Here are the latest developments in global markets:

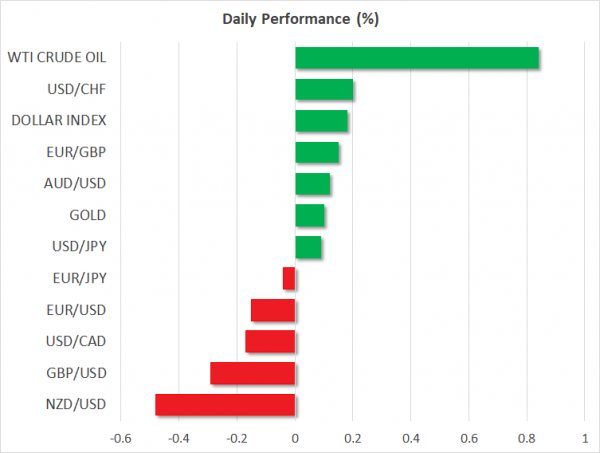

FOREX: Dollar/yen managed to recover earlier losses to climb back to 110.14 (+0.08%) as a US official messaged on Wednesday that Washington will not use stricter trade frictions against China but monitor Chinese investments through an existing national security review system. The dollar index also advanced to touch 94.79 (+0.14%), while investors were preparing their positions ahead of the durable goods orders later in the day and preliminary PCE inflation numbers on Friday. On the other hand, the euro was heading downwards as trade risks and political conditions in Germany continued to hang in the background. Euro/dollar moved lower to 1.1626 (-0.15%) before the EU summit kicks off on Thursday although Italy’s eurosceptic Senate, Alberto Bagnai said today that the government will not act against the euro. Pound/dollar remained in the negative ground, dropping below the 1.3200 handle (-0.10%) after the BOE Governor Carney highlighted risks from Brexit at his financial stability review presentation. He also argued that rising trade uncertainties could pull world interest rates back. Dollar/loonie was slightly up at 1.3310. Aussie/dollar held below its opening level around 0.7386 (-0.14%), while kiwi/dollar declined to 0.6820 (-0.61%) ahead of the RBNZ policy meeting overnight

STOCKS: European equities were in the green at 1200 GMT, with the pan-European STOXX 600 and the blue-chip Euro STOXX 50 rising by 0.54% and by 0.65% repsectively. The German DAX 30 jumped by 0.97%, the French CAC 40 gained 0.74%%, while the Italian FTSE MIB moved up 0.66%. The UK’s FTSE 100 advanced by 0.81%. In Asia, equity markets closed in the negative territory with the exception of the Japanese Topix, while in the US, futures tracking the major stock indices were pointing to a positive open.

COMMODITIES: Oil prices had a significant winning day after yesterday’s API readings printed a much bigger inventory drawdown than analysts expected. Concerns over US sanctions on Iran were also supporting the market today. .West Texas Intermediate (WTI) oil surpassed $71 per barrel, posting a new one-month high and adding 0.78% to its daily performance. London-based Brent crude climbed by 0.48% to $76.68 per barrel. In precious metals, gold retreated by 0.21% to $1,257.43 per ounce, hitting a fresh six-month low of $1,253 early today.

Day ahead: US durable goods attract attention; RBNZ to hold rates steady but eyes on outlook

Durable goods orders and pending home sales out of the US will highlight the economic calendar later on Wednesday, while trade developments will continue to be closely monitored, with investors waiting eagerly to see whether the US will soften its protectionist stance against China.

At 1230 GMT, the US Census Bureau is expected to say that US durable goods orders have dropped by 1.0% m/m in May, by less than the 1.6% fall in the previous month, while in the absence of transport products the gauge is projected to record a growth of 0.5% m/m compared to 0.9% expansion in April. The non-defense core measure which excludes aircraft is also expected to slow down, easing from 1.0% m/m to 0.5%. Should the numbers surprise to the upside, calming concerns that the US trade frictions could cut back investments in the business sector, the dollar could attract some buying interest.

Separately, pending home sales due 1400 GMT are anticipated to increase by 0.5% m/m in May after a decline of 1.3% in the prior month.

Still, any deterioration or improvement in the trade situation could offset the impact of the above data.

Meanwhile, in oil markets, the EIA weekly report on US oil inventories could move prices at 1430 GMT. Recall that the API figures indicated a sharp downfall of 9.2mn barrels in US crude stocks in the week ending June 22, with crude prices hitting fresh highs in the wake of the data. In case the EIA figures unexpectedly show a bigger decrease than the 2.5mn decline currently priced in, then the market could post additional gains.

On the monetary policy front, the Reserve Bank of New Zealand will announce its decision on interest rates early on Thursday (Wednesday 2100 GMT). Analysts, though, are highly expecting policymakers to keep borrowing costs unchanged at 1.75% for the eleventh consecutive time as GDP growth in the first quarter weakened as expected, hinting that the economy is not ready yet to welcome a rate hike at times when risks around global trade are flashing red thanks to the US trade policy. Earlier today, New Zealand’s ANZ business confidence stats missed forecasts, retreating from -27.2% to -39.0%, the lowest since November. Therefore, given the data weakness, investors will turn their attention to the rate statement submitted along the rate decision to identify the RBNZ’s outlook on the economy. If the Bank turns more worried about the economy’s prospects (to avoid outlook twice), sending messages that a rate cut could still be on the cards, the kiwi could extend losses. Alternatively, if policymakers use a more hawkish tone, suggesting that the slowdown could be temporary, the local currency could reverse to the upside.

In terms of public appearances, Fed Vice Chair for Supervision Randal Quarles (1500 GMT – permanent FOMC voting member), Boston Fed President Eric Rosengren (1430 GMT – non-voter in 2018) and Bank of Canada Governor Stephen Poloz (1915 GMT) are some of the policymakers to deliver speeches later today.

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals