Indicative votes on Brexit alternatives in the UK House of Commons will catch most attention ahead. Debate is due to start by 1500GMT. We’ll see what alternative Brexit path could gain majority in the Parliament. House of Commons Speaker John Bercow will select which of the proposals will be put to a vote. The options now include “respect the referendum result”, “customs union”, “confirmatory public vote”, “revocation to avoid no deal” and “no deal”.

Ahead of that, Sterling is trading as the strongest one for today so far. But it should be emphasized that Pound is stuck in recently established range against Dollar, Euro and Yen. There is no sign of breakout and current rise is nothing more than part of consolidations. Yen is following as the second strongest with help from weakness in global treasury yields. In particular, US 10-year yield is extending recent decline to as low as 2.379 so far, losing 2.4% handle. Yield curve inversion is just getting worse and worse.

Meanwhile, New Zealand and Australian Dollar remain the weakest ones undoubtedly. NZD is sold off sharply after RBNZ indicated that next move is a cut. AUD follows as RBNZ’s dovish shift somewhat solidifies that case for RBA cuts too.

In other markets, US stocks open mildly higher with DOW, S&P 500 and NASDAQ trading up around 0.2%. In Europe, FTSE is up 0.17%. DAX is up 0.62%. CAC is up 0.58%. German 10-year yield is down -0.0546 at -0.068. Earlier in Asia: Nikkei dropped -0.23%. Hong Kong HSI rose 0.56%. China Shanghai SSE rose 0.85%, back above 3000 handle. Singapore Strait Times dropped -0.06%. Japan 10-year JGB yield dropped -0.0018 at -0.067.

EU Tusk: Cannot betray increasing majority of British people who want to stay in EU

European Commission President Jean-Claude Juncker and European Council President Donald Tusk talked Brexit to the European Parliament day.

Tusk said the voices of British people whole wanted to stay in the EU shouldn’t be ignored. And he urged the Parliament to be open to a longer Article 50 extension. He said, “I said that we should be open to a long extension if the UK wishes to rethink its Brexit strategy, which would of course mean the UK’s participation in the European parliament elections. And then there were voices saying that this would be harmful or inconvenient to some of you…. Let me be clear: such thinking is unacceptable. You cannot betray the 6 million people who signed the petition to revoke article 50, the 1 million people who marched for a people’s vote, or the increasing majority of people who want to remain in the European Union.”

Juncker said it’s unclear how Brexit would unfold. And, “I told some of you that if you compare Great Britain to a sphinx then the sphinx would seem to me an open book. We will see in the course of this week how this book will speak,”

Also, chief Brexit negotiator told lawmakers: “In all scenarios, the Good Friday agreement will continue to apply. The United Kingdom will remain a core guarantor of that agreement and is expected to uphold it in spirit and in letter:” And, “the Commission is ready to make additional resources available to Ireland, technical and financial to address any additional challenges.”

UK retail sales volume dropped most in 17 months as Brexit uncertainty escalates

UK CBI Reported Sales dropped sharply to -18 in March, down from 0 and missed expectation of 5. That is, 28% of respondents reported that sales volumes were up on a year ago in March, while 46% said they were down, giving a balance of -18%. It’s the fastest contraction in 17 months, marked four-month run in which sales have not grown.

Anna Leach, CBI head of economic intelligence, said: “Even accounting for Easter timing, the High Street’s poor run continues. While real wage growth is picking up, consumer confidence has been hit by escalating uncertainty over Brexit and concern over the economy’s future. The pain currently being felt on the High Street is yet another reason why it is so vitally important politicians agree a deal in Parliament that is acceptable to the EU and protects our economy. No-deal must be averted at all costs.”

ECB Draghi: Intra- and extra- Eurozone trade growth recoupled downward for the first time since GFC

ECB President Mario Draghi said in a speech that it’s “not yet certain” whether Eurozone is experience a “more lasting deterioration in the growth outlook” right now. The loss of momentum has been “predominantly driven by pervasive uncertainty in the global economy”. Domestic economy has “remained relatively resilient” and expansion drivers “remain in place”. But risks remained “tilted to the downside”.

Draghi pointed to continuing weakness in wold trade which has “significantly affected the manufacturing sector” and Eurozone is now “seeing a more persistent deterioration of external demand”. Intra-euro area trade also slowed steeply last year. And, “recoupling of intra- and extra-euro area trade growth in a downward direction has not occurred since the start of the global financial crisis”. For now, “current data suggest that external demand has not yet spilled over significantly into domestic demand”. But ” risks have risen in the last months and uncertainty remains high”.

Draghi also reiterated that “substantial accommodation is still needed”. At last meeting, ECB decided to extend the date-based leg of the rate guidance “at least through the end of 2019”. That ECB will continue too the “very sizeable stocks of assets” bought under the asset purchase program for even longer. Also, Draghi added that “we would ensure that monetary policy continues to accompany the economy by adjusting our rate forward guidance to reflect the new inflation outlook.” It suggests ECB is ready to extend delay a rate hike further when necessary.

ECB de Guindos: Eurozone slowdown raises financial stability risks

Vice President Luis de Guindos warned that weak Eurozone growth is raising financial stability risks due to weakening bank profits and rising concern over sovereign debt sustainability.

De Guindos said in a conference in Frankfurt that “in an environment where cyclical factors may exert further downward pressure on bank profitability, banks would need to step up their efforts to overcome structural challenges”.

Also, “such measures may include cost reductions – including lower staffing costs and streamlining of branch networks, enhanced digitalization – implying initial, one-off large-scale investments, revenue diversification and the reduction of the stock of non-performing loans in the six countries where levels are still high.”

NZD dives as RBNZ turns dovish, next move is rate cut

New Zealand Dollar dives sharply after RBNZ kept OCR unchanged at 1.75% and shifted to a clear dovish stance. It now expected that “the more likely direction of our next OCR move is down”.

In the statement, it also noted that balance of risks to the outlook has “shifted to the downside”. At the same time, risk of a “more pronounced global downturn has increased”, and ‘low business sentiment continues to weigh on domestic spending.” Though, on the upside, “inflation could rise faster if firms pass on cost increases to prices to a greater extent.”

Markets are raising bets of an RBNZ rate cut this year. A cut it full priced in for November and there speculations that it might happen as soon as in May.

More in

China industrial profits dropped -14%. Autos, oil processing, steel and chemicals dragged

China’s industrial profits in January-February period slumped -14.0% yoy to CNY 708B. It’s the biggest contraction since 2011. National Bureau of Statistics (NBS) said the contract was mainly due to distortions caused by the timing of Lunar New Year.

Meanwhile, there were notable declines in profits in auto, oil processing, steel and chemical industries. Ex-factory prices of Auto, oil processing, steel and chemicals dropped -0.4%, -1.3%, -2.5% and -2.3% respectively. Profits dropped CNY 37B, CNY 32B, CNY, 29B and CNY 19B respectively. Combined the contributed to -14.2% contraction in profits. Excluding them, industrial profits rose 0.2%.

While the set of data is largely ignored by the stock markets, it’s putting some more weight to the upcoming round of trade talks. US Trade Representative Robert Lighthizer and Treasury Secretary Steven Mnuchin will visit Beijing on March 28-29. Even though an eventual trade might might not help reverse the slowdown in China, at least, the drag on exports will likely be eased.

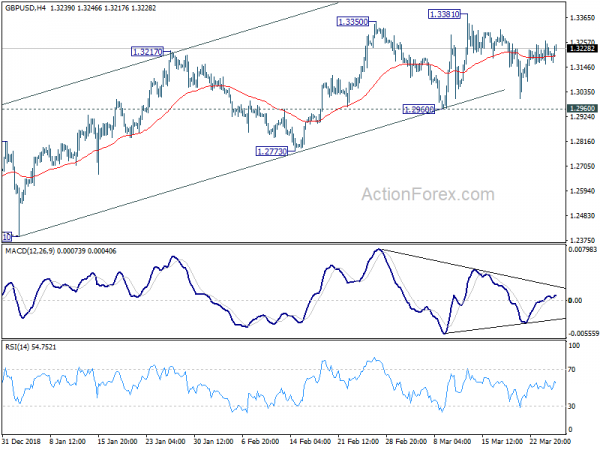

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3155; (P) 1.3209; (R1) 1.3259; More….

GBP/USD strengthens mildly but remains bounded in range of 1.2960.3381. Intraday bias remains neutral and more sideway trading could be seen. As long as 1.2960 support holds, further rally remains in favor. On the upside, firm break of 1.3381 will resume the rebound from 1.2391 to 61.8% retracement of 1.4376 to 1.2391 at 1.3618 next. However, on the downside, decisive break of 1.2960 will indicate that rebound from 1.2391 has completed earlier than expected. Deeper fall would then be seen to 1.2773 support for confirmation.

In the bigger picture, medium term decline from 1.4376 (2018 high) should have completed at 1.2391. Rise from 1.2391 is now seen as the third leg of the corrective pattern from 1.1946 (2016 low). Further rise could be seen through 1.4376 in medium term. On the downside, though, break of 1.2773 support will dampen this view. Focus will be turned back to 1.2391 low and break will resume the fall from 1.4376 to 1.1946.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:00 | NZD | RBNZ Official Cash Rate | 1.75% | 1.75% | 1.75% | |

| 11:00 | GBP | CBI Reported Sales Mar | -18 | 5 | 0 | |

| 12:30 | CAD | International Merchandise Trade (CAD) Jan | -4.2B | -2.3B | -4.6B | -4.8B |

| 12:30 | USD | Trade Balance (USD) Jan | -51.1B | -57.5B | -59.8B | -59.9B |

| 14:00 | USD | Current Account Balance (USD) Q4 | -130B | -125B | ||

| 14:30 | USD | Crude Oil Inventories | -9.6M |

Signal2forex review

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals