Euro recovers mildly today as partly supported by strong rebound in German economic sentiment. Though, upside is capped for now as outlook for the country remains negative. Follows as the second strongest, then Yen. Fed is still widely expected to cut interest rate again tomorrow. And the question is whether Chair Jerome Powell would signal that’s the end of the mid-cycle adjustment. On the other hand, Australian Dollar remains the weakest one on dovish RBA minutes. New Zealand Dollar is the second weakest, then Swiss Franc.

Technically, EUR/USD continues to engage in sideway consolidation. A break through 1.0926 is still expected but it might come at a later stage. USD/CHF’s break of 0.9946 suggests resumption recent choppy rise from 0.9659. 0.9975 will be an important structural resistance to take out. For now, AUD/USD is still holding above 0.6807 minor support, but break there will indicate completion corrective rebound from 0.6677.

In Europe, currently, FTSE is flat. DAX is down -0.56%. CAC is down -0.23%. German 10-year yield is down -0.006 at -0.485. Earlier in Asia, Nikkei rose 0.06%. Hong Kong HSI dropped -1.23%. China Shanghai SSE dropped -1.75%. Singapore Strait Times dropped -0.65%. Japan 10-year JGB yield rose 0.0043 to -0.151.

Lagarde approved by European Parliament as next ECB President

European Parliament approved appointment of IMF managing director Christine Lagarde as next ECB president. The motion was voted for by 394 to 206, with 49 abstentions. Lagarde should take over the job from Mario Draghi from November 1. Luxemburger Yves Mersch was also voted by the parliament to become the next Vice President of the supervision arm, by 379 to 230 votes, with 69 abstentions.

German ZEW economic sentiment jumped to -22.5, but outlook remains negative

German ZEW Economic Sentiment rose to -22.5 in September, up from -44.1 and beat expectation of -38. But it’s still well below long-term average of 21.5. Current Situation index dropped to -19.9, down from -13.5 and missed expectation of -15.0. Eurozone ZEW Economic Sentiment rose to -22.4, up from -43.6, beat expectation of -37.4. Eurozone Current Situation index dropped -1.1 to -15.6.

“The rise of the ZEW Indicator of Economic Sentiment is by no means an all-clear concerning the development of the German economy in the next six months. The outlook remains negative. However, the rather strong fears that financial experts had in the previous month regarding a further intensification of the trade conflict between the USA and China did not come true. And there is still hope that a no deal Brexit can be avoided. In addition, the European Central Bank is attempting to reduce the economic risks in the eurozone by further easing its monetary policy,” comments ZEW President Professor Achim Wambach.

SECO downgrades 2019 Swiss GDP growth forecast to 0.8%

Swiss State Secretariat for Economic Affairs downgraded 2019 growth forecasts and warned that the outlook has become “gloomier”. And in the coming years, “Swiss economy is set to brighten only gradually.” GDP growth is projected to be at 0.8% for 2019, way below June forecasts of 1.2%. For 2020, though, GDP growth forecast was kept unchanged at 1.7%.

Exports growth will be below-average in 2019 “as signs of a weak second half of 2019 for important trade partner Germany are increasing, among other factors.” Domestic outlook has come gloomier too as “companies are set to invest only hesitantly in equipment in the near future”. Consumer is expected to continue moderate growth.

Globally, downside risks “clearly predominate”, with new US-China tariffs, Brexit and fragile situation in some emerging economies like Argentina. “Upward pressure on the Swiss franc could also increase if further risks with considerable implications materialize, with corresponding dampening effects on the export economy. ”

RBA minutes suggest easing bias, affirm more rate cut

In the minutes of September meeting, RBA maintained easing bias with some dovishness between paragraphs. The minutes overall are inline with market expectations of further rate cut ahead, probably in October. It’s noted that “members would assess developments in both the international and domestic economies, including labour market conditions, and would ease monetary policy further if needed to support sustainable growth in the economy and the achievement of the inflation target over time.”

On international developments, RBA said “risks to the global growth outlook were to the downside”. US-China trade disputes had “escalated” while China’s growth “had continued to slow”. These developments were “affecting trade and investment decisions in overseas economies”. And, “against this backdrop and with ongoing low inflation, a number of central banks had reduced interest rates over recent months and further monetary easing was widely expected.”

Domestically, employment growth continued to be strong but “unemployment rate had remained steady at around 5.2 per cent”. Wages growth had “remained slow” with few indications of building pressures. Also, RBA repeated that the economy “could sustain lower rates of unemployment and underemployment.” Q2 Growth was expected to have been around 0.5%. “Private final demand, which includes consumption, business investment and dwelling investment, was expected to have been weak.”

Also released, Australia house price index dropped -0.7% qoq in Q2, better than expectation of -1.1% qoq. New Zealand Westpac consumer confidence dropped from 103.5 to 103.1 in Q3.

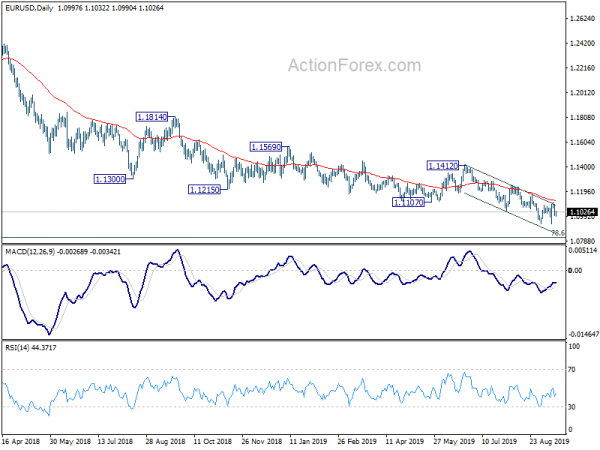

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0970; (P) 1.1028; (R1) 1.1062; More…

EUR/USD recovers mildly but stays in consolidation from 1.0926. Intraday bias remains neutral and more sideway trading might be seen. But overall, outlook remains bearish as long as 1.1164 resistance holds. Firm of 1.0926 will resume lager down trend from 1.2555 for 1.0813 fibonacci level next. However, firm break of 1.1164 will be an early indication of larger reversal and target 1.1249 resistance.

In the bigger picture, down trend from 1.2555 (2018 high) is in progress. Prior rejection of 55 week EMA also maintained bearishness. Further fall should be seen to 78.6% retracement of 1.0339 to 1.2555 at 1.0813. Decisive break there will target 1.0339 (2017 low). On the upside, break of 1.1412 resistance is needed to indicate medium term bottoming. Otherwise, outlook will stay bearish in case of rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:00 | NZD | Westpac Consumer Confidence Q3 | 103.1 | 103.5 | ||

| 01:30 | AUD | House Price Index Q/Q Q2 | -0.70% | -1.10% | -3.00% | |

| 01:30 | AUD | RBA Minutes Sep | ||||

| 09:00 | EUR | German ZEW Economic Sentiment Sep | -22.5 | -38 | -44.1 | |

| 09:00 | EUR | German ZEW Current Situation Sep | -19.9 | -15 | -13.5 | |

| 09:00 | EUR | Eurozone ZEW Economic Sentiment Sep | -22.4 | -37.4 | -43.6 | |

| 12:30 | CAD | Manufacturing Sales M/M Jul | -1.30% | -1.20% | -1.40% | |

| 13:15 | USD | Industrial Production M/M Aug | 0.20% | -0.20% | ||

| 13:15 | USD | Capacity Utilization Aug | 77.60% | 77.50% | ||

| 14:00 | USD | NAHB Housing Market Index Sep | 66 | 66 |

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals