The global financial markets are blessed by strong risk appetite today, as US and China agreed on 90 days ceasefire on trade war. US stock futures point to sharply higher open, following strengthen and European and Asian markets. Australian Dollar, being a close trade partner of both the US and China, and a risk sensitive currency, is the strongest one. Canadian Dollar follows with help from rebound in oil price. Meanwhile, Sterling is the weakest one for today on renewed selloff over Brexit vote worry. For now, it’s likely that the Brexit bill will be voted down by the Parliament on December 11. Yen is the second weakest while Dollar is mixed.

In other markets, major European indices are all trading with gains at the time of writing. FTSE is up 1.69%, DAXC is up 2.21% and CAC is up 1.00%. German 10 year yield is up 0.004 at 0.321. Italian 10 year yield is down -0.0495 at 3.164. German-Italian spread continues to narrow away from 300. There is no concrete result in the budget talk between Italy and EU yet. But just like what European Commission Vice President Valdis Dombrovskis said, “it is positive that the tone of discussion has changed”. Earlier in Asia, Nikkei closed up 1.00% at 22574.76. China Shanghai SSE rose 2.57% to 2654.8. Hong Kong HSI rose 2.55% to 27182.04. Singapore Strait Times rose 2.34% to 3190.62.

Technically, AUD/USD’s rise and EUR/AUD’s fall are both in progress. GBP/USD’s break of 1.2725 minor support suggests decline resumption for 1.2661 low. 144.02 in GBP/JPY and 0.8939 resistance in EUR/GBP will be watched to see if selloff in pound widens. USD/CAD’s break of 1.3187 support today is a strong sign of near term bearish reversal after rejection by 1.3385 resistance.

Fed Clarida: It’s a symmetric inflation objective around 2%

Fed Vice Chair Richard Clarida said in a Bloomberg interview that “we have a symmetric objective around 2 percent.” And he emphasized that “two percent is not meant to be a ceiling”. He added that “we’ve operated below 2 percent, we could operate somewhat above 2 percent, depending on the shocks.” Clarida also said the US economy is in good shape with solid outlook. And, the current monetary policy framework is serving Fed well.

Eurozone PMI manufacturing finalized at 51.8, big four at the bottom

Eurozone PMI manufacturing is finalized at 51.8 in November, revised up from 51.5, down from October’s 52.0. It’s also the lowest since August 2016. Markit noted that growth of production is only marginal as demand continues to falter. Also, business confidence remains weakest in around six years. And, the euro area’s ‘big-four’ economies posted the lowest manufacturing PMI readings of all countries covered by the survey during November.

Among the countries, Italy PMI manufacturing stayed in contraction and dropped to 48.6, a 47-month low. France PMI manufacturing dropped to 50.8, a 26-month low. Germany PMI manufacturing dropped to 51.8, a 31-month low. Spain PMI manufacturing dropped to 3-month low at 52.6.

Chris Williamson, Chief Business Economist at IHS Markit noted that “manufacturers reported that demand is now falling in Germany, France and Italy, while only modest growth was recorded in Spain.” And, “the darker outlook is linked to trade wars and tariffs as well as intensifying political uncertainty and has led to increased risk aversion and a commensurate cutting back on expenditure, notably for investment.

UK PMI manufacturing rose to 53.1, lacklustre picture of manufacturing sector

UK PMI manufacturing rose to 53.1 in November, up from 51.1 and beat expectation of 52.0. Markit noted that trends in output and new orders strengthen slightly. But new export orders decrease for the second month running.

Rob Dobson, Director at IHS Markit. noted that “the November PMI provided a lacklustre picture of the UK manufacturing sector, as ongoing global trade tensions and Brexit uncertainty weighed on current business conditions and dampened the outlook for the year ahead.”

Also released in European session, Swiss retail sales rose 0.8% yoy in October. PMI manufacturing rose to 57.7 in November versus expectation of 56.3.

Japan PMI manufacturing finalized at 52.2, momentum tilting towards a slowdown

Japan PMI manufacturing was finalized at 52.2 in November, revised up from 51.8. Markit noted that new orders rise at joint-weakest rate in just over two years. Also production growth moderates and business confidence drops for sixth month running.

Joe Hayes, Economist at IHS Markit noted that “October’s bounce-back was indeed a transitory jump”. And, “the underlying picture remains subdued, with momentum tilting towards a slowdown.” ” Subdued sales performances reflected fragile conditions both domestically and abroad. According to firms, weak demand from China and parts of Europe hampered export growth.”

Also from Japan, capital spending rose 4.5% in Q3, much lower than expectation of 8.6%.

China Caixin PMI manufacturing rose to 50.2, domestic demand improved, overseas demand subdued

China Caixin PMI rose 0.1 to 50.2 in November, slightly above expectation of 50.1. Markit noted in the release that production is unchanged for the second month running. There is further in crease in total new work, but export trends remains subdued. Meanwhile, input cost inflation softens to seven-month low.

Dr. Zhengsheng Zhong, Director of Macroeconomic Analysis at CEBM Group noted in the release that “Overall, domestic demand across the manufacturing sector improved in November, while overseas demand was still subdued. Production slowed, confidence was relatively stable, capital turnover was improved, and upward pressure on industrial product prices eased. China’s economy was weak, but did not show significant signs of deterioration.”

AUD shrugs weak manufacturing, building and profits data

The Australian Industry Group Performance of Manufacturing Index dropped sharply by -7 to 51.3 in November. That’s the lowest level since October 2017. It’s still the twenty-six months of uninterrupted recovery and expansion, longest streak since 2005. Also from Australia, building approvals dropped -1.5% mom in October, below expectation of -1.4% mom. Company operating profits rose 1.9% qoq, below expectation of 2.9% qoq. From New Zealand terms of trade index dropped -0.3% qoq, below 0.1% qoq expectation.

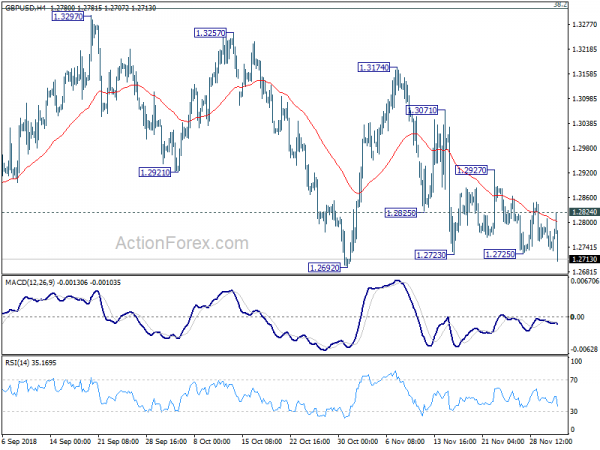

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2721; (P) 1.2766; (R1) 1.2796; More…

GBP/USD’s break of 1.2725 suggests recent fall is resuming. Intraday bias is turned back to the upside for 1.2661 low. Decisive break there will resume larger down trend from 1.4376. On the upside, above 1.2824 minor resistance will turn intraday bias to the upside for rebound. After all, price actions from 1.2661 are viewed as a consolidation pattern. Even in case of strong rebound, upside should be limited by 1.3316 fibonacci level to bring down trend resumption eventually.

In the bigger picture, whole medium term rebound from 1.1946 (2016 low) should have completed at 1.4376 already, after rejection from 55 month EMA. The structure and momentum of the fall from 1.4376 argues that it’s resuming long term down trend. And this will be the preferred case as long as 38.2% retracement of 1.4376 to 1.2661 at 1.3316 holds. However, firm break of 1.3316 would bring stronger rebound to 61.8% retracement at 1.3721. And, the eventual depth of the fall from 1.4376, and the chance of hitting 1.1946 low, will depend on the strength of the interim corrective rebound from 1.2661.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | AUD | AiG Performance of Manufacturing Index Nov | 51.3 | 58.3 | ||

| 21:45 | NZD | Terms of Trade Index Q/Q Q3 | -0.30% | 0.10% | 0.60% | 0.40% |

| 23:50 | JPY | Capital Spending Q3 | 4.50% | 8.60% | 12.80% | |

| 0:00 | AUD | TD Securities Inflation M/M Nov | 0.00% | 0.10% | ||

| 0:30 | AUD | Company Operating Profit Q/Q Q3 | 1.90% | 2.90% | 2.00% | 2.40% |

| 0:30 | AUD | Building Approvals M/M Oct | -1.50% | -1.40% | 3.30% | 5.50% |

| 0:30 | JPY | PMI Manufacturing Nov F | 52.2 | 51.8 | 51.8 | |

| 1:45 | CNY | Caixin PMI Manufacturing Nov | 52.6 | 50.1 | 50.1 | |

| 8:15 | CHF | Retail Sales Real Y/Y Oct | 0.80% | -0.70% | -2.70% | |

| 8:30 | CHF | PMI Manufacturing Nov | 57.7 | 56.3 | 57.4 | |

| 8:45 | EUR | Italy Manufacturing PMI Nov | 48.6 | 48.9 | 49.2 | |

| 8:50 | EUR | France Manufacturing PMI Nov F | 50.8 | 50.7 | 50.7 | |

| 8:55 | EUR | Germany Manufacturing PMI Nov F | 51.8 | 51.6 | 51.6 | |

| 9:00 | EUR | Eurozone Manufacturing PMI Nov F | 51.8 | 51.5 | 51.5 | |

| 9:30 | GBP | PMI Manufacturing Nov | 53.1 | 52 | 51.1 | |

| 14:30 | CAD | Manufacturing PMI Nov | 53.9 | |||

| 15:00 | USD | Construction Spending M/M Oct | 0.40% | 0.00% | ||

| 14:45 | USD | Manufacturing PMI Nov F | 55.4 | 55.4 | ||

| 15:00 | USD | ISM Manufacturing Nov | 57.5 | 57.7 | ||

| 15:00 | USD | ISM Prices Paid Nov | 70.5 | 71.6 | ||

| 15:00 | USD | ISM Employment Nov | 56.8 |

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals