Selloff in commodity currencies intensifies today as risk sentiment turn sour again. Major European indexes are all in deep red while US futures point to lower open. Yen, Swiss Franc and Dollar are taking turns to be the strongest one in a three-horse race. Aussie is so far the worst performing, followed by Loonie and Kiwi. But there is not much difference between the three. Euro and Sterling are mixed for now, stuck in the middle. WTI crude oil also dives below 64k handle, but Gold is resilient at around 1780.

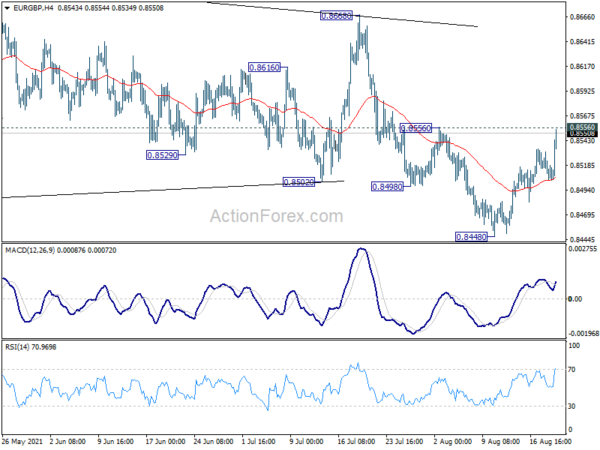

Technically, we’ll pay attention to development in EUR/GBP for the rest of the session. Firm break of 0.8556 support will suggest that fall form 0.8668 is over, and bring retest of this resistance. That could also be a prelude to larger bullish reversal. If that happens we’d also likely see GBP/USD drops further to 1.3570 support GBP/JPY would also follow and drop to 148.43 support. There are where the key support level for the Pound to defend.

In Europe, at the time of writing, FTSE is down -1.94%. DAX is down -1.96%. CAC is down -2.65%. Germany 10-year yield is down -0.002 at -0.481. Earlier in Asia, Nikkei dropped -1.10%. Hong Kong HSI dropped -2.13%. China Shanghai SSE dropped -0.57%. Singapore Strait Times dropped -1.42%. Japan 10-year JGB yield dropped -0.0003 to 0.017.

US initial jobless claims dropped to 348k, continuing claims at 2.82m

US initial jobless claims dropped -29k to 348k in the week ending August 14, better than expectation of 362k. That’s also the lowest level since March 14, 2020. Four-week moving average of initial claims dropped -19k to 378k, lowest since March 14, 2020 too.

Continuing claims dropped -79k to 2820 in the week ending August 7, lowest since march 14, 2020. Four-week moving average of continuing claims dropped -111k to 2999k, lowest since March 21, 2020.

Philly Fed manufacturing dropped to 19.4, but remained elevated

In the August Philadelphia Fed Manufacturing Business Outlook Survey diffusion index for currency activity dropped to 19.4 in August, down from 21.9, below expectation of 24.3. It’s also the fourth consecutive decline. 28% of the firms reported increases in current activity while 9% reported decreases.

Philadelphia Fed said: “Responses to the August Manufacturing Business Outlook Survey suggest continued expansion for the region’s manufacturing sector. The indicators for current activity and shipments decreased from last month but remained elevated. Additionally, the firms reported increases in new orders and employment. The survey’s future indexes moderated this month but continue to suggest expected growth over the next six months.”

ECB Lane explains three conditions for rate hike

ECB Chief Economist Philip Lane explained a a blog post the three key conditions for lifting interest rates, as reflected in the latest forward guidance.

The first condition “until we see inflation reaching two per cent well ahead of the end of our projection horizon” provides reassurance that the convergence of inflation towards the new target should be sufficiently advanced and mature at the time of policy rate lift off. It helps to “hedge monetary policy against the risk of reacting to forecast errors”.

The second condition expects inflation to stay at 2% “durably for the rest of the projection horizon”. It “telegraphs that reaching the inflation target should be lasting.”

The third condition “progress in underlying inflation is sufficiently advanced to be consistent with inflation stabilising at two per cent over the medium term” signals that policy rates should not be lifted unless underlying inflation is also judged to have made satisfactory progress towards the target.

Lane further explained that “underlying inflation” is a broad concept and refers to the persistent component of inflation that filters out short-lived, reversible movements in the inflation rate and provides the best guide to the medium-term inflation developments

Also, the sentence that the forward guidance “may also imply a transitory period in which inflation is moderately above target” makes explicit that rate forward guidance that is committed to avoiding premature tightening.

Released in European session, Swiss trade surplus narrowed slightly to CHF 5.25B in July, above expectation of EUR 4.78B. Eurozone current account surplus rose to EUR 21.8B in Jun, above expectation of 12.3B.

Australia unemployment rate dropped to 4.6%, people falling out of the labour force

Australia employment grew 2.2k in July, better than expectation of -45.0k contraction. Full-time jobs dropped -4.2k while part-time jobs rose 6.4k. Unemployment rate dropped -0.3% to 4.6%, which was already -0.6% lower than than 5.1% level at the start of the pandemic in March 2020. However, participation rate dropped by -0.2% to 66.0% at the same time.

Bjorn Jarvis, head of labour statistics at the ABS, said: “Early in the pandemic we saw large falls in participation, which we have again seen in recent lockdowns. Beyond people losing their jobs, we have also seen unemployed people drop out of the labour force,”

“In Victoria, we saw unemployment fall by 19,000 people in July 2020, during the second wave lockdown, and by 13,000 in the June 2021 lockdown. The fall in unemployment in New South Wales in July 2021 was more pronounced than either of these, falling by 27,000 people.”

“In each of these instances, the unemployment rate also fell. Falls in unemployment and the unemployment rate may be counter-intuitive, given they have coincided with falls in employment and hours, but reflect the limited ability for people to actively look for work and be available for work during lockdowns. This means that people are falling out of the labour force.”

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3727; (P) 1.3757; (R1) 1.3786; More…

GBP/USD’s fall continues to as low as 1.3673 so far and intraday bias stays on the downside for 1.3570 support. Break there will resume the fall form 1.4248 to 1.3482 resistance turned support. Firm break there will carry larger bearish implication and target 38.2% retracement of 1.1409 to 1.4248 at 1.3164. On the upside, above 1.3785 minor resistance will mix up the near term outlook and turn intraday bias neutral first.

In the bigger picture, as long as 1.3482 resistance turned support holds, up trend from 1.1409 should still continue. Decisive break of 1.4376 resistance will carry larger bullish implications. However, firm break of 1.3482 will argue that the rise from 1.1409 has completed. GBP/USD would then be seen as in another leg of long term range pattern between 1.1409 and 1.4376. Deeper fall could then be seen to 61.8% retracement of 1.1409 to 1.4248 at 1.2493, and even below.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:30 | AUD | Employment Change Jul | 2.2K | -45.0K | 29.1K | |

| 01:30 | AUD | Unemployment Rate Jul | 4.60% | 5.00% | 4.90% | |

| 06:00 | CHF | Trade Balance (CHF) Jul | 5.25B | 4.78B | 5.53B | 5.47B |

| 08:00 | EUR | Eurozone Current Account (EUR) Jun | 21.8B | 12.3B | 11.7B | 13.9B |

| 12:30 | CAD | ADP Employment Change Jul | 221.3K | -294.2K | ||

| 12:30 | USD | Initial Jobless Claims (Aug 13) | 348K | 362K | 375K | 377K |

| 12:30 | USD | Philadelphia Fed Manufacturing Aug | 19.4 | 24.3 | 21.9 | |

| 14:30 | USD | Natural Gas Storage | 28B | 49B |

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals