Dollar’s decline slowed today, ahead of FOMC rate decision. But there is so far no momentum for a sustainable rebound. It’s like trading mixed as a bystander for now. Instead, major movements are found in Euro and Sterling, which start to weaken mildly. Euro is somewhat weighed down by European Commission’s new forecasts. The Pound, on the other hand, starts to lose steam as there is no positive Brexit news to give it another lift. Australian Dollar remains the strongest one for today but it’s now followed by Canadian Dollar, which is having a comeback.

Technically, some pairs are clearly losing momentum just ahead of key resistance levels. Those include AUD/USD ahead of 0.7314, EUR/JPY ahead of 130.20 and GBP/JPY ahead of 149.70. It’s a bit early to tell but these pairs could be building up a turnaround. Considering FOMC as background, USD/CHF and USD/JPY and USD/CAD are worth a watch today. All three are bounded in tight range this week, below 1.0094, 113.81 and 1.3170 resistance respectively. The pullbacks are all rather shallow in these three. In case of a Dollar comeback, these three may move first.

In other markets, European indices are mixed for the moment. FTSE is up 0.39% but DAX is down -0.16% and CAC is down -0.12%. German 10 year yield is up 0.0018 at 0.452. Italian 10 year yield is up 0.066 at 3.408. German-Italian spread stays below 300 for now. Major Asian indices closed higher except China. Nikkei gained 1.82%, Hong Kong HSI rose 0.31% and Singapore Strait Times added 0.91%. But China Shanghai SSE dropped -0.22%. Gold failed to stay above 1235 this week and it’s now back pressing 1220.

NOTE: We offer you free download forex robot based on stop and reverse system for testing results in Metatrader.

US initial claims dropped to 214k, continuing claims lowest since 1973

US initial jobless claims dropped -1k to 214k in the week ended November 3. Four-week moving average of initial claims dropped -0.25k to 213.75k. Continuing claims dropped -8k to 1.623m in the week ended October 27, lowest since July 28, 1973. Four-week moving average of continuing claim dropped -7.5k to 1.64075m, lowest since August 11, 1973. From Canada, new housing price index rose 0.0% in September, housing starts rose to 206k in October.

Released earlier, German trade surplus narrowed to trade surplus narrowed to EUR 17.6B in September. Swiss unemployment rate was unchanged at 2.5% in October. From China, exports rose 15.6% yoy in October to USD 217.3B. Imports rose 21.4% yoy to USD 183.2B. Trade surplus widened to USD 34.0B. UK RICS house price balance dropped to -10 in October, lowest since September 2012. Japan machine orders dropped -18.3% mom in September. Current account surplus narrowed to JPY 1.33T.

Fed to stand pat and reiterates economy is strong, inflation on target

The upcoming focus will turn to FOMC rate decision and statement. Fed is widely expected to keep federal funds rate unchanged at 2.00-2.25%. Also, the accompanying statement would also reiterate the strength in the job market as well as strong rate of growth. Also, inflation is near Fed’s target of 2%. The focus for the near term is another rate hike in December. Currently, fed funds futures are pricing in around 80% chance of that. For 2019, we’d probably only get more hints on Fed policy makers’ view in next economic projections. But so far, it seems there is consensus among FOMC members that Fed would at least continue the rate hike till hitting neutral rate level.

More readings on FOMC:

Eurozone 2019 growth forecasts lowered, inflation to dive to only 1.6% in 2020

The European Commission lowered 2019 Eurozone growth forecast by 0.1% to 1.9%, then slow to 1.7% in 2020. HICP inflation forecast for both 2018 and 2019 are raised by 0.1% to 1.8%. However, HICP inflation is projected to slow down to 1.6% in 2020.

In the release European Commission warned that “rising global uncertainty, international trade tensions and higher oil prices will have a dampening effect on growth in Europe”. And looking ahead “the drivers of growth are set to become increasingly domestic”.

There are two interesting points to note. Firstly, inflation is forecast to move away from ECB’s 2% target in 2020, reflecting further slowdown in activity. Does that mean ECB shouldn’t raise interest rates in 2019? Secondly, Italy’s budget deficit is projected at -2.9% of GDP in 2019, way higher than its government’s own target of -2.4%. In 2020, Italy’s deficit is even projected to exceed EU’s limit of -3%.

NOTE: if you do not have time to search for strategies and study all the tools of the trade, you do not have the extra funds for testing and errors, tired of taking risks and incurring losses – trade with the help of our best forex robots developed by our professionals.

This is a quick summary:

GDP growth at

- 2.1% in 2018 vs 2.1% (Summer) vs 2.3% (Spring)

- 1.9% in 2019 vs 2.0% (Summer) vs 2.0% (Spring)

- 1.7% in 2020

HICP inflation at

- 1.8% in 2018 vs 1.7% (Summer) vs 1.5% (Spring)

- 1.8% in 2019 vs 1.7% (Summer) 1.6% (Spring)

- 1.6% in 2020

Tria: EU forecasts of Italy deficit inaccurate and incomplete

Italian Economy Minister Giovanni Tria complained that the new budget deficit forecasts for Italy by European Commission released today. The Commission projected Italy’s deficit to hit 2.9% of GDP in 2019. Even worse, Italy’s deficit is projected to hit 3.1% in 2020, breaking EU’s 3% limit. This is much higher than Italy’s own target of 2.4% in 2019.

Tria said “the European Commission’s forecasts for the Italian deficit are in sharp contrast to those of the Italian government and derive from an inaccurate and incomplete analysis.” Though, Tria also said that the projections would not affect the “continuation of constructive dialogue” with the Commission. And, the coalition government is committed to the 2.4% deficit target.

ECB: Ongoing broad-based expansion to continue, markets revised up interest rate expectations

ECB’s monthly bulletin paints an upbeat picture on the Eurozone economy. In short, even though incoming information was “somewhat weaker than expected”, they remains consistent with “ongoing broad-based economic expansion”. The expansion is supported by ” domestic demand and continued improvements in the labour market. Risks are “broadly balanced”.

On prices, measures of underlying inflation “remained generally muted but stand above earlier lows”. At the same time “Supply chain price pressures for non-energy industrial goods in the HICP continued to increase.” “Wage growth developments point to increasing domestic cost pressures.”

Also, ECB noted that the EONIA forward curve shifted slightly upwards over the review period. And, that indicates “market participants revised up their interest rate expectations for longer horizons.”

UK Hunt: Brexit negotiation in final stage but seven days is probably pushing it

UK Foreign Minister Jeremy Hunt said in Paris today that Brexit negotiation is in a “final stage”. Regarding EU, he said “I am confident that we will reach an agreement because it is in all sides interest to reach an agreement.” However, he also emphasized that “seven days is probably pushing it”, referring to question whether the agreement could be done within seven days.

Domestically, Hunt said “we are confident that we will be able to get a final deal through parliament for the simple reason that Theresa May is not going to sign up to a deal that is inconsistent with the letter and spirit of the referendum.”

RBNZ Orr refuses to rule out rate cut, but NZD stays firm

New Zealand Dollar stays firm after RBNZ left OCR unchanged at 1.75% as widely expected. In the accompanying statement, RBNZ maintained the intention to keep OCR unchanged “through 2019 and into 2020”.

The language that the “the direction of our next OCR move could be up or down” was removed. Instead, RBNZ said “there are both upside and downside risks to our growth and inflation projections. As always, the timing and direction of any future OCR move remains data dependent.”. That at first glance looked like the central bank is moving away from the possibility of a cut. However, Governor Adrian Orr made it clear in the press conference that “it would be pointless to remove that option”, regarding a cut.

Orr also talked down the pick-up in GDP growth in the June quarter as “partly due to temporary factors”. Instead, he pointed to businesses surveys which “suggest growth will be soft in the near term”. While employment is “around its “maximum sustainable level”, core inflation remains below 2% target mid-point, “necessitating continued supportive monetary policy”.

More readings on RBNZ

China-US trade shrank sharply in October, exports down -8.5%, imports down -12.9%

Trade data from China showed sharp decline in trade between the US and China in October, clearly a result of tariffs. To highlight, exports to US dropped -8.5% mom. Imports from US dropped even more by -12.9% mom. One might argue that imports from EU also dropped -12.5% mom. Admittedly, that could be a warning sign of slowdown in the Chinese economy. But over the year, imports from EU did rose 12.3% yoy.

In USD term, exports rose 15.6% yoy in October to USD 217.3B. Imports rose 21.4% yoy to USD 183.2B. Trade surplus widened to USD 34.0B, below expectation of USD 36.3B.

In CNY terms, exports rose 20.1% to CNY 1490B. Imports rose 26.3% to 1257B. Trade surplus widened to CNY 234B, above expectation of CNY 209B.

More details in this quick note.

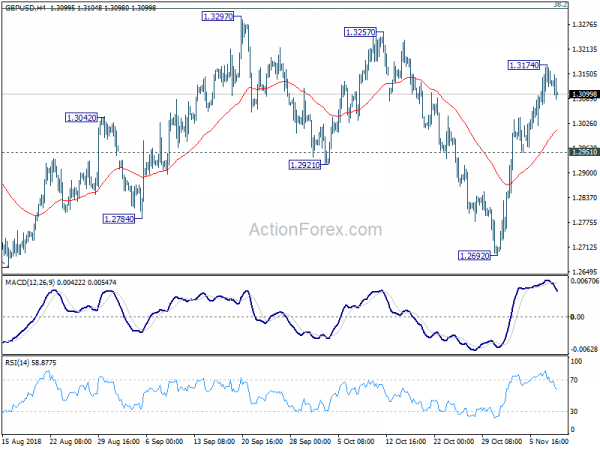

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3076; (P) 1.3125; (R1) 1.3177; More…

Intraday bias in GBP/USD stays neutral for consolidation below 1.3174 temporary top. With 1.2951 minor support intact, further rise could still be seen to 1.3257/3297 resistance zone. However, as rise fro 1.2692 is seen as the third leg of consolidation pattern from 1.2661, we’d expect strong resistance from 1.3316 fibonacci level to limit upside to bring down trend resumption eventually. On the downside, below 1.2951 minor support will turn bias back to the downside for 1.2692 and then 1.2661 key support.

In the bigger picture, whole medium term rebound from 1.1946 (2016 low) should have completed at 1.4376 already, after rejection from 55 month EMA. The structure and momentum of the fall from 1.4376 argues that it’s resuming long term down trend. And this will be the preferred case as long as 38.2% retracement of 1.4376 to 1.2661 at 1.3316 holds. However, firm break of 1.3316 would bring stronger rebound to 61.8% retracement at 1.3721. And, the eventual depth of the fall from 1.4376, and the chance of hitting 1.1946 low, will depend on the strength of the interim corrective rebound from 1.2661.

Economic Indicators Update

56B48B

2.00%2.00%

2.25%2.25%

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 20:00 | NZD | RBNZ Official Cash Rate | 1.75% | 1.75% | 1.75% | |

| 23:50 | JPY | BOJ Summary of Opinions | ||||

| 23:50 | JPY | Machine Orders M/M Sep | -18.30% | -8.90% | 6.80% | |

| 23:50 | JPY | Current Account (JPY) Sep | 1.33T | 1.36T | 1.43T | |

| 00:01 | GBP | RICS House Price Balance Oct | -10.00% | -2.00% | -2.00% | |

| 03:00 | CNY | Trade Balance (USD) Oct | 34.0B | 36.3B | 31.7B | |

| 03:00 | CNY | Trade Balance (CNY) Oct | 234B | 209B | 213B | |

| 05:00 | JPY | Eco Watchers Survey Current Oct | 49.5 | 48.9 | 48.6 | |

| 06:45 | CHF | Unemployment Rate Oct | 2.50% | 2.50% | 2.50% | |

| 07:00 | EUR | German Trade Balance Sep | 17.6B | 21.2B | 18.3B | 18.2B |

| 09:00 | EUR | ECB Economic Bulletin | ||||

| 10:00 | EUR | European Commission Economic Forecasts | ||||

| 13:15 | CAD | Housing Starts Oct | 206K | 195K | 189K | |

| 13:30 | CAD | New Housing Price Index M/M Sep | 0.00% | 0.10% | 0.00% | |

| 13:30 | USD | Initial Jobless Claims (NOV 3) | 214K | 214K | 214K | 215K |

| 15:30 | USD | Natural Gas Storage | ||||

| 19:00 | USD | FOMC Rate Decision (Lower Bound) | ||||

| 19:00 | USD | FOMC Rate Decision (Upper Bound) |

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals