Hot on the heels of the preliminary GDP readings, Eurostat will publish the flash estimates of Eurozone inflation for October on Wednesday at 10:00 GMT. With growth in the euro area unexpectedly slowing in the third quarter, the inflation numbers will likely bring better news for policymakers as both headline and underlying measures are anticipated to move higher. An upward trend could offer some support for the euro, which continues to be weighed by a weakening growth outlook and renewed political uncertainty in Europe.

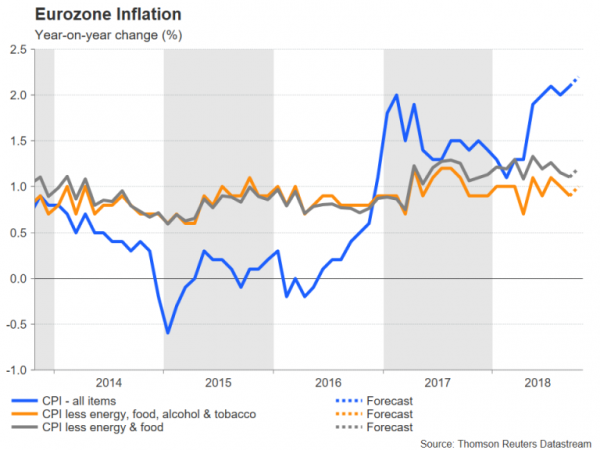

The 12-month rate of the consumer price index (CPI) has stood at or above 2% since June, as higher energy prices push up the headline measure. A further pickup is expected in October with CPI forecast to rise by 2.2% year-on-year, up from 2.1% in September. However, looking at the two core gauges monitored by the European Central Bank, there’s been little progress in lifting underlying prices. When excluding energy and food items, CPI stood at 1.1% y/y in September, while the narrower measure that strips out alcohol and tobacco as well was 0.9%. Both are forecast to nudge upwards in October, with the former rising to 1.2% and the latter to 1.0%.

The absence of underlying price pressures is putting into question the ECB’s normalization plans, though the central bank’s chief, Mario Draghi, remains confident core inflation will recover. Draghi told reporters at the October policy meeting that while underlying inflation currently remains muted, he expects it to increase towards the end of the year. Should a pickup remain elusive, however, the ECB could be forced to contemplate extending its asset purchase program beyond December 2018, when the program is expected to end.

In the meantime, the odds that Eurozone growth and inflation would not evolve within the ECB’s projections were given a boost on Tuesday when GDP data showed the bloc’s economy expanded by just 0.2% during the third quarter – half the prior and expected rate of 0.4%. This only adds to the darkening outlook for the Eurozone economy, which has been clouded by the US-China trade war, a slowing Chinese economy, and closer to home, by fears that the budget stand-off between Italy and the EU could lead to a full-blown crisis.

These factors have strongly contributed to the euro’s downtrend during 2018. Any positive developments therefore on the inflation front could provide the single currency with a much-needed lift, at least in the short term, as it would back the ECB’s plans to gradually withdraw monetary stimulus.

An upside surprise to the CPI data could help euro/dollar overcome immediate resistance at around 1.1408, which is the 78.6% Fibonacci retracement level of the August-September upleg from 1.1297 to 1.1815. Clearing this hurdle would strengthen any positive momentum and drive the pair towards the 61.8% and 50% Fibonacci levels at 1.1495 and 1.1556, respectively.

But if the inflation numbers fall short of expectations, euro/dollar could come under fresh selling pressure, with the August low of 1.1297 being the immediate barrier to the downside. A break below this level would open the way for the 123.6% Fibonacci extension at 1.1175, followed by the 138.2% Fibonacci at the 1.11 handle.

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals