The US Fed and Bank of Canada still remain firmly focused on go-forward risks to growth from the US-China trade-war. The Fed cut rates for the third time in the last three meetings on October 30. The Bank of Canada held steady on rates, but clearly flagged concerns that slower global growth and trade disruptions could spill more significantly over to Canada. In Europe, another Brexit deadline came and went with a UK-EU divorce agreement deferred to early next year – and after another UK election.

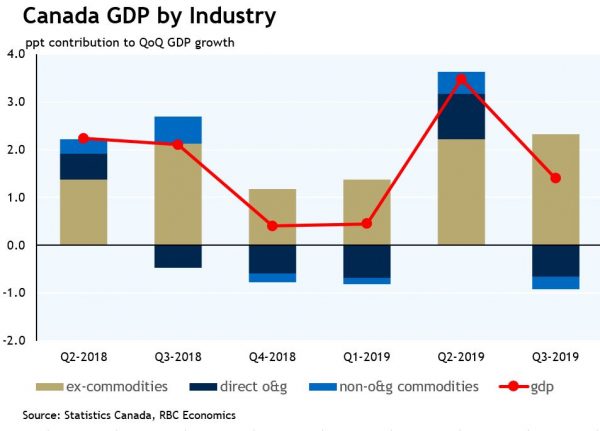

We certainly agree that concerns about global growth headwinds are legitimate. Yet current economic data has remained resilient, at least in North America. US GDP rose a respectable 1.9% in Q2 with another (probably trade-uncertainty-related) pullback in investment spending offset by another solid gain in consumer spending. And a strong October employment report left US household income/spending underpinnings on solid footing. In Canada, headline GDP growth is tracking a smaller gain, closer to 1 ½%, in Q3 after a modest 0.1% August GDP increase. And soft investment in the oil & gas sector has become more of a go-forward concern as well. Still, most of a Q3 (to-date) pullback in oil extraction looks like it is due to transitory disruptions that will reverse in the near-term. Excluding ‘commodities’ production – so largely the 70% of the economy accounted for by services-output – growth has actually been stronger-than-expected, tracking roughly a 2 1/2 % pace in Q3 by our count.

We expect that broad narrative to remain largely in place over the next week. In the US, service-sector growth indicators (i.e. the ISM non-manufacturing index) are expected to look a little better and still-low jobless claims data aren’t signalling rising layoffs. Canada’s September net trade report should show still lacklustre trends in export growth, and we assume a similar deficit to August. Canada’s October employment report will be watched closely for any sign that global industrial growth pressures are spilling over more significantly to the home-front – but the reality is labour markets will probably still look strong regardless of any move in the notoriously volatile employment count given (shockingly) strong recent trends. To be sure, we do not expect the almost 40k/month pace of employment growth over the last 12 months to be sustained, and wouldn’t be surprised if the job machine floundered in October. But it would take a dramatic move indeed to really cancel out prior positive trends. More important will be growth in wages, which have strengthened significantly in recent months, and any change in the unemployment rate, which tends to be more stable.

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals