The financial markets are slightly firmer today but lacks conviction. All eyes are on the results of US-China negotiations in Washington. There were rumors that the teams are drafting MOUs, and China pledged to increase agricultural purchases. But no details were leaked regarding the real core issues, in particular on enforcement of the agreement. Trump is set to meet Chinese Vice Premier Liu He again today. And we’ll see if they’ll release something of substance.

Meanwhile, for today, New Zealand Dollar is the weakest one so far. RBNZ is proposing to raise capital requirements for top banks. But markets are concerned that eventually, tighter financial conditions will force the central bank to cut interest rates. Yen is the second weakest on mild risk appetites. Canadian Dollar is the third weakest as rally in oil prices lost momentum. Canadian retail sales will be a test for Loonie’s resilience.

On the other hand, Australian Dollar is the strongest one for today. But it’s just paring some of this week’s steep losses. Officials are trying to talk down the significance of China Dalian port’s ban of Australian coal imports. Euro is the second strongest. German Q4 GDP confirmed to have grown 0% qoq, narrowly avoiding a technical recession in H2 of last year. Swiss Franc is so far the third strongest.

Technically, USD/CAD’s recovery and break of 1.3225 minor resistance now turns focus back to 1.3340 resistance. AUD/USD will be looking at 0.7054 key support in next fall. Against Europeans, Dollar is mildly tin favor to extend this week’s pull back. But EUR/USD and GBP/USD have to break 1.1371 and 1.3109 temporary tops first.

In Asia, Nikkei closed down -0.18%. Hong Kong HSI is up 0.17%. China Shanghai SSE is up 1.62%. Singapore Strait Times is down -0.26%. Japan 10-year JGB yield is up 0.0018 at -0.038. Overnight, DOW dropped -0.40%. S&P 500 dropped -0.35%. NASDAQ dropped -0.39%. 10-year yield rose 0.034 to 2.688.

RBNZ to raise top banks’ capital requirement, might cut interest rate

New Zealand Dollar drops broadly today after RBNZ proposed to raise capital requirement for top banks of the country. Capital ratios would be increased to 16% of frisk-weighted assets. Combined the top four banks might need to raise NZD 20B over the next five years to meet the rule.

RBNZ Deputy Governor Geoff Bascand said the move would only lead to a “marginal tightening of monetary conditions”. But he added that the central could consider to loosen up monetary further is needed. Bascand said “when we set the OCR (Official Cash Rate), we set it with for a 18 month to 2 year look ahead. So let’s say we are making a decision in the third quarter of this year…we just have to feed that into our regular monetary policy decision making”. And, “if we were worried, and thinking we were undershooting inflation, undershooting maximum sustainable employment, then we would obviously look for an OCR change…that is the implication.”

RBA Lowe: What’s of concern is accumulation of downside risks

RBA Governor Philip Lowe said today that the central scenario for 2019 is for growth of around 3%, inflation of around 2%and unemployment of around 5. And “this is not a bad set of numbers”. However, what is more of concern is the “accumulation of downside risks”.

The first major area of risks globally is “political risks” including US-China trade and technology tensions, Brexit, rise of populism and strains in some wester European countries. Second area of international risk is China slowdown. Domestically, RBA board has recently been paying “particularly close attention” to household spending and housing market. Lowe noted that ” underlying trend in consumption is softer than it earlier looked to be”. Decline housing prices could also affect overall spending.

On monetary policy, Lowe reiterated that “the probability that the next move is up and the probability that it is down are more evenly balanced than they were six months ago.”

AU FM Cormann: Dalian coal ban unrelated to bilateral relationship between Australia and China

Australian Dollar tumbles broadly yesterday on news that China’s Dalian port banned the countries’ coal import. But Australian offices are quick to talk down the implication. Mathias Cormann, Minister for Finance, said “when decisions like this have been made in the past at local port level, it was related to domestic supply related issues, environmental issues at a local level”. Cormann emphasized “it was unrelated with anything to do with the bilateral relationship between Australia and China.”

RBA Governor Philip Low said “I wouldn’t jump yet to the conclusion that this is something directed to Australia”. And, “It may well turn out to be that it’s being driven by concerns about the environment in China and the profitability of the coking coal industry in China.”

UK Barclay, Cox to meet EU Barnier again next week

There appears to be no breakthrough on Brexit for now. Brexit Minister Stephen Barclay and Attorney General Geoffrey Cox met EU chief Brexit negotiator Michel Barnier yesterday. They had “productive meeting” and discussed the “positions of both ides”. And it’s agreed that “talks should now continue urgently at a technical level”. Cox will explore “legal options” with the commission’s team. The trio will discuss again next week.

UK is seeking legal binding assurance that the Irish border backstop would be temporary if triggered. It’s believed that once this issue is solved, especially with the endorsement of Cox, the Brexit deal would get through the Commons. However, European Commission President Jean-Claude Juncker was “not very optimistic”. He noted that “in the British parliament every time they are voting, there is a majority against something, there is no majority in favor of something.”

On the data front

Japan national CPI core rose to 0.8% yoy in January, up from 0.7% yoy and matched expectations. But that’s still way off BoJ’s 2% target. Germany will release GDP final, Ifo business claims today. Eurozone will also release CPI final. Canada retail sales will be the main focus later in the day.

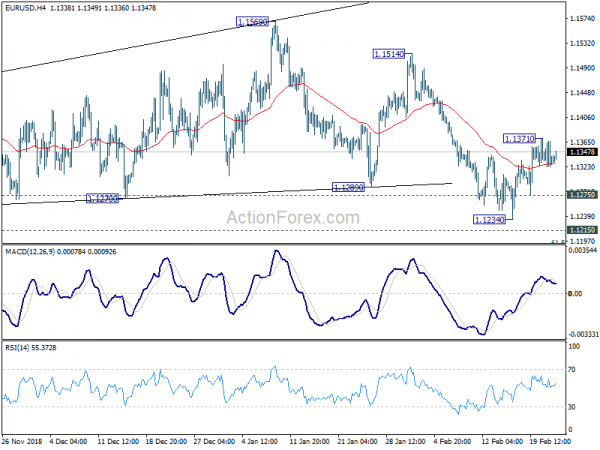

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1313; (P) 1.1341; (R1) 1.1361; More…..

EUR/USD is staying in tight range below 1.1371 and intraday bias remains neutral. Further rise is mildly in favor with 1.1275 minor support intact. Rebound fro 1.1234 is seen as another leg in consolidation pattern from 1.1215. On the upside, above 1.1371 will extend the rebound from 1.1234, towards 1.1514 resistance. On the downside, though, break of 1.1275 minor support will turn bias back to the downside for 1.1215 low instead. Decisive break there will confirm completion of consolidation from 1.1215, and resumption of down trend from 1.2555.

In the bigger picture, as long as 1.1814 resistance holds, down trend down trend from 1.2555 medium term top is still in progress and should target 61.8% retracement of 1.0339 (2017 low) to 1.2555 at 1.1186 next. Sustained break there will pave the way to retest 1.0339. However, break of 1.1814 will confirm completion of such down trend and turn medium term outlook bullish.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | National CPI Core Y/Y Jan | 0.80% | 0.80% | 0.70% | |

| 07:00 | EUR | German GDP Q/Q Q4 F | 0.00% | 0.00% | 0.00% | |

| 09:00 | EUR | German IFO Business Climate Feb | 98.9 | 99.1 | ||

| 09:00 | EUR | German IFO Expectations Feb | 94.2 | 94.2 | ||

| 09:00 | EUR | German IFO Current Assessment Feb | 103.9 | 104.3 | ||

| 10:00 | EUR | Eurozone CPI Core Y/Y Jan F | 1.10% | 1.10% | ||

| 10:00 | EUR | Eurozone CPI M/M Jan | -1.10% | 0.00% | ||

| 10:00 | EUR | Eurozone CPI Y/Y Jan F | 1.40% | 1.60% | ||

| 13:30 | CAD | Retail Sales M/M Dec | -0.30% | -0.90% | ||

| 13:30 | CAD | Retail Sales Ex Auto M/M Dec | -0.30% | -0.60% |

For traders: our Portfolio of forex robots for automated trading has low risk and stable profit. You can try to test results of our download forex ea

Signal2forex review

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals