US and China agreed not to escalate trade war after meeting between Trump and Xi. A cease-fire agreement was reached. Even though it’s just for 90 days, Asian markets responded positively to the development with all major indices recording solid gains. DOW futures are also pointing to a day of 2% gain for now. In the currency markets, Australian Dollar is the biggest beneficiary and have a strong head start to a busy week. Canadian Dollar and New Zealand Dollar follow as the next strongest. Yen is naturally the weakest one on return of risk appetite. Dollar is the second worst performing, and will need some support from this week’s data including NFP, as well as Powell’s testimony to reversed weakness.

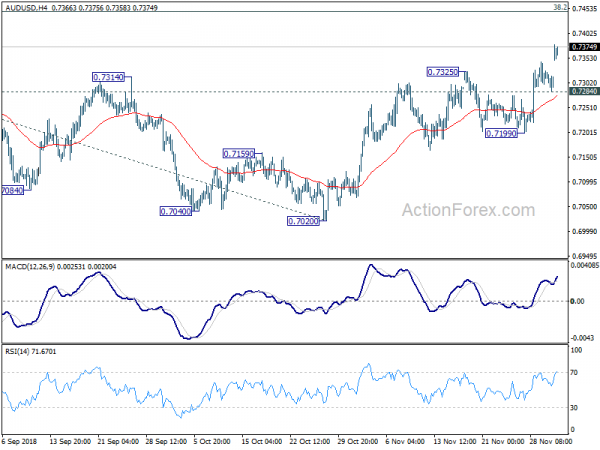

Technically, AUD/USD finally shows some conviction by gapping up through 0.7314 key resistance. That should seal the case of medium term bullish reversal and next target is 0.7446 fibonacci level. USD/CAD’s steep fall today also add credence to the case of rejection of 1.3385 resistance Immediate focus is back on 1.3187 support for confirming near term reversal. Elsewhere, EUR/USD, GBP/USD, USD/CHF, USD/JPY, EUR/GBP, EUR/JPY and GBP/JPY are all staying in familiar range only.

In other markets, Nikkei closed up 1.0% or 223.7 pts at 22574.76. Hong Kong HSI is up 2.46% at the time of writing. China Shanghai SSE is up 2.57%. Singapore Strait Times is up 2.26%. 10 year JGB yield is down -0.0049 at 0.086, below 0.09 handle. WTI crude oil rebound strongly and is now at 53.3. Gold is attempting to recover on Dollar weakness and is pressing 1230.

US-China trade war ceasefire for 90 days, China to work on reforms immediately

US President Donald Trump hailed that he had an “amazing and productive meeting” with Chinese President Xi Jinping, as sideline of G20 summit in Argentina. Both sides agreed to ceasefire on trade war for 90 days and work on structural changes in China. China also agreed to start buying US agriculture products immediately. Trump said there are “unlimited possibilities for both the United States and China.”

In a White House statement:

- Trump agreed NOT to raise the tariffs on USD 200B of Chinese progress to 25% on January 1, but leave them at 10%.

- China will purchase a “very substantial” amount of agricultural, energy, industrial, and other product from the US, starting immediately with agriculture.

- Most importantly, negotiations will immediately begin on structural reforms regarding “forced technology transfer, intellectual property protection, non-tariff barriers, cyber intrusions and cyber theft, services and agriculture. “

- The negotiations will be completed within the next 90 days. If an agreement couldn’t be made, the above mentioned tariffs will be raised from 10% to 25%.

Just a day after the cease-fire agreement with China. Trump just tweeted that China has agreed to “reduce and remove tariffs on cars” from the US. And the current tariff is 40%.

Japan PMI manufacturing finalized at 52.2, momentum tilting towards a slowdown

Japan PMI manufacturing was finalized at 52.2 in November, revised up from 51.8. Markit noted that new orders rise at joint-weakest rate in just over two years. Also production growth moderates and business confidence drops for sixth month running.

Joe Hayes, Economist at IHS Markit noted that “October’s bounce-back was indeed a transitory jump”. And, “the underlying picture remains subdued, with momentum tilting towards a slowdown.” ” Subdued sales performances reflected fragile conditions both domestically and abroad. According to firms, weak demand from China and parts of Europe hampered export growth.”

Also from Japan, capital spending rose 4.5% in Q3, much lower than expectation of 8.6%.

China Caixin PMI manufacturing rose to 50.2, domestic demand improved, overseas demand subdued

China Caixin PMI rose 0.1 to 50.2 in November, slightly above expectation of 50.1. Markit noted in the release that production is unchanged for the second month running. There is further in crease in total new work, but export trends remains subdued. Meanwhile, input cost inflation softens to seven-month low.

Dr. Zhengsheng Zhong, Director of Macroeconomic Analysis at CEBM Group noted in the release that “Overall, domestic demand across the manufacturing sector improved in November, while overseas demand was still subdued. Production slowed, confidence was relatively stable, capital turnover was improved, and upward pressure on industrial product prices eased. China’s economy was weak, but did not show significant signs of deterioration.”

AUD shrugs weak manufacturing, building and profits data

The Australian Industry Group Performance of Manufacturing Index dropped sharply by -7 to 51.3 in November. That’s the lowest level since October 2017. It’s still the twenty-six months of uninterrupted recovery and expansion, longest streak since 2005. Also from Australia, building approvals dropped -1.5% mom in October, below expectation of -1.4% mom. Company operating profits rose 1.9% qoq, below expectation of 2.9% qoq. From New Zealand terms of trade index dropped -0.3% qoq, below 0.1% qoq expectation.

But overall, AUD/USD couldn’t care less about the weak data. It surges sharply today on news of US-China trade war ceasefire. AUD/USD should now be in medium term rebound to 0.7446 fibonacci level.

Big week for USD, AUD and CAD

Looking ahead, Fed chair Jerome Powell’s testimony will be a major focus of the week. Powell will have a chance to be scrutinized and clarify his views on how close interesting rate is to neutral, being “just below”. Many Fed officials are also busy speaking this week, paving the way for another hike on December 19, two weeks away. And of course, US data like ISM indices and non-farm payrolls will be closely watched.

It’s a big week for Australia. Aussie got a head start with the help from US-China trade war cease fire. But challenges lie ahead. RBA is expected to keep interest rate unchanged at 1.50% and maintain a neutral stance. Australia will also release GDP, retail sales, and trade balance.

It’s also a big week for Canadian Dollar. BoC is widely expected to keep interest rate unchanged at 1.75%. Canada will release trade balance, Ivey PMI and employment data. But OPEC meeting could be more moving for the Loonie.

Besides, there are numerous important data to be featured including UK PMIs, Swiss CPI, etc. Here are some highlights for the week:

- Monday: China Caixin PMI manufacturing; Eurozone PMI manufacturing final. UK PMI manufacturing; US ISM manufacturing , construction spending

- Tuesday: Japan monetary base; RBA rate decision, Australia current account; Swiss CPI; UK construction PMI; Eurozone PPI; Canada labor productivity

- Wednesday: Australia GDP; China Caixin PMI services; Eurozone PMI services final; UK PMI services; Eurozone retail sales; US ADP employment; non-farm productivity; ISM services, Fed’s Beige Book; BoC rate decision

- Thursday: Australia retail sales, trade balance; Germany factory orders; Canada trade balance, Ivey PMI; US trade balance, factory orders, jobless claims

- Friday: Japan average cash earnings, leading indicators; Germany industrial production; Swiss foreign currency reserves; Eurozone employment, GDP revision; Canada employment; US non-farm payroll, U of Michigan consumer sentiment

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7289; (P) 0.7308; (R1) 0.7332; More…

AUD/USD surges to as high as 0.7380 so far today. The strong break of 0.7314 resistance finally confirmed medium term reversal. Intraday bias is on the up side for further rally to 38.2% retracement of 0.8135 to 0.7020 at 0.7446 and above. On the downside, break of 0.7284 minor support will turn intraday bias neutral first. But near term outlook will stay bullish as long as 0.7199 support holds.

In the bigger picture, AUD/USD’s decline from 0.8135 should have completed at 0.7020 already, ahead of 0.6826 key support (2016 low). Stronger rebound should be seen. But still, we’d expect strong resistance from 0.7500 support turned resistance to limit upside. Medium term fall from 0.8135 should extend to take on 0.6826 low at a later stage.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | AUD | AiG Performance of Manufacturing Index Nov | 51.3 | 58.3 | ||

| 21:45 | NZD | Terms of Trade Index Q/Q Q3 | -0.30% | 0.10% | 0.60% | 0.40% |

| 23:50 | JPY | Capital Spending Q3 | 4.50% | 8.60% | 12.80% | |

| 00:00 | AUD | TD Securities Inflation M/M Nov | 0.00% | 0.10% | ||

| 00:30 | AUD | Company Operating Profit Q/Q Q3 | 1.90% | 2.90% | 2.00% | 2.40% |

| 00:30 | AUD | Building Approvals M/M Oct | -1.50% | -1.40% | 3.30% | 5.50% |

| 00:30 | JPY | PMI Manufacturing Nov F | 52.2 | 51.8 | 51.8 | |

| 01:45 | CNY | Caixin PMI Manufacturing Nov | 50.2 | 50.1 | 50.1 | |

| 08:15 | CHF | Retail Sales Real Y/Y Oct | -0.70% | -2.70% | ||

| 08:30 | CHF | PMI Manufacturing Nov | 56.3 | 57.4 | ||

| 08:45 | EUR | Italy Manufacturing PMI Nov | 48.9 | 49.2 | ||

| 08:50 | EUR | France Manufacturing PMI Nov F | 50.7 | 50.7 | ||

| 08:55 | EUR | Germany Manufacturing PMI Nov F | 51.6 | 51.6 | ||

| 09:00 | EUR | Eurozone Manufacturing PMI Nov F | 51.5 | 51.5 | ||

| 09:30 | GBP | PMI Manufacturing Nov | 52 | 51.1 | ||

| 14:30 | CAD | Manufacturing PMI Nov | 53.9 | |||

| 15:00 | USD | Construction Spending M/M Oct | 0.40% | 0.00% | ||

| 14:45 | USD | Manufacturing PMI Nov F | 55.4 | 55.4 | ||

| 15:00 | USD | ISM Manufacturing Nov | 57.5 | 57.7 | ||

| 15:00 | USD | ISM Prices Paid Nov | 70.5 | 71.6 | ||

| 15:00 | USD | ISM Employment Nov | 56.8 |

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals