Market sentiments generally stabilized today after initial selloff in Asia. While major European indices are still in red, losses are so far very limited. German 10-year bund yield even managed to turn positive briefly. Better than expected German Ifo Business Climate gave sentiment a mild lift. Yet, the picture isn’t cleared as manufacturing sector remained weak. With an empty economic calendar in North America, focus will turn to Brexit debate in the Commons.

UK Prime Minister Theresa May just completed her Cabinet meeting without any comments to the press. The discussions there were reported to be positive but inconclusive. It’s now uncertain whether indicative vote on Brexit will be tabled today, or will be pushed after another meaningful vote on Tuesday. Meanwhile, there seems to be a tacit understanding that for some Brexiteers, May’s future is linked to the MV3.

In the currency markets, Yen and Canadian Dollar are currently the weakest ones, followed by Dollar. Sterling recovered some ground but remains clueless. Australian and New Zealand Dollar are the strongest ones. In Europe, FTSE is down -0.65%. DAX is down -0.04%. CAC is down -0.12%. German 10-year bund yield is up 0.0034 at -0.008. Earlier in Asia, Nikkei dropped -3.01%. Hong Kong HSI dropped -2.03%. China Shanghai SSE dropped -1.97%. Singapore Strait Times dropped -0.91%. Japan 10-year JGB yield dropped -0.119 to -0.085.

EU completes April 12 no-deal Brexit preparation

In a statement released today, EU said it completes the preparations for no-deal Brexit on April 12. It also noted that it is “increasingly likely” that UK will leave EU without a deal. EU also urged all EU citizens and businesses to continue informing themselves about the consequences of a possible “no-deal” scenario and to complete their no-deal preparedness.

EU’s no-deal contingency measures cover PEACE programme, EU budget, fishing rights and compensation, financial services, air connectivity and safety, road connectivity, rail connectivity, ship inspects, re-alignment of the North Sea – Mediterranean core network corridor, climate policy, Erasmus+ programme, social security entitlements and Visa reciprocity.

EU explained again that in a no-deal scenario, UK will “become a third country” without any transitionary arrangements. And this week “cause significant disruption for citizens and businesses”. In such case, relations between UK and EU will be government by general international public law, including rules of the World Trade Organization. Tariffs will immediately apply at the borders. And these controls could sauce significant delays at the border.

German Ifo rose to 99.6, resilient economy except manufacturing

Germany Ifo Business Climate improved to 99.6 in March, up from 98.7 and beat expectation of 98.5. That’s also the first increase following six declines in a row. Current Assessment rose 0.2 to 103.8, beat expectation of 102.9. Expectations gauge also rose to 95.6, versus consensus of 94.0.

Looking at the details, manufacturing dropped from 9.1 to 6.6, seventh decline in a row. But services rose from 21.3 to 26.0. Trade rose from 4.9 to 8.2. Construction rose from 18.0 to 20.3.

Ifo President Clemens Fuest noted “sentiment among German business leaders has improved somewhat”. And “companies are somewhat more satisfied with their current business situation, and they are decidedly more optimistic regarding business in the coming six months.” He added “the German economy is showing resilience.”

Ifo economist Klaus Wohlrabe said, “Brexit uncertainty is particularly hitting the industrial sector. The other sectors don’t appear to be affected” .

Fed Harker: Risks tilt very slightly to the downside, at most one hike this year

Philadelphia Fed President Patrick Harker said in a speech in London that “potential risks tilt very slightly to the downside” in the US. Though he emphasized the work “slight” as he saw “outlook as positive” and economy “continues to grow” and is on pace to the the longest economic expansion in history.

Harker added there was “continued strength” in the labor market. He’d “cautious against” getting caught up in a single data point in February’s dismal job data. Meanwhile, inflation is running around 2% target and “does not appear to be on a strong upward trajectory”. Rather inflation is “edging slightly downward”.

Combining all, Harker stays in “wait-and-see mode”. He expects “at most, on rate hike this year, and one in 2020”. But his stance will be “guided by data”.

Fed Evans: May need to loosen monetary policy if activity softens more than expected

Chicago Fed President Charles Evans said he now doesn’t expect a rate hike until second half of next year. Also he warned that “at the moment, the risks from the downside scenarios loom larger than those from the upside ones”. And, “if activity softens more than expected or if inflation and inflation expectations run too low, then policy may have to be left on hold — or perhaps even loosened — to provide the appropriate accommodation to obtain our objectives.”

On the other hand, “if growth runs close to its potential and inflation builds momentum, then some further rate increases may be appropriate over time to ensure that the economy settles in on its long-run sustainable growth path and that inflation runs symmetrically about our 2 percent target”. He added “in this scenario, the path for rates will depend crucially on any signals of an acceleration in core inflation.”

Though, he emphasized that US economy is still in good shape. He pointed to Fed’s forecasts of 1.75-2.0% GDP growth in 2019. Evans said “the lower end of this range is actually in line with my view of the economy’s long-run growth potential. So we’re not looking at a bad number.” Though, “:the economy won’t feel like it is doing very well compared with last year’s very strong performance.”

Former Fed chair Yellen: Yield curve inversion signals Fed cut, not recession

Former Fed Chair Janet Yellen said in a conference in Hong Kong that yield curve inversion doesn’t indicate recession in the US economy ahead. Rather, the development suggests that Fed might need to cut interest rate.

Simply, put she said “my own answer is no, I don’t see it as a signal of recession”. She explained, “in contrast to times past, there’s a tendency now for the yield curve to be very flat”. Thus, it’s now easier for it to invert.

On the other hand, Yellen said “it might signal that the Fed would at some point need to cut rates, but it certainly doesn’t signal that this is a set of developments that would necessarily cause a recession.”

BoJ Harada: Unemployment rate won’t be below 2.5% without QQE

BoJ board member Yutaka Harada hailed that the quantitative and qualitative easing (QQE) program boosted productivity and drove down unemployment rate. He said in a speech that “the biggest contribution QQE has made to Japan’s economy was to boost its productivity.” Also, “without QQE, Japan’s jobless rate would not have fallen below 2.5 percent”.

Harada is a persistent dissent in BoJ’s monetary policy decisions. He complained regularly that allowing the long-term yields to move upward and downward to some extent was too ambiguous as the guideline for market operations. Also, he urged to introduce forward guidance that would further clarify its relationship with the price stability target.

Released from Japan, all industry activity index dropped -0.2% mom in January, versus expectation of -0.4% mom.

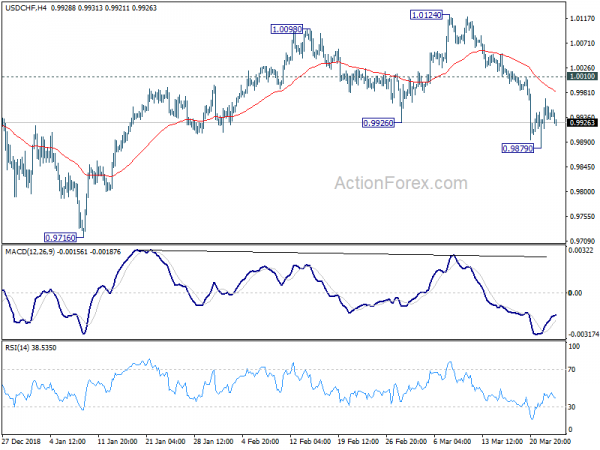

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9909; (P) 0.9940; (R1) 0.9966; More…..

USD/CHF is staying in consolidation above 0.9879 temporary low. Intraday bias remains neutral first. Further decline remains in favor with 1.0010 minor resistance intact. On the downside, below 0.9879 will resume the fall from 1.0124 to 0.9716 key support. Nevertheless, break of 1.0010 will turn bias back to the upside for 1.0124/28 resistance zone.

In the bigger picture, focus is back on medium term trend line (now at 0.9846). Decisive break there will argue that whole rise from 0.9186 has completed. Further break of 0.9716 will confirm reversal and target next support level at 0.9541. Nevertheless, there is still a chance that price action from 1.0128 are forming a consolidative pattern with fall from 1.0124 as third leg. If this is the case, stronger support should be seen between 0.9716 and the trend line to contain downside.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 4:30 | JPY | All Industry Activity Index M/M Jan | -0.20% | -0.40% | -0.40% | |

| 9:00 | EUR | German IFO Business Climate Mar | 99.6 | 98.5 | 98.5 | 98.7 |

| 9:00 | EUR | German IFO Current Assessment Mar | 103.8 | 102.9 | 103.4 | 103.6 |

| 9:00 | EUR | German IFO Expectations Mar | 95.6 | 94 | 93.8 |

Signal2forex review

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals