📑 Table of Contents

- 1. What Is Market Cap Weighting?

- 2. What Is Equal Weighting?

- 3. The S&P 500 Concentration Problem (2026)

- 4. Market Cap Weighted ETFs — The Giants

- 5. Equal Weight ETFs — The Alternative

- 6. Performance Comparison: Market Cap vs Equal Weight (2026)

- 7. Advantages and Disadvantages of Each Approach

- 8. Which ETF Strategy Is Right for You?

- 9. Frequently Asked Questions

1. What Is Market Cap Weighting?

Market capitalisation weighting is the most common indexing method used by ETFs like SPY, IVV, and VOO. Under this approach, each stock in the index is weighted according to its total market capitalisation — the number of outstanding shares multiplied by the current share price. The larger the company, the greater its influence on the index’s performance.

For example, a 1% move in Apple (AAPL) will have a much larger impact on the S&P 500 than a 1% move in a small-cap company. This means the index’s performance is heavily influenced by the largest stocks — creating significant concentration risk. As of 2026, the top 10 stocks in the S&P 500 account for more than 35% of the index’s total weight.

Market cap weighting is simple, transparent, and cost-effective. It requires minimal rebalancing because the index naturally adjusts as stock prices change. This is why most popular S&P 500 ETFs use this method.

2. What Is Equal Weighting?

Equal weighting is an alternative indexing method where each stock in the index receives the same allocation, regardless of company size. The most popular equal-weight S&P 500 ETF is RSP (Invesco S&P 500 Equal Weight ETF), which holds all 500 stocks but gives each company an equal weight of approximately 0.2% of the fund’s assets.

This approach provides better diversification and reduces concentration risk. In an equal-weight fund, a 1% move in Apple has the same impact as a 1% move in any other stock. This can be particularly advantageous when the market is broadening beyond the largest tech giants.

Equal-weight ETFs require regular rebalancing (typically quarterly) to maintain equal allocations. This rebalancing process can capture mean reversion — buying stocks that have underperformed and selling those that have outperformed — which can enhance long-term returns. However, the rebalancing also leads to higher expense ratios compared to market-cap weighted funds.

3. The S&P 500 Concentration Problem (2026)

The S&P 500 has become increasingly concentrated in recent years, with the “Magnificent Seven” (Apple, Microsoft, Nvidia, Alphabet, Amazon, Meta, and Tesla) dominating the index. As of 2026, these seven stocks alone account for approximately 28-30% of the entire S&P 500 market cap.

This concentration creates significant single-stock risk for investors in market-cap weighted ETFs. When a handful of stocks drive the index’s performance, the benefits of diversification are diminished. If these stocks experience a correction, the entire index suffers disproportionately.

The equal-weight approach offers a solution. By giving each stock an equal allocation, RSP and similar funds reduce the influence of mega-cap tech stocks. Technology makes up about 16% of RSP, compared to roughly 28% in SPY. This more balanced sector exposure can lead to smoother returns and reduced drawdowns during tech-sector corrections.

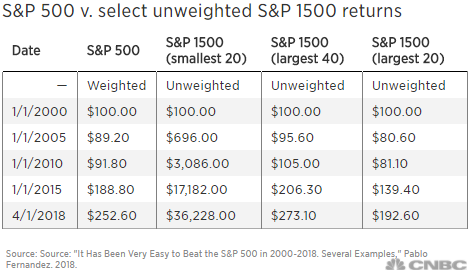

In fact, the equal-weight index has outperformed the market-cap version in 12 of the past 21 calendar years, according to historical data. This suggests that the equal-weight approach can provide superior long-term returns while also offering better diversification.

4. Market Cap Weighted ETFs — The Giants

Three major ETFs dominate the market-cap weighted S&P 500 space. Each has slightly different characteristics but follows the same underlying indexing methodology.

SPY — The Original

SPY (SPDR S&P 500 ETF Trust) is the oldest and most widely traded ETF in the world. As of 2026, it has approximately $779 billion in assets under management. SPY tracks a market-cap weighted index of the S&P 500 and has an expense ratio of 0.0945%. Its high liquidity and options volume make it a favourite among active traders.

IVV — The Low-Cost Alternative

IVV (iShares Core S&P 500 ETF) is managed by BlackRock and has grown to approximately $831 billion in AUM. Its expense ratio is just 0.03%, making it one of the cheapest S&P 500 ETFs available. IVV is particularly popular among long-term investors seeking low-cost core exposure.

VOO — Vanguard’s Offering

VOO (Vanguard S&P 500 ETF) is Vanguard’s entry in the S&P 500 space. With approximately $838 billion in AUM and an expense ratio of 0.03%, it is another extremely cost-effective option. VOO benefits from Vanguard’s reputation for low-cost investing and is a favourite among buy-and-hold investors.

5. Equal Weight ETFs — The Alternative

While market-cap weighted ETFs dominate the landscape, equal-weight ETFs have gained significant traction in recent years, particularly as concentration risk has become a growing concern.

RSP (Invesco S&P 500 Equal Weight ETF) is the most popular equal-weight S&P 500 ETF. As of 2026, it has approximately $83.2 billion in assets under management and an expense ratio of 0.20%.

RSP’s sector allocation is more balanced than market-cap weighted funds, with technology making up about 16% of the portfolio compared to roughly 28% in SPY. This reduces exposure to the tech sector and increases exposure to other sectors like financials, industrials, and healthcare.

The fund rebalances quarterly to maintain equal weights, which can capture mean reversion and potentially enhance returns. In 2026, RSP has seen significant inflows, with $3.6 billion entering the fund at the start of the year as investors sought to reduce concentration risk.

6. Performance Comparison: Market Cap vs Equal Weight (2026)

2026 has been a strong year for both market-cap and equal-weight S&P 500 ETFs, but the equal-weight approach has shown a noticeable edge. The table below compares the key metrics.

| Metric | SPY (Market Cap) | RSP (Equal Weight) | Difference |

|---|---|---|---|

| YTD Return (2026) | 8.4–10.2% | 9.7–11.4% | +1.3% advantage to RSP |

| Technology Exposure | ~28% | ~16% | RSP more diversified |

| Concentration Risk | High (top 10 stocks dominate) | Low (equal allocation) | RSP reduces risk |

| Rebalancing | Automatic (market driven) | Regular (quarterly) | RSP captures mean reversion |

📌 2026 performance data reflects the widest margin in six years, as the market broadens beyond the Magnificent Seven.

7. Advantages and Disadvantages of Each Approach

Both market-cap and equal-weight ETFs have their strengths and weaknesses. Understanding these trade-offs is essential for making an informed investment decision.

| Aspect | Market Cap Weighted | Equal Weighted |

|---|---|---|

| Advantages | Lower fees, simpler, tracks the market perfectly | Better diversification, higher long-term returns, captures mean reversion |

| Disadvantages | Concentration risk, overweights overvalued stocks, performance drag from mega-caps | Higher fees, requires rebalancing, more volatile in some periods |

| Best For | Low-cost core portfolio, “set and forget” investors | Investors seeking diversification, value-oriented approach |

📌 Many investors use both approaches in their portfolios to balance cost, diversification, and return potential.

8. Which ETF Strategy Is Right for You?

The choice between market-cap and equal-weight ETFs depends on your investment goals, risk tolerance, and market outlook. Here is a simple decision framework to help you decide.

Choose Market Cap Weighted (SPY, IVV, VOO) if:

- You want the lowest possible fees (0.03% for IVV and VOO)

- You believe in efficient markets and want to track the market precisely

- You are a buy-and-hold investor who prefers a “set and forget” approach

- You are comfortable with the concentration risk in mega-cap tech stocks

Choose Equal Weight (RSP) if:

- You want better diversification and reduced concentration risk

- You believe mean reversion will benefit smaller and mid-cap stocks

- You are willing to pay a slightly higher fee (0.20%) for the rebalancing benefit

- You are concerned about the dominance of the Magnificent Seven

Consider a Combination

Many investors choose to hold both types of ETFs in their portfolios. For example, you might allocate 70-80% to a low-cost market-cap ETF like IVV or VOO and 20-30% to an equal-weight ETF like RSP. This approach combines the low fees of market-cap weighting with the diversification benefits of equal weighting.

9. Frequently Asked Questions

What is market cap weighting in ETFs?

Market cap weighting is an indexing method where stocks are weighted according to their total market capitalisation. Larger companies have a greater influence on the index’s performance. For example, a 20% move in Apple can shift the entire S&P 500 by more than half a percent.

What is equal weighting in ETFs?

Equal weighting is an indexing method where each stock in the index receives the same allocation, regardless of company size. This provides better diversification and reduces concentration risk in the largest stocks.

Which performs better — market cap weighted or equal weight ETFs?

Historically, equal-weight ETFs have outperformed their market-cap counterparts in many periods. In 2026, the Invesco S&P 500 Equal Weight ETF (RSP) is up 9.7–11.4%, compared to SPY’s 8.4–10.2%. Equal-weight has outperformed in 12 of the past 21 calendar years.

What is the S&P 500 concentration problem?

The concentration problem refers to the fact that a handful of large companies (the “Magnificent Seven”) now make up a disproportionate share of the S&P 500. This creates concentration risk where the performance of the entire index depends heavily on a few stocks.

What is RSP ETF?

RSP is the Invesco S&P 500 Equal Weight ETF. It holds all S&P 500 stocks but gives each company equal weight, significantly reducing exposure to mega-cap tech stocks. Its sector allocation is more balanced, with technology making up about 16% of the fund.

What is SPY ETF?

SPY (SPDR S&P 500 ETF) is the largest and oldest S&P 500 ETF. It tracks a market-cap weighted index of the S&P 500 with approximately $779 billion in assets under management as of 2026.

Why is equal-weight outperforming in 2026?

Equal-weight is outperforming in 2026 because the market is broadening beyond the Magnificent Seven tech stocks. Smaller and mid-cap companies are catching up, and the equal-weight approach captures this broader market participation.

Are equal-weight ETFs more expensive?

Yes, equal-weight ETFs typically have higher expense ratios because they require regular rebalancing to maintain equal allocations. RSP’s expense ratio is 0.20%, compared to SPY’s 0.0945%.

Which S&P 500 ETF has the lowest fees?

IVV (iShares Core S&P 500 ETF) and VOO (Vanguard S&P 500 ETF) both have expense ratios of 0.03%, making them the lowest-cost S&P 500 ETFs available.

Should I invest in market cap weighted or equal weight ETFs?

The answer depends on your investment goals. Market cap weighted ETFs (SPY, IVV, VOO) are ideal for low-cost, broad market exposure. Equal weight ETFs (RSP) are better for investors seeking diversification, reducing concentration risk, and capturing mean reversion. Many investors use both in their portfolios.

📖 Need Help Choosing the Right ETF? Visit our comprehensive Help Centre for detailed guides on ETF investing, portfolio construction, and risk management. Whether you are a beginner or an experienced investor, our resources will help you make informed decisions about market-cap weighted and equal-weight ETFs, and how they fit into your overall investment strategy.

🤖 Automate Your Trading Strategy: While ETFs provide excellent long-term exposure, active traders can complement their portfolios with automated trading solutions. Browse our curated collection of forex trading robots and Expert Advisors — fully automated systems designed to execute a variety of strategies across different market conditions. Our robots trade 24/7, eliminate emotional decision-making, and have been tested across multiple market environments.

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals