Dollar jumps broadly in early US session after very strong retail sales and jobless claims. Yen is the only one stronger than the greenback, thanks to pull back in global treasury yields. Euro, as well as benchmark German yield tumble as poor PMIs dent hope for a recovery in Q2. New Zealand Dollar is the only weaker one for today. Despite strong Canadian retail sales and Australian Employment, both are among the weakest ones. For the week, Yen is now the strongest one, followed by Dollar and then Aussie. Kiwi is the weakest one, followed by Swiss Franc and then Euro.

Technically, USD/CHF break of 1.0128 resistance now suggests resumption of medium term up trend from 0.9186 towards 1.0342 key resistance. EUR/USD’s break of 1.1250 minor support now put focus back to 1.1176 low. Break will resume medium term down trend from 1.2555. 111.69/112.13 range in USD/JPY will be watched as the pair will have to decide whether to break through or reverse. USD/CAD is range bound but break of 1.3467 is mildly in favor. AUD/USD will look at 0.7139 minor support to indicate completion of near term recovery.

In Europe, currently, FTSE is down -0.05%. DAX is up 0.32%. CAC Is up 0.24%. German 10-year yield is down -0.046 at 0.038, still way above 0%. Earlier in Asia, Nikkei dropped -0.54%. China Shanghai SSE dropped -0.40%. Hong Kong HSI dropped -0.54%. Singapore Strait Times dropped -0.03%. Japan 10-year JGB yield dropped -0.0179 to -0.026.

US initial jobless claims trending down again, retail sales also strong

Initial jobless claims dropped -5k to 192k in the week ending April 13, below expectation of 207k. It’s also the lowest since September 6, 1969 when it was 182k. Four week moving average of initial claims dropped -6k to 201.25k, lowest since November 1, 1969. And the series seem to be trending down again. Continuing claims dropped -64k to 1.653m. Four week moving average of continuing claims dropped 022.75k to 1.713m.

Headline retail sales rose 1.6% mom in March versus expectation of 0.8% mom. That’s also the strongest rise since September 2017. Meanwhile, 12 of 13 major retail categories increased. Ex-auto sales rose 1.2% mom versus expectation of 0.7% mom. Total sales from January through March rose 2.9% yoy.

Philadelphia Fed Manufacturing Business Outlook, however, dropped to 8.5, down from 13.7 and missed expectation of 11.0.

From Canada, retail sales rose 0.8% mom in February versus expectation of 0.4% mom. Ex-auto sales rose 0.6% mom versus expectation of 0.2%. Both figures are also strong.

Eurozone PMIs: Disappointing start to Q2, suggest under 0.2% GDP growth

Eurozone PMI manufacturing rose to 47.8, up from 47.5 but missed expectation of 48.1. PMI services dropped to 52.5, down from 53.3 and missed expectation of 53.1. PMI composite dropped to 51.3, down from 51.6, and hit a 3-month low. The surveys indicate that quarterly eurozone GDP growth has slowed to just under 0.2%.

Chris Williamson, Chief Business Economist at IHS Markit said: “The eurozone economy started the second quarter on a disappointing footing, with the flash PMI falling to one of the lowest levels seen since 2014. The data add to worries that the economy has failed to rebound with any conviction from one-off factors that dampened activity late last year, and continues to show only very modest growth in the face of headwinds from slower global demand growth and subdued economic sentiment.”

Germany PMI manufacturing rose to 44.5 in April, up from 44.1 but missed expectation of 45.2. It’s staying deep in contraction below 50. PMI services rose to 55.6, up from 55.4, beat expectation of 55.0. PMI composite rose to 52.1, up from 51.4.

France PMI manufacturing dropped to 49.6 in April, down from 49.7 and missed expectation of 50.0. That’s the lowest level in 32 months. PMI services, on the other hand, improved to 50.5, up from 49.1 and beat expectation of 49.8. PMI composite rose to 50.0, up from 48.9.

Also release in European session, UK retail sales include auto and fuel rose 1.1% mom, 6.7% yoy in March versus expectation of -0.4% mom, 4.6% yoy. Retail sales exclude auto and fuel rose 1.2% mom, 6.2% yoy in March versus expectation of -0.3% mom, 4.0% yoy. Germany PPI dropped -0.1% mom, rose 2.4% yoy in March. Swiss trade surplus widened to CHF 3.18B in March.

Australia employment rose 25.7k, no imminent need for RBA cut

Australia employment grew 25.7k in March, much better than expectation of 15.2k. Full time employment rose 48.3k while part time jobs dropped -22.6k. Unemployment rate rose from 4.9% to 5.0%, matched expectations. Participation rate also rose from 65.6% to 65.7%.

The largest increase in employment was in Queensland (up 10.4k), followed by Victoria (up 10.0k) and South Australia (up 8.5k). The largest decrease was in New South Wales (down 2.6k) followed by Tasmania (down 1.8k). The seasonally adjusted unemployment rate increased in Queensland (up 0.7 pts to 6.1%), South Australia (up 0.2 pts to 5.9%), Tasmania (up 0.2 pts to 6.7%), Western Australia (up 0.1 pts to 6.0%) and New South Wales (up 0.1 pts to 4.3%). The only decrease in the unemployment rate was observed in Victoria (down 0.1 pts to 4.6%).

The strong gain in full time jobs underlines the robustness in the employment market. However, unemployment rate rose in all regions, only except Victoria, which is a concern. At this point, there is no imminent push for an RBA rate cut in the first up. But situation could worsen ahead that trigger the expected two cuts in the second half. The key will lie in upcoming economic projections in May.

Australia NAB business conditions continued broad based easing

Australia NAB Business Confidence dropped to -1 in Q1, down from 1. Current Business Conditions dropped to 4, down from 9. Business Conditions for the next two months dropped slightly to 22, down from 25. Capex plans dropped to 22, down from 25.

Alan Oster, NAB Group Chief Economist noted that easing of business conditions continued through 2018 into 2019. And they’re only “just above average”. Together with “negative conditions and forwards orders”, they suggest outlook “remains weak”. And the easing in conditions has been “broad based across most industries and all states”, in particular retail.

Oster also said: “For now, we will wait and see how leading indicators of the labour market evolve, though we think it is likely the RBA will act to cut the cash rate and bolster the economy should the labour market deteriorate on the back of weaker activity data”.

Japan PMI manufacturing improved to 49.5, remained stuck in its rut

Japan PMI manufacturing rose to 49.5 in April, up from 49.2 and beat expectation of 49.4. Nevertheless, it’s still the third straight month of sub-50 reading. Markit pointed out that weaker demand from domestic and international markets persists, leading output to fall further. But manufacturing employment remains resilient.

Joe Hayes, Economist at IHS Markit said: “Japan’s manufacturing sector remained stuck in its rut at the start of Q2, with the factors which have prohibited any growth such as US-Sino relations, growth fears in China and the turn in the global trade cycle, all remaining prominent risks. Export orders dipped at a stronger rate in April, domestic demand for goods was similarly weak and firms cut their stocks and scaled back production. Yet again, the service sector will need to pick up any slack to help keep Japan’s economy afloat.”

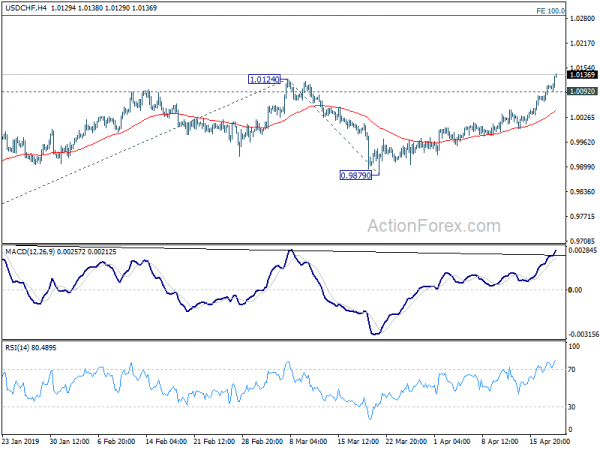

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 1.0076; (P) 1.0094; (R1) 1.0124; More…

USD/CHF’s rally accelerates to as high as 1.0137 so far. Break of 1.0128 resistance confirms larger up trend resumption. Intraday bias stays on the upside for 100% projection of 0.9716 to 1.0124 from 0.9879 at 1.0287 next. On the downside, below 1.0092 minor support will turn intraday bias neutral and bring consolidations, before staging another rise.

In the bigger picture, medium term up trend from 0.9186 is resuming. Current rise should now target 1.0342 resistance next. For now, we’d be cautious on strong resistance from there to limit upside, until we see medium term upside acceleration. On the downside, break of 0.9879 support is needed to indicate reversal. Otherwise, outlook will stay bullish in case of deep pull back.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:30 | AUD | NAB Business Confidence Q1 | -1 | 1 | ||

| 01:30 | AUD | Employment Change Mar | 25.7K | 15.2K | 4.6K | |

| 01:30 | AUD | Unemployment Rate Mar | 5.00% | 5.00% | 4.90% | |

| 06:00 | EUR | German PPI M/M Mar | -0.10% | 0.20% | -0.10% | |

| 06:00 | EUR | German PPI Y/Y Mar | 2.40% | 2.70% | 2.60% | |

| 06:00 | CHF | Trade Balance (CHF) Mar | 3.18B | 2.87B | 3.13B | 2.94B |

| 07:15 | EUR | France Manufacturing PMI Apr P | 49.6 | 50 | 49.7 | |

| 07:15 | EUR | France Services PMI Apr P | 50.5 | 49.8 | 49.1 | |

| 07:30 | EUR | Germany Manufacturing PMI Apr P | 44.5 | 45.2 | 44.1 | |

| 07:30 | EUR | Germany Services PMI Apr P | 55.6 | 55 | 55.4 | |

| 08:00 | EUR | Eurozone Manufacturing PMI Apr P | 47.8 | 48.1 | 47.5 | |

| 08:00 | EUR | Eurozone Services PMI Apr P | 52.5 | 53.1 | 53.3 | |

| 08:30 | GBP | Retail Sales Inc Auto Fuel M/M Mar | 1.10% | -0.40% | 0.40% | 0.60% |

| 08:30 | GBP | Retail Sales Inc Auto Fuel Y/Y Mar | 6.70% | 4.60% | 4.00% | |

| 08:30 | GBP | Retail Sales Ex Auto Fuel M/M Mar | 1.20% | -0.30% | 0.20% | 0.40% |

| 08:30 | GBP | Retail Sales Ex Auto Fuel Y/Y Mar | 6.20% | 4.00% | 3.80% | |

| 12:30 | CAD | Retail Sales M/M Feb | 0.80% | 0.40% | -0.30% | -0.40% |

| 12:30 | CAD | Retail Sales Ex Auto M/M Feb | 0.60% | 0.20% | 0.10% | -0.60% |

| 12:30 | USD | Retail Sales Advance M/M Mar | 1.60% | 0.80% | -0.20% | |

| 12:30 | USD | Retail Sales Ex Auto M/M Mar | 1.20% | 0.70% | -0.40% | |

| 12:30 | USD | Philadelphia Fed Business Outlook Apr | 8.5 | 11 | 13.7 | |

| 12:30 | USD | Initial Jobless Claims (APR 13) | 192K | 207K | 196K | 197K |

| 13:45 | USD | US Manufacturing PMI Apr P | 53 | 52.4 | ||

| 13:45 | USD | US Services PMI Apr P | 55 | 55.3 | ||

| 14:00 | USD | Leading Index Mar | 0.40% | 0.20% | ||

| 14:00 | USD | Business Inventories Feb | 0.30% | 0.80% | ||

| 14:30 | USD | Natural Gas Storage | 25B |

Signal2forex review

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals