Executive Summary

After a decade without a rate cut, the Federal Reserve Open Market Committee (FOMC) has now cut the fed funds rate in back-to-back meetings. Will the October 29 & 30 meeting make it threein- a-row? Last week alone, twelve different Fed officials weighed in on policy at different events from London (Bullard) to Los Angeles (Daly). We have now entered the blackout period, the leadup to the FOMC meeting during which Fed officials refrain from commenting on monetary policy.

This meeting really comes down to two options with respect to rates: cut or no cut? Though it is a close call, we suspect the most likely outcome for next week’s meeting is that the FOMC will cut the fed funds rate another 25 bps, while continuing to emphasize risks to the outlook from global growth and trade policy and acknowledging that inflation remains below target. In the event of a cut in October, a fourth rate cut in December would likely not be needed.

On the balance sheet side, the unexpected announcement from the Fed on October 11 that it will begin growing its balance sheet again ostensibly reduces the need for a scenario analysis. But, with the future of the program still unclear and likely to be a major topic of Chairman Powell’s press conference on October 30, we tackle this issue in the second half of this report. We think the most likely outcome is that the Fed buys $60 billion of T-bills per month through the end of the year and then scales back, such that the total purchases amount to roughly $270 billion from mid-October through mid-April.

Base Case: A Third Consecutive Quarter-Point Cut (60% Probability)

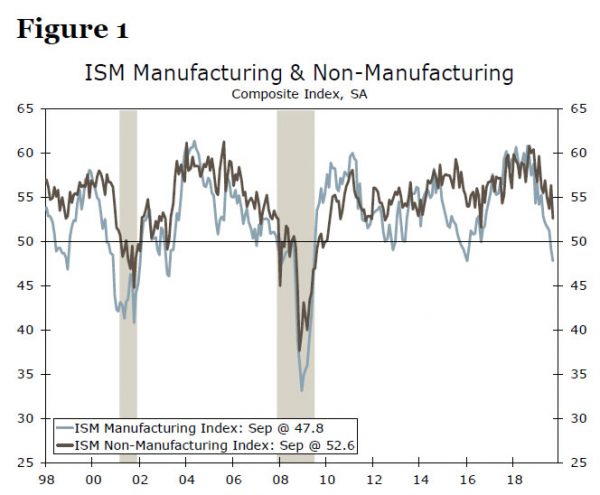

In a speech at the start of this month, Fed Chairman Powell remarked that the U.S. economy was in a good place and “our job is to keep it there as long as possible.” But a number of key indicators have moved in the “not good” direction. The ISM manufacturing index plumbed its lowest level since the depths of the recession in 2009, heralding even more contraction in the factory sector (Figure 1).

The service-sector ISM has managed to stay in expansionary territory (above 50), but this bellwether for a much larger part of the economy is at its lowest level in about three years. Many of the selected responses in both ISM surveys highlight the headwinds to business fixed investment (BFI) spending in a number of different industries from the ongoing trade war and tariffs. Until trade policy is clarified in a way that has a degree of permanence, it is not clear what would signal to Fed policymakers that BFI spending is set to improve meaningfully.

As it happens, uncertainties in trade policy leading to bad outcomes are exactly what worry the Fed. Consider the minutes from the September FOMC meeting in which policymakers acknowledge that “downside risks to the outlook for economic activity had increased…particularly those stemming from trade policy uncertainty and conditions abroad.” If the September cut was due to worries about trade policy uncertainty, an October cut could be justified on the basis of those uncertainties translating to actual declines in economic outcomes.

The fact that the trend weakening in the manufacturing sector has begun to bleed into the service sector is particularly worrying, as consumer spending had been a bright spot, at least until recently. This contamination effect of weakness in manufacturing and trade worries getting into consumers’ heads is something that concerns the Fed as well.

Although she is not a FOMC voter this year, hawkish Cleveland Fed President Loretta Mester said in the first week of October, “What I am looking for is: Are the weaknesses that we are seeing in trade and in manufacturing going to spill over to the consumer. So far, we have not seen that.” As of the time of her comments, the softer consumer confidence numbers had not yet led to declines in broad measures of actual spending. But by last week, retail sales figures for September came in well-below expectations, falling 0.3% relative to August and missing even the lowest forecast.

Although there has been some deceleration in “control group” retail sales, which aligns closely with consumer spending in the GDP accounts, it is still growing at a respectable pace (Figure 2). The question is whether policymakers view the September decline in retail sales, the first monthly drop in seven months, as an aberration or a sign of things to come.

In addition to the deterioration in the economic data, another compelling reason to expect a cut in October is the fact that the Fed has not made an earnest attempt to walk back financial market expectations for another 25 bps cut. If anything, Fed speakers have underpinned those expectations. On the very same day that the disappointing retail sales report was released, FOMC voter Charles Evans, President of the Chicago Fed, said, “there is some risk that the economy will have more difficulty navigating all the uncertainties out there or that unexpected downside shocks might hit…So there is an argument for more accommodation now to provide some further riskmanagement buffer against these potential events.”

Counter-Argument: The Case for No-Cut (40% Probability)

In the prior section, we highlighted how the Fed minutes for the September meeting discussed the deteriorating outlook for trade policy and the negative implications that might have for the economy. Although the trade situation has not meaningfully improved, one could reasonably argue that it has gotten no worse since the last FOMC meeting in September. Will a month or so without further escalation stay the committee’s hand?

There also is something to be said for the rising cost of “insurance.” If we re-read Charles Evans’ comment, he is essentially articulating the case for an ounce of prevention being worth a pound of cure. But as the FOMC guides the fed funds rate closer to zero, the number of quarter-point cuts shrinks, making each more scarce and thus more dear. It also risks fueling more risk taking and potential imbalances, a concern of Boston Fed President Eric Rosengren. In other words, the cost of an insurance cut is going up.

In these days of trade wars, administration criticism of Fed policy and discussions about extending the expansion, it is worthwhile to recall the Fed’s primary dual objectives of low and stable inflation and maximum employment. By any reckoning, the labor market is in solid shape. Although it is true that the pace of job growth is slowing, that comes with the territory when the unemployment rate sits at a 50-year low and businesses are finding it tougher to find qualified workers (Figure 3). The FOMC had already expected some slowing in job growth, as Chairman Powell highlighted in his last press conference, so the recent downshift is unlikely to concern the committee.

The robust labor market is at last giving way to stronger wage growth, although that has yet to push inflation up to the Fed’s 2.0% target. Ostensibly then, the fact that inflation is below target gives the Fed cover to cut rates, but is the inflation case really that compelling?

When the FOMC first raised rates in this cycle in December 2015, headline PCE inflation was sub-0.3% and core PCE inflation was below 1.3%. Compare that situation to where we are today (Figure 4, red circles). Both headline and core inflation are higher today than they were in December 2015 when the Fed began raising rates. In fact, core inflation is already back at the FOMC’s target, as prices have increased at a 2.1% annualized pace over the past six months.

We discussed earlier how “control group” retail spending has decelerated but that the growth rate is still solid. Real personal consumption expenditures (PCE) grew at an annualized rate of 4.6% in the second quarter, and not withstanding September’s soft print for retail sales, consumer spending is on track to be a major driver of GDP growth in Q3 as well. Although it is not our base-case scenario, policymakers at the Fed might reasonably evaluate the landscape in the context of its dual mandate and ask whether lower rates beyond the 50 bps of cuts since July are what the economy needs most at this moment, and opt to leave rates unchanged at this FOMC meeting.

Fed Balance Sheet: Action Announced, but What Next?

Anticipation had been building a few weeks ago that the Federal Reserve would announce a new asset purchase program at its October 30 meeting to deal with recent repo market volatility. Indeed, growing the balance sheet was one of the tools we listed in a recent report that detailed the options available to the Fed for dealing with upward pressure on money market rates.

Then, on October 11, the FOMC unexpectedly announced new policy actions that resulted from a video conference among committee members on October 4. In its statement, the FOMC committed to, at least through January 2020, “conduct overnight and term repo operations to ensure that the supply of reserves remains ample.” The Fed has been conducting overnight and term repo operations since repo rates skyrocketed on September 16/17, so this policy was simply an affirmation that the Fed will not be stepping away from the market anytime soon. This move was mostly in line with our expectations: even with an asset purchase program in place, it would take a few months before the impact of more reserves/fewer Treasury securities would be fully felt.

Second, the FOMC announced that the Fed will “purchase T-bills at an initial pace of approximately $60 billion per month, starting with the period from mid-October to mid-November.” There was no explicit number on additional purchases past that, but there was a commitment to “purchase T-bills at least into the second quarter of next year to maintain over time ample reserve balances at or above the level that prevailed in early September 2019.”

This unexpected inter-meeting decision helps the FOMC separate any monetary policy moves it makes at its October 30 meeting from these policy actions that the Fed has painstakingly tried to portray as technical in nature. Fed officials have repeatedly emphasized that these purchases are not quantitative easing (QE), as the main motivation is to add banking reserves to the financial system, and not to put downward pressure on long-term interest rates, as was the case in previous asset purchase programs.

That said, even though the FOMC has already taken action on the balance sheet, it is still worth exploring a bit more where the Fed’s balance sheet may go from here. Chairman Powell did not hold a press conference on October 11 when the new actions were announced, so the October 30 meeting will be a prime opportunity for him to expound upon the future of the program. In its October 11 statement, the FOMC left itself plenty of wiggle room to adjust the size of the monthly purchases going forward. Our best guess is that the plan is to act boldly between now and year-end, as year-end is when funding pressure are expected to be most acute (Figure 5).

We think the most likely outcome is that the Fed buys $60 billion per month through the end of the year and then scales back its purchases. For example, if the Fed were to buy $60 billion in the first two months, $45 billion in the next two months and then $30 billion in the final two months, this would put it on pace to cumulatively buy about $270 billion of Treasury securities, roughly in-line with our initial projections. By mid-April, we project this would result in total bank reserves being about $100 billion higher than they were in early September 2019 (Figure 6). We estimate that total net Treasury bill issuance will be about $225 billion over Q4-2019 and Q1-2020, meaning that our baseline scenario assumes the Fed will absorb all new T-bill supply in the coming months. Most of this new supply is set to come in February and March, meaning that net issuance will likely be negative over the next few months, after accounting for Fed purchases. This in turn could put some downward pressure on short-term Treasury yields and steepen out the curve, all else equal.

Scenario II: No Taper

What if, instead, the Fed were to maintain its purchases of Treasury bills at $60 billion a month for the next six months? We view this as the second most likely scenario, after the one outlined above. This approach would have the benefit of aggressively tackling upward pressure on repo rates. Purchases at this pace would likely lift total reserves to levels well above those seen in early September 2019. It would also send another signal to markets that the Fed will do whatever it takes

to resolve the issue. That said, pursuing this avenue is not without its drawbacks. The Fed wants to hold “no more securities than is necessary” to conduct monetary policy, so it would likely prefer to avoid an overkill move. If the goal is to get reserve levels a bit above where they were in early September 2019, there is likely no need to be this aggressive. Furthermore, such an aggressive entrance into the T-bill market could cause disruptions. Purchases at this pace would result in the Fed going from owning a tiny share of the T-bill market to 15% in just six months.

Scenario III: Aggressive Taper

The least likely scenario, in our view, is one in which the Fed tapers even more quickly than in our baseline scenario. An illustrative example of what this might look like can be found in the last row of Table 1. In this path, the Fed buys enough to get reserves back to roughly where they were in early September 2019 but no further. While possible, we suspect the Fed will want to provide more of a reserve buffer than this option offers. And, as mentioned previously, we also believe the Fed will want to remain aggressive in its buying through at least year-end in order to prevent a significant spike in repo rates, as occurred on December 31, 2018 (Figure 5).

What about a Standing Repo Facility?

Left unmentioned thus far has been the prospects for a standing repo facility (SRF), a solution to the repo problem we have argued would be a useful tool in the Fed’s arsenal. In our previous reports, we argued that the earliest time the Fed could realistically roll out a SRF was Q1-2020, given the technical challenges it is still contemplating. Recent developments lead us to believe that the SRF is still very much in the mix. The minutes from the September FOMC meeting reveal that when the committee was discussing the prospects for expanding the balance sheet to deal with recent repo market volatility, “several participants suggested that such a discussion could benefit from also considering the merits of introducing a standing repurchase agreement facility.”

Although we continue to think the longer-term prospects for a SRF are good, the Fed’s recent actions lead us to believe a SRF may not be imminent. The decisiveness of recent Fed policy action indicates it takes this issue very seriously, and likely wants to rely on tried-and-true policy tools until the repo situation is firmly in hand. Once that has been achieved, and as ongoing open market operations provide real world data on how the central bank’s actions can impact the repo market, the Fed can turn to more long-run considerations as part of the framework for implementing monetary policy.

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals