Asian stocks open the week lower, following Friday’s selloff in the US. But the forex markets are pretty steady. Dollar is the weakest one for now, followed by Sterling and then Canadian. On the other hand, New Zealand Dollar leads the way higher, followed by Euro and then Japanese Yen. As usual on a Monday, the picture could drastically change throughout the day. In particular, Sterling is still hibernating in tight range except versus Euro. It might finally wake up as Tuesday’s Brexit deal vote approaches.

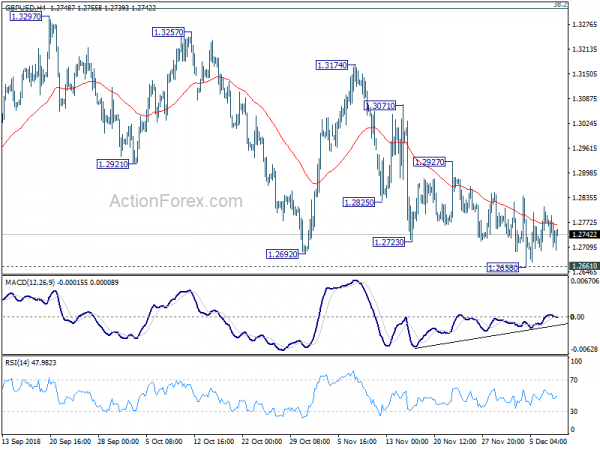

Technically, while EUR/USD strengthens today, it’s capped below 1.1472 resistance and thus, there is not indication of bullish reversal yet. This is a key level to watch should Dollar’s weakness extends. On the other hand, 1.2661 is key support in GBP/USD is another level to pay attention to. Break of which will be a sign that Sterling bears are finally coming out.

In other markets, at the time of writing. Nikkei is down -2.19%. Hong Kong HSI is down -1.41%. China Shanghai SSE is down -0.84% and Singapore Strait Times is down -1.36%. Japan 10 year JGB yield is down -0.0166 at 0.046.

UK PM May: Voting down the Brexit deal would take UK into uncharted waters

Ahead of the parliamentary vote on the Brexit deal on Tuesday, Prime Minister Theresa May warned on Sunday that voting down the deal could take the UK into “uncharted waters”. And, that would mean “grave uncertainty for the nation with a very real risk of no Brexit or leaving the European Union with no deal.” She added “when I say if this deal does not pass we would truly be in uncharted waters, I hope people understand this is what I genuinely believe and fear could happen.”

At this, chance remains very slim for the bill to be passed. And there are rumor that May could pull the plug and postpone the vote. And she could go back to Brussels for some tweaks first. but Brexit Minister Stephen Barclay warned that “the risk for those who say simply go back and ask again, the risk is that isn’t necessarily a one way street, the French the Spanish and others will turn round, if we seek to reopen the negotiation, and ask for more.”

USTR Lighthizer: Trade talks with China not going beyond March

US Trade Representative Robert Lighthizer commented on trade negotiation with China for the first time since taking the leading role. He noted that 90 days talk has a “hard deadline” and Trump is “not talking about going beyond March. And, “the way this is set up is that at the end of 90 days, these tariffs will be raised”. US has postponed raising of tariffs on USD 200B in Chinese imports from 10% to 25% after Trump-Xi meeting.

Lighthizer also said the US need “agricultural sales” and “manufacturing sales”. But at the same time “we need structural changes on this fundamental issue of non-economic technology transfer.” And, Americans “can be reassured that if there is a deal that can be made that will assure the protection of U.S. technology…and get additional market access…the president wants us to do it.” But he also echoed Trump’s rhetorics that “if not we will have tariffs.”

OECD: RBA policy rates should start to rise soon

In a report released over the weekend, OECD said Australia’s “long span of positive output growth continues”. And, “continued robust output growth of around 3% is projected in the near future”. On RBA, OECD said that “in the absence of negative shocks, policy rates should start to rise soon”. It warned that “monetary conditions remain very accommodative, with the risk of imbalances accumulating further if the low-interest rate environment persists.” And, “in the absence of a downturn, a gradual tightening should start as inflation edges up and wage growth gains momentum.”

However, OECD also warned that the housing market is “a source of vulnerability”. So far, “data point to a soft landing without substantial consequence for the overall economy.” But “risk of a hard landing remains.” And it urged authorities to “prepare contingency plans for a severe collapse in the housing market. These should include the possibility of a crisis situation in one or more financial institutions.

On the data front

New Zealand manufacturing activity rose 2.0% qoq in Q3. Japan GDP was finalized at -0.6% qoq in Q3, revised down from -0.5% qoq. Current account surplus narrowed to JPY 1.33T. Australia home loans rose 2.2% mom in October, versus expectation of -0.5% mom.

For the day ahead, Swiss will release unemployment rate. German will release trade balance. UK will release trade balance, GDP and productions. Eurozone will release Sentix Investor Confidence. Later in the day, Canada will release housing starts and building permits.

Looking ahead

The week is very busy ahead. Brexit vote in the UK on Tuesday (supposedly) would be a key event risk. Also, Italy may finally resubmit its revised budget plan to EU. Besides Two central banks will meet. SNB should keep monetary policy unchanged without a doubt. And based on recent global market volatility, SNB should also reiterate the need to maintain negative interest rate, and stand ready for intervention if needed.

No change in ECB’s immediate plan is expected. That is, interest rates will be kept unchanged and ECB will stop asset purchase program after December. The main question is how ECB is viewing the current slow down in Eurozone growth. Would they maintain that Q3’s slow down was just temporary? Or would they change the tune. A dovish shift doesn’t necessarily change the forward guidance of keep interest rates at present levels at least “through the summer of 2019”. ECB has enough flexibility in the guidance. But more cautiousness would likely mean more pressure on Euro.

There are also enough economic data to keep trades and investors busy. Here are some highlights for the week:

- Monday: Japan GDP; Swiss unemployment; Eurozone Sentix investor confidence; Germany trade balance; UK GDP, productions, trade balance; Canada housing starts, building permits

- Tuesday: Japan BSI manufacturing; Australian house price, NAB business confidence; UK employment; German ZEW economic sentiment; US PPI

- Wednesday: Australia Westpac consumer sentiment; Japan PPI, machine orders, tertiary industry index; Eurozone industrial production; US CPI

- Thursday: US RICS house price balance; Australia inflation expectation; German CPI final; Swiss CPI, SNB rate decision; ECB rate decision; Canada new housing price index; US import prices, jobless claims

- Friday: New Zealand BusinessNZ manufacturing; Japan Tankan survey, PMI manufacturing; China fixed asset investment, industrial production, retail sales, unemployment rate; Eurozone PMIs; US retail sales, industrial production, PMIs, business inventories.

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2693; (P) 1.2749; (R1) 1.2787; More…

GBP/USD continues to stay in tight range above 1.2658 temporary low and intraday bias remains neutral first. On the downside, sustained break of 1.2661 key support will resume larger down trend from 1.4376. Next target will be 1.1946. On the upside, break of 1.2927 will extend the consolidation from 1.26661 with another rise. But even in case of strong rebound, upside should be limited by 1.3316 fibonacci level to bring down trend resumption eventually.

In the bigger picture, whole medium term rebound from 1.1946 (2016 low) should have completed at 1.4376 already, after rejection from 55 month EMA. The structure and momentum of the fall from 1.4376 argues that it’s resuming long term down trend. And this will be the preferred case as long as 38.2% retracement of 1.4376 to 1.2661 at 1.3316 holds. However, firm break of 1.3316 would bring stronger rebound to 61.8% retracement at 1.3721. And, the eventual depth of the fall from 1.4376, and the chance of hitting 1.1946 low, will depend on the strength of the interim corrective rebound from 1.2661.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Manufacturing Activity SA Q/Q Q3 | 2.00% | 1.80% | ||

| 23:50 | JPY | GDP Q/Q Q3 F | -0.60% | -0.50% | -0.30% | |

| 23:50 | JPY | GDP Deflator Y/Y Q3 F | -0.30% | -0.30% | -0.30% | |

| 23:50 | JPY | Current Account (JPY) Oct | 1.21T | 1.29T | 1.33T | |

| 0:30 | AUD | Home Loans M/M Oct | 2.20% | -0.50% | -1.00% | |

| 5:00 | JPY | Eco Watchers Survey Current Nov | 49.5 | 49.5 | ||

| 6:45 | CHF | Unemployment Rate Nov | 2.50% | 2.50% | ||

| 7:00 | EUR | German Trade Balance Oct | 17.2B | 17.6B | ||

| 9:30 | GBP | Visible Trade Balance (GBP) Oct | -10.5B | -9.7B | ||

| 9:30 | GBP | Industrial Production M/M Oct | 0.10% | 0.00% | ||

| 9:30 | GBP | Industrial Production Y/Y Oct | -0.20% | 0.00% | ||

| 9:30 | GBP | Manufacturing Production M/M Oct | 0.00% | 0.20% | ||

| 9:30 | GBP | Manufacturing Production Y/Y Oct | 0.00% | 0.50% | ||

| 9:30 | GBP | Construction Output M/M Oct | -0.40% | 1.70% | ||

| 9:30 | GBP | GDP M/M Oct | 0.10% | 0.00% | ||

| 9:30 | GBP | Index of Services 3M/3M Oct | 0.30% | 0.40% | ||

| 9:30 | EUR | Eurozone Sentix Investor Confidence Dec | 8.4 | 8.8 | ||

| 13:15 | CAD | Housing Starts Nov | 198K | 206K | ||

| 13:30 | CAD | Building Permits M/M Oct | -0.20% | 0.40% |

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals