annual GDP contraction.

Previous: 0.1% Wells Fargo: -2.0% Consensus: -3.5% (Quarter-over-Quarter)

Canada Manufacturing PMI • Friday

The Canadian economy is likely to come under significant stress over the course of 2020 as it deals with its own lockdown protocol as well as lower oil prices and a pending U.S. recession. Oil prices are down around 70% this year as demand has cratered amid the fallout from COVID-19 and the impact of tensions between Saudi Arabia and Russia are still being felt in oil markets despite a recent deal to cut production. In addition, strong trade linkages between the U.S. and Canada should place added pressure on the domestic economy. While we will not get Q1 GDP data for a little while, we expect a significant contraction indicating the start of a recession as well as an annual contraction in Canada. Looking past Q1, next week’s manufacturing PMI should give more insight into how the Canadian economy will be impacted into Q2. As of now, the manufacturing PMI is in contraction territory, and given the further collapse in oil prices this month, we expect another decline in April.

Previous: 46.1

Point of View

Interest Rate Watch

Upcoming FOMC Meeting

After a swift rollout of previously used and brand new policy tools, the Federal Reserve has never in its 107 year history had the expansive toolkit it has at its disposal today. The next Federal Open Market Committee (FOMC) meeting will conclude this coming Wednesday April 29.

Former Minneapolis Fed President Kocherlakota suggested this week that the FOMC may steer rates into negative territory. Although there are no zeroprobabilities in today’s world, we believe it is highly unlikely the FOMC will venture into the land of negative interest rates or yield curve control. Not only have the results been mixed in the economies where it’s been adopted, but also money market funds play an important role in the U.S. financial system, so this policy could have more adverse effects in the United States than in other major economies.

The Fed has been very active with QE thus far in the crisis. At its peak in late March, the Fed was purchasing $75 billion in Treasury securities per day, a stunningly large sum. As Treasury yields have declined and liquidity in the market has improved, the Fed has steadily tapered its purchases to roughly $15 billion per day at present. We expect this tapering to continue, and for the Fed to purchase at least another $500 billion in Treasury securities by quarter-end. Purchases thus far have already totaled an astounding $2.4 over the past two months.

The Fed’s support to state and local governments through various liquidity facilities should help states with their cash flow until July 15, the new tax filing deadline in the wake of the CARES Act. Additional clarification about those plans could be in store next week.

We expect the FOMC will increase the Interest Rate on Excess Reserves (IOER) 5 bps to 0.15%. The last IOER tweak came at the end of January, when the spread of the effective fed funds rate over the lower bound was close to where it is today. Yes, it will be a strange message to be increasing a policy rate given all the other things it is doing to ease conditions, but, in our view, the FOMC has been successful in separating “tweaks” to IOER from its broader policy message.

Credit Market Insights

Argentina Debt Plan Rejected

A group of major Argentine bondholders have rejected the government’s proposal aimed at restructuring $66.2 billion of its foreign-law bonds as part of an effort to support the budget and kick start growth. In our opinion, the rejection of the offer was not surprising as we expected bondholders to show resistance given the terms of the proposal. The restructuring proposal outlined late last week called for a 62% haircut on interest payments, a threeyear grace period on foreign-debt payments and a 5% cut in the value of the principal.

The group, which holds more than 25% of Argentina’s bonds issued after 2016 and over 15% of exchange bonds issued during the last restructuring, said the government’s proposal seeks “to place a disproportionate share of Argentina’s longer-term adjustment efforts on the shoulders of international bondholders.” Bondholders also expressed their skepticism of any cash flows set far into the future, due to the country’s history of restructuring. Although the offer was denied, the government gave bondholders 20 days to review and negotiate a new deal to restore debt sustainability.

Argentina currently faces around $500 million in debt payments in April, which if the government misses, has a 30-day grace period before entering default. That said, although the country’s bonds under foreign and local law are not under hard default to date, a debt default is highly likely given the economy is currently in recession and it is unlikely the government will be able to rollover its debt.

Topic of the Week

It’s Hard to Be Positive When Oil is Negative

The decline in oil prices has been astonishing. For perspective, WTI started off the year around $60/barrel, and was $66 this time last year. The precipitous decline in prices is the result of a significant imbalance in global energy markets. Worldwide efforts to contain COVID-19 have resulted in a near evaporation of global energy demand, while heated negotiations earlier in the year between Saudi Arabia and Russia led to an increase in OPEC production and left a massive oversupply of oil. More recently, OPEC and other global producers have come to an agreement to scale back production, but that will take some time to filter through to prices, and even then, oil is likely to remain in oversupply until global growth picks up.

What’s more, these recent developments have occurred against a backdrop of weakening oil and gas sector capital spending. Over the past few years, the dramatic rise in oil production in places such as Texas and North Dakota has put immense pressure on existing energy infrastructure, and build-out of pipeline and takeaway capacity has lagged the upshift in production. This had brought prices lower and prompted many operators to cut back capital expenditures—in fact, the rig count had already dropped 25% last year. Even with the pullback, production has continued in many shale plays, as prices were still hovering at a level which would allow many operators to remain profitable.

Fast forward to the past few weeks. With shrinking energy demand and production still rising, operators have simply run out of physical storage capacity. Furthermore, prices have fallen well below levels needed to cover operating costs, which means production in many areas will be suspended and capital spending budgets will be slashed further. Given these supply constraints and the dimming prospects for a rebound in global energy demand, the sector is in for a prolonged period of pain, with a wave of bankruptcies and consolidations expected.

Normally, lower oil prices might be a tailwind for consumer spending and offset declines in oil and gas investment. However, these are not normal times, and it is unlikely lower energy prices will provide much relief given widespread stay-at-home orders.

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals